Beyond the headlines: The ‘Magnificent Seven,’ AI, and the technology product cycle

Beyond the headlines: The ‘Magnificent Seven,’ AI, and the technology product cycle

The Magnificent Seven is at a critical juncture

The “Magnificent Seven”—Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla—are at a pivotal point in the early adoption of a new and transformative technology: artificial intelligence (AI).

At the same time, numerous financial news sources are presenting opinions as facts, which has contributed to a stressed investment environment for these seven global corporations.

In my view, much of the current retail financial commentary has been built on a mix of misinformation, manipulated information, and outright false information. I don’t believe there was ever an “AI bubble,” nor has there been a major shift of customers away from the AI technology largely driven by the Magnificent Seven toward a so‑called new AI model.

Warnings about the AI bubble started in late 2024 and grew throughout 2025 and 2026. Major financial outlets such as The Motley Fool, CNBC, Yahoo, Reuters, Fortune, and Bloomberg highlighted that sentiment—but often also offered counterarguments. Bloomberg has been at the forefront of reporting on AI-based valuations, the “new AI model,” and the cybersecurity risks posed by some of the newest AI technologies.

Understanding the technology product cycle

The Magnificent Seven are in a long‑term infrastructure development phase that began in late 2023 and is expected to conclude in late 2026. This phase represents a positive corporate action, not a warning sign for future growth.

Historically, new technologies move through identifiable phases of development and adoption. AI is no exception. Those phases typically include innovation, research and development, market introduction (early adopters), market integration (secondary adopters), market acceptance, mass market adoption (the longest phase), pre-market saturation, market saturation, market decline, and reinvention.

The timeline for each phase varies by technology. In addition to artificial intelligence, more than 20 emerging technologies are currently advancing through the earliest stages of this cycle.

AI and the current bull market

The current bull market began in 2023, coinciding with the initial introduction of AI technology into large corporations worldwide. In 2024, AI adoption expanded into small businesses.

At the same time, Fortune 1000 corporations in the United States faced a persistent challenge: a shortage of qualified college graduates with the education and training many roles required. Job openings have remained near 7 million openings for several years.

For many of these corporations, AI was viewed as the productivity solution to this labor shortage.

The reality of AI integration

What CEOs and CIOs quickly discovered was that AI is unlike any previous technology.

Integrating AI was not simply a matter of training programmers or staff to use new software. Instead, employees had to train AI systems for their specific roles and responsibilities. That process proved far more time‑consuming and costly than expected. AI also struggles with learning human language, a limitation that became apparent early in the integration process.

The result was a more challenging rollout than many companies had banked on, with several notable effects:

- Expected payroll reductions for lower‑level employees were delayed

- Costs for highly skilled employees increased

- Job openings remained elevated

AI did not deliver immediate corporate benefits at the pace many companies had anticipated.

![]() Related Article: Unraveling the 2025 market collapse: The hidden dynamics of market participants

Related Article: Unraveling the 2025 market collapse: The hidden dynamics of market participants

Market reaction and the 2025–2026 correction

Retail financial news outlets seized on this gap between expectations and reality. Sell‑side institutions and hedge funds took notice. In early 2025, the stock market experienced significant stress, creating profitable short‑selling opportunities.

Despite strong revenue and earnings growth, as well as an expanding AI customer base, the Magnificent Seven’s stock prices declined. In my view, that decline was not caused by weak earnings or an AI bubble. I believe the true cause of the 2025 market correction was the subtle weaponization of retail financial news, beginning with the AI bubble narrative.

Average American investors reacted to the headlines, while sell‑side institutions and hedge funds were already positioned to profit from short sales. The profitability of these trades encouraged even more negative commentary.

Recently, criticism has intensified around the Magnificent Seven, particularly Microsoft. Some have argued that Microsoft could lose both business and consumer AI customers due to competing free AI alternatives. I think those claims are misleading.

The reality of Microsoft’s AI position

Microsoft’s AI offerings primarily serve small businesses. Copilot is built into Microsoft’s operating system and is also available in a free version for PCs using Microsoft software.

Small businesses are often among a major corporation’s most loyal customers. They do not tend to switch quickly to new AI platforms. Many have already invested significant time and money in training employees and AI systems to fit their existing business models.

Now that these AI systems are operational, small businesses have little incentive to abandon them for a new AI platform that would require retraining both employees and technology from scratch.

Infrastructure investment is essential

Infrastructure development has been underway across the Magnificent Seven since 2024. Retail financial news has largely portrayed these investments as negative.

AI infrastructure spending is indeed a massive, high-stakes investment. It is often described as a virtuous circle for long-term growth, yet it has faced significant scrutiny for potential overinvestment and poor monetization.

In reality, infrastructure development is mandatory for the next phase of AI technology. AI is not traditional software. It is a neural network that operates above cloud technology. Without the cloud infrastructure developed over the past decade, AI neural networks would not exist.

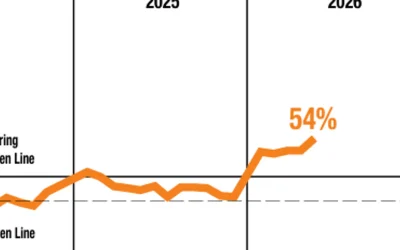

A sectorwide perspective

Rather than signaling weakness, infrastructure investment is a positive sign for the Magnificent Seven. Each company occupies a distinct niche in the AI market and is building the foundation necessary for future expansion.

The technology sector index illustrates where AI technology currently stands within its broader market cycle.

Source: TechniTrader

The top companies in this sector represent different industries:

- Amazon: e‑commerce and specialty retail

- Google and Meta: internet information services

- Microsoft: software applications for small businesses

- Apple: consumer electronics

- Nvidia: semiconductors

These companies are heavily weighted within the technology sector index, so their price movements largely define the sector’s overall trend. (Another Magnificent Seven company, Tesla, is excluded because it is classified as an automaker and not part of the technology index. However, Tesla is increasingly investing in next-generation chip technology.)

Still in a transition phase

New technologies do not advance in straight lines. The technology sector index points to an early‑stage growth trend in AI, marked by regular corrections rather than speculative excess. That volatility reflects the realities of infrastructure build‑out, workforce adaptation, and delayed efficiency gains. I believe the financial news media, in seeking an attention-getting narrative, has added heavily to investors’ concerns, along with sell-side institutions that have benefited from weakness—at least in the short term—in AI-related stocks.

The Magnificent Seven are navigating a necessary transition phase—one that historically precedes broader adoption and longer‑term expansion. Understanding where AI sits in its product and market cycle is essential to interpreting today’s market behavior accurately.

The opinions expressed in this article are those of the author and the sources cited and do not necessarily represent the views of Proactive Advisor Magazine. This material is presented for educational purposes only.

Martha Stokes, CMT, is the co-founder and CEO of TechniTrader and a former buy-side technical analyst. Since 1998, she has developed over 40 TechniTrader stock and option courses. She specializes in relational analysis for stocks and options, as well as market condition analysis. An industry speaker and writer, Ms. Stokes is a member of the CMT Association and earned the Chartered Market Technician designation with her thesis, "Cycle Evolution Theory." www.technitrader.com

Martha Stokes, CMT, is the co-founder and CEO of TechniTrader and a former buy-side technical analyst. Since 1998, she has developed over 40 TechniTrader stock and option courses. She specializes in relational analysis for stocks and options, as well as market condition analysis. An industry speaker and writer, Ms. Stokes is a member of the CMT Association and earned the Chartered Market Technician designation with her thesis, "Cycle Evolution Theory." www.technitrader.com

RECENT POSTS