Active ‘stock picking’ or passive market exposure?

Active ‘stock picking’ or passive market exposure?

A heated debate continues over whether investors should favor active or passive equity funds.

Recently, substantial outflows from active equity funds and strong inflows into passive strategies suggest that passive investing has won the argument.

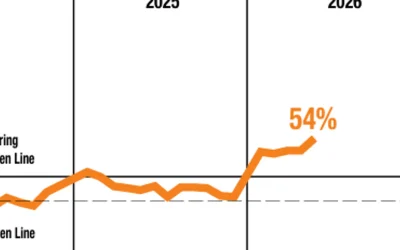

However, the current stock market environment tells a more nuanced story. As shown in the following chart, Athena’s Active Equity Opportunity (AEO) measure indicates that active strategies are currently more attractive.

ACTIVE EQUITY OPPORTUNITY (1998–2025)

Source: AthenaInvest Inc.

AEO is a statistical measure of stock market opportunity created by measuring how widely individual stock prices vary, including extreme highs, lows, and individual stock ranges.

Such market disruption provides managers with more opportunities to find mispriced stocks. Examining this measure over the almost 40-year period shown above, 55% of months favored stock picking, while 45% favored broad market exposure.

Recent developments have helped explain the significant outflows from active equity strategies. During the decade from 2010 to 2019, market exposure was favorable, and active managers correspondingly struggled to generate excess returns.

Following the COVID-related market disruption in 2020, the equity environment shifted decisively in favor of stock picking and has remained supportive since then. However, the Magnificent Seven stocks have masked the underlying market conditions and opportunities, as a handful of large stocks have driven broad indexes higher.

Despite some prevalent perceptions, the current market environment favors stock picking over passive market exposure. As market breadth improves, active equity investing will become increasingly attractive. While both active and passive investments have their merits, it is even more important to stay invested over the long term and avoid short-term loss aversion and performance chasing.

![]() Related Article: From plan to portfolio: A needs-based planning approach

Related Article: From plan to portfolio: A needs-based planning approach

From the behavioral viewpoint

What is going on?

- Short-term volatility and performance reporting generate strong emotions in the form of myopic loss aversion. This can drive us away from long-term growth investments. We do not want to make a mistake and experience the associated loss and regret, which are powerful emotional drivers. Daniel Crosby calls this psychological pattern “conservatism.”

- With the fallacy of control, we attempt to micromanage long-term investments as a series of short-term activities, seeking to manage 10 one-year investments, rather than one 10-year investment. This usually ends up in performance chasing and buying and selling the wrong investments at the wrong time.

- Delayed gratification requires a conscious effort to trade off a current benefit for long-term value. The benefit of being a better long-term investor comes years down the road.

What can investors do?

- Commit to long-term investing and learn to understand that progress toward goals is often more important than short-term investment performance.

- Work with a qualified financial advisor to develop a needs-based financial plan as a road map and to illustrate the value of long-term investing. Make contributions whenever possible. Be realistic, and review and update the plan regularly as life circumstances change.

- Build a strategy-diverse portfolio of active equity managers for long-term growth, and plan to invest in them for decades. Simple idea, but not easy to do.

- Consult with your financial advisor whenever questions arise. Financial advisors can add significant value through behavioral coaching, helping clients understand how the changing nature of risk and return can be managed through rules-based, data-driven investment decisions.

This is an edited version of an article that was first published by AthenaInvest on Jan. 15, 2026.

The opinions expressed in this article are those of the author and the sources cited and do not necessarily represent the views of Proactive Advisor Magazine. This material is presented for educational purposes only.

C. Thomas Howard, Ph.D., is the founder, CEO, and chief investment officer at AthenaInvest Inc. Dr. Howard is a professor emeritus in the Reiman School of Finance, Daniels College of Business at the University of Denver. Dr. Howard is the author of the book “Behavioral Portfolio Management” and co-author of “Return of the Active Manager.” AthenaInvest applies behavioral finance principles to investment management and also provides advisor coaching and educational resources.

C. Thomas Howard, Ph.D., is the founder, CEO, and chief investment officer at AthenaInvest Inc. Dr. Howard is a professor emeritus in the Reiman School of Finance, Daniels College of Business at the University of Denver. Dr. Howard is the author of the book “Behavioral Portfolio Management” and co-author of “Return of the Active Manager.” AthenaInvest applies behavioral finance principles to investment management and also provides advisor coaching and educational resources.

RECENT POSTS