The University of Michigan’s preliminary February 2026 consumer sentiment reading, released Feb. 6, edged up to 57.3 from 56.4 in January, above consensus forecasts of around 55. This marked the highest level since August 2025, even as overall sentiment remains well below year-ago levels.

Beyond the headline number, current conditions improved to 58.3 from 55.4, while the expectations component slipped slightly to 56.6 from 57.0. Inflation expectations were mixed. One-year inflation expectations fell to 3.5% from 4.0%, the lowest level since January 2025, while five-year inflation expectations inched up to 3.4% from 3.3%. The survey window ran from Jan. 20 to Feb. 2, and the final February reading is scheduled for Feb. 20.

TABLE 1: UNIVERSITY OF MICHIGAN PRELIMINARY RESULTS FOR FEBRUARY 2026

Source: University of Michigan

Business analyst coverage of the report emphasized that the modest improvement looks uneven. Sentiment improved among households with large stock portfolios but was significantly weaker for those without equity exposure, reinforcing a more “K-shaped” feel to consumer attitudes.

At the same time, respondents continue to cite pressure from high prices and a heightened risk of job loss. They also highlighted ongoing sensitivity to tariff-related inflation and softer labor-market signals, including weaker job-openings data, even as the near-term inflation outlook cooled.

For markets and policy, the combination of better current conditions, easing one-year inflation expectations, but sticky-to-higher long-run expectations keeps the data consistent with a Federal Reserve that can’t yet declare victory on inflation expectations. The consumer backdrop may be resilient at the top end, but it remains fragile for more price-sensitive households.

University of Michigan commentary

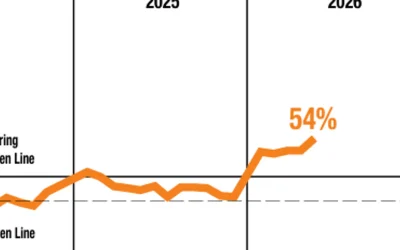

Surveys of Consumers Director Joanne Hsu reinforced the disparity between demographic groups in the report’s commentary:

“Sentiment surged for consumers with the largest stock portfolios, while it stagnated and remained at dismal levels for consumers without stock holdings. …

“While sentiment is currently the highest since August 2025, recent monthly increases have been small—well under the margin of error—and the overall level of sentiment remains very low from a historical perspective. Concerns about the erosion of personal finances from high prices and elevated risk of job loss continue to be widespread.”

FIGURE 1: WEALTH GAPS IN SENTIMENT CONTINUE TO WIDEN, MIRRORING TRENDS SEEN IN 2023 AND 2024

Source: University of Michigan

The Associated Press (AP) provided further perspective on income and spending discrepancy in a December 2025 article:

“From corporate executives to Wall Street analysts to Federal Reserve officials, references to the ‘K-shaped economy’ are rapidly proliferating.

“So what does it mean? Simply put, the upper part of the K refers to higher-income Americans seeing their incomes and wealth rise while the bottom part points to lower-income households struggling with weaker income gains and steep prices.

“A big reason the term is popping up so often is that it helps explain an unusually muddy and convoluted period for the U.S. economy. Growth appears solid, yet hiring is sluggish and the unemployment rate has ticked up. Overall consumer spending is still rising, but Americans are less confident. AI-related data center construction is soaring while factories are laying off workers and home sales are weak. And the stock market still hovers near record highs even as wage growth is slowing.”

AP further notes, “Poorer workers saw the largest [wage] growth in 2023-24, but the smallest in 2025.”

FIGURE 2: WAGE GROWTH WEAKENS FOR LOWER-INCOME WORKERS

Figures are adjusted for inflation.

Source: Federal Reserve Bank of Minneapolis / Graphic: Christopher Rugaber

![]() Related Article: No, a home price collapse isn’t on the horizon

Related Article: No, a home price collapse isn’t on the horizon

AP added, “After increasing at similar levels in 2023 and 2024, spending has diverged this year. Most recent figures are October spending increases from a year earlier by income level.”

FIGURE 3: HIGHER-INCOME CONSUMERS DRIVE SPENDING

Total credit and debit card spending per household, 3-month moving average, year-over-year growth.

Source: Bank of America Institute / Graphic: Christopher Rugaber

RECENT POSTS