The two-year Treasury-note yield calls for a Fed rate cut

The two-year Treasury-note yield calls for a Fed rate cut

Since 2009, I have been writing about how the yield on the two-year Treasury note sends a strong message about what the Federal Open Market Committee (FOMC) should do with its fed funds target. It is gratifying to see so many other analysts now picking up on this topic. Unfortunately, the FOMC has yet to do so, and the members—as well as the 400 Ph.D.s working at the Federal Reserve—seem to think they know better than the bond market.

Exactly how the two-year Treasury-note yield seems to know ahead of time what the FOMC is going to (eventually) do is an interesting question—but not an essential one. There is a long enough track record of the Fed ultimately doing what the two-year note suggests it should. How long it waits to get around to that is a big variable. The longer the delay, the more problems tend to arise.

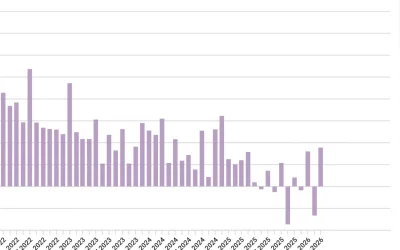

TRACKING THE TWO-YEAR TREASURY-NOTE YIELD VERSUS FED FUNDS RATE

Source: McClellan Financial Publications

![]() Related Article: Is the yield curve’s predicted recession arriving?

Related Article: Is the yield curve’s predicted recession arriving?

The most prominent example of this came in 2007. The real estate bubble had popped. Home and condo prices were falling dramatically by the time the FOMC made its first rate cut on Sep. 18, 2007, decreasing the fed funds target from 5.25% to 4.75%. But by that point, the two-year Treasury-note yield had already dropped to 3.97% and was falling fast.

FOMC members soon realized they had a big problem on their hands. On Jan. 22, 2008, they implemented a dramatic three-quarter-point rate cut. Even so, they were still behind the power curve, as the two-year yield was already down to 2.00%.

The necessity for those dramatic cuts came about in part because the Fed had kept rates too high in 2007 to ensure it had thoroughly deflated the real estate bubble. But in doing so, it applied the brakes too hard and then had to scramble to clean up the damage.

Thankfully, we are no longer facing the same problems. Still, the Fed is taking a risk by once again assuming it knows better. As of July 25, the fed funds target rate stands at 4.375%—0.44 percentage points too high, according to the two-year yield. Even if the FOMC had made a quarter-point cut at its July 30–31 meeting, policy would still be tight. We saw this dynamic before in early 2022, when the Fed was slow to hike rates and had to play catch-up with the two-year Treasury-note yield.

Chairman Jerome Powell likes to assert that the FOMC is “data dependent” when setting interest-rate policy. That may be true, but the Fed appears to be relying on the wrong data. It’s time to start inviting “Professor Two” to Jackson Hole—and to start listening more closely to what it has to say.

This is an edited version of an article that first appeared at McClellan Financial Publications on July 25, 2025.

The opinions expressed in this article are those of the author and the sources cited and do not necessarily represent the views of Proactive Advisor Magazine. This material is presented for educational purposes only.

Tom McClellan is the editor of The McClellan Market Report newsletter and its companion, Daily Edition. He started that publication in 1995 with his father Sherman McClellan, the co-creator of the McClellan Oscillator, and Tom still has the privilege of working with his father. Tom is a 1982 graduate of West Point, and served 11 years as an Army helicopter pilot before moving to his current career. Tom was named by Timer Digest as the #1 Long-Term Stock Market Timer for both 2011 and 2012. mcoscillator.com

Tom McClellan is the editor of The McClellan Market Report newsletter and its companion, Daily Edition. He started that publication in 1995 with his father Sherman McClellan, the co-creator of the McClellan Oscillator, and Tom still has the privilege of working with his father. Tom is a 1982 graduate of West Point, and served 11 years as an Army helicopter pilot before moving to his current career. Tom was named by Timer Digest as the #1 Long-Term Stock Market Timer for both 2011 and 2012. mcoscillator.com

RECENT POSTS