6 trends impacting financial advisors in 2019

6 trends impacting financial advisors in 2019

While 2019 may present challenges in terms of market uncertainty and volatility, financial advisors have clear opportunities to further solidify client relationships, provide sound portfolio stewardship, and grow their practices. What are some key trends impacting advisors in the U.S.?

Financial advisors and their clients were in a relatively upbeat mood during 2018, up until they witnessed one of the worst December sell-offs since the Great Depression. The first quarter of 2019 saw a rapid, V-shaped market reversal, but many diverse concerns have remained at the forefront this year.

Within the context of uncertainty surrounding global macro issues, the lengthy bull market, and more volatile financial markets—both in 2018 and 2019—what are some of the major trends and issues impacting financial advisors as they look to solidify and grow their client bases and enhance revenue streams?

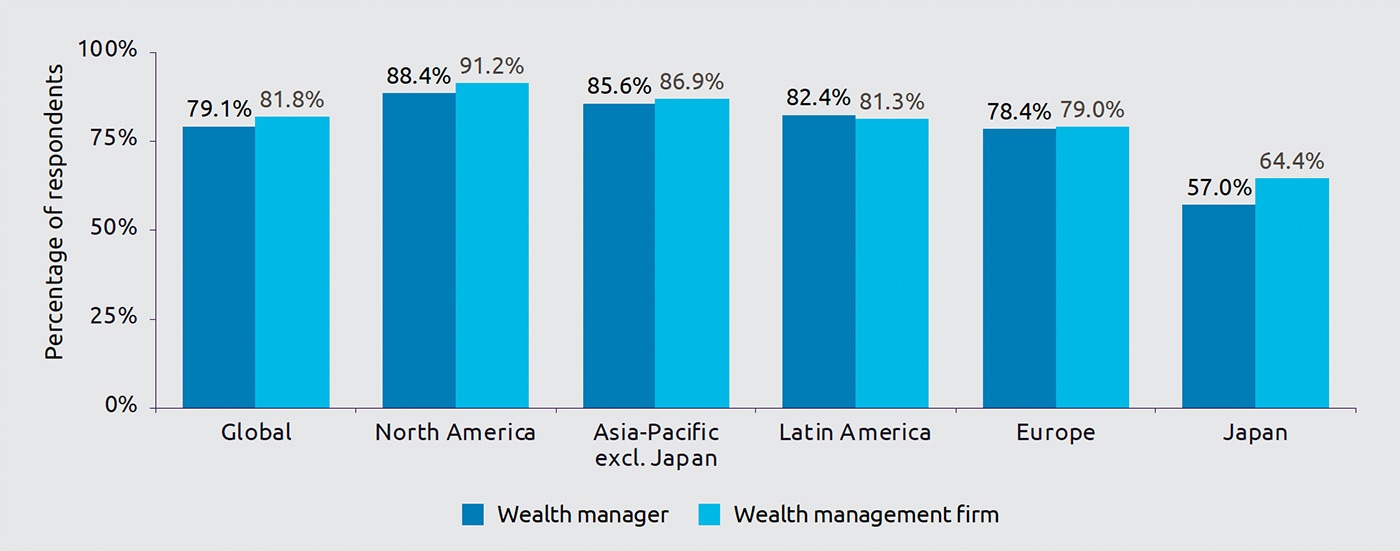

1. Overall satisfaction with wealth managers remained strong through the first quarter of 2019—but referral sentiment among clients could be much stronger.

High-net-worth clients were generally satisfied with their wealth managers through Q1 2019. This was despite a decline in overall wealth for high-net-worth clients globally—the first overall decline in seven years, says consulting and technology firm Capgemini. HNW individuals in North America saw their wealth shrink by 1.1% on average, which was a better performance than all other regions in the world, with the notable exception of the Middle East.

Capgemini’s “World Wealth Report 2019” reported several major findings regarding how North American HNW clients saw their relationships with financial advisors:

- 88.4% agreed or agreed strongly that they have trust and confidence in their primary wealth manager, and 91.2% agreed or agreed strongly on the same question for their primary wealth-management firm.

- Somewhat surprisingly, among those same HNW clients, only 50.3% said they were “likely to recommend the firm to a friend, family member, or colleague.” However, that was a significant uptick from Q4 2018’s 41.4%.

- The market volatility and downturn at the end of 2018 had a significant impact on HNW clients’ asset allocations, with cash or cash equivalents surpassing equities as the largest client asset class (27.1% versus 26.3%).

Source: Capgemini Financial Services Analysis, 2019; Global HNW Insights Survey, 2019

One of the potential reasons for the lower scores on “likelihood to refer” may have to do with the price/value relationship HNW clients saw in their relationships with wealth managers. Only 64.4% of North American HNW clients answered with positive responses to the question, “Given the performance of your assets and the service you received from your primary wealth management firm, how comfortable were you with the fees you were charged in 2018?”

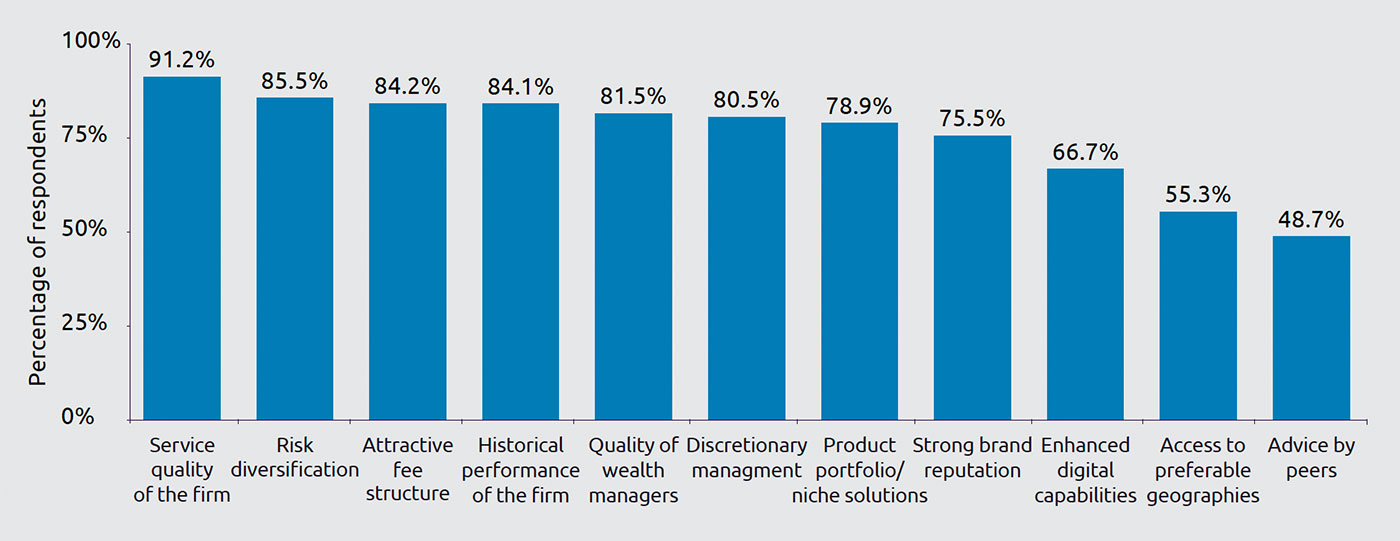

Service quality, risk diversification, attractive fees, and historical performance ranked as the most important factors in Capgemini’s study among HNW individuals in selecting a wealth-management firm.

FIGURE 2: PRIMARY CRITERIA FOR SELECTING A WEALTH-MANAGEMENT FIRM

Source: Capgemini Financial Services Analysis, 2019; Global HNW Insights Survey, 2019

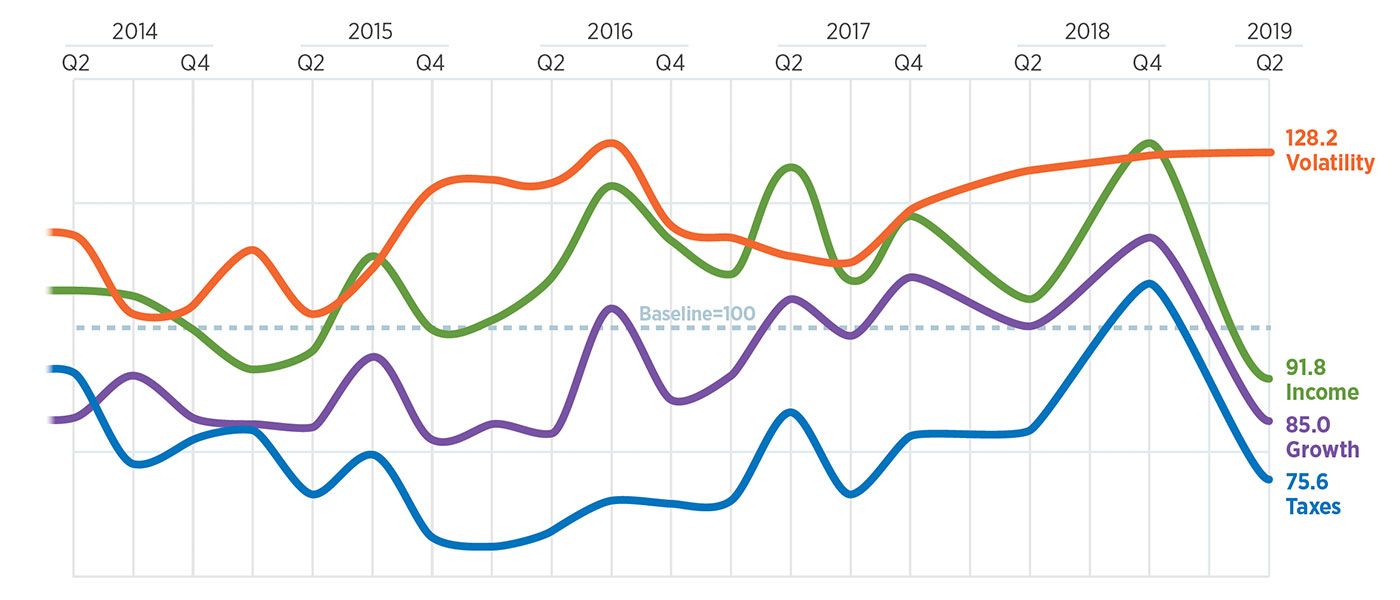

According to Eaton Vance’s Advisor Top-of-Mind Index Survey (Spring 2019):

- While sentiment has improved markedly since the beginning of the year, advisors expect volatility to remain a primary concern in financial markets. Monitoring the economic impact of trade negotiations and the U.K.’s Brexit plan are high on the Federal Reserve’s watch list, which undoubtedly makes those both of prime concern to financial advisors as well.

- Generating income, growing capital, and managing tax exposure remain important objectives as advisors guide their clients, but currently fall below the importance of “managing volatility” in the current market environment.

FIGURE 3: RELATIVE IMPORTANCE OF 4 FACTORS FOR CLIENTS’

FINANCIAL/INVESTMENT PLANNING

Source: Eaton Vance Advisor Top-of-Mind Index (ATOMIX), Spring 2019

Specific findings of Eaton Vance’s study among financial advisors include the following:

- 94% note clients are interested in reallocating their portfolios based on volatility.

- 58% say volatility will increase in the U.S. stock market over the next six months.

- 57% believe the U.S. political environment and geopolitical issues and/or conflicts will be the top drivers of volatility.

- 88% state that political developments now factor into client conversations about the market.

- 79% say they have no concern about a possible recession in 2019.

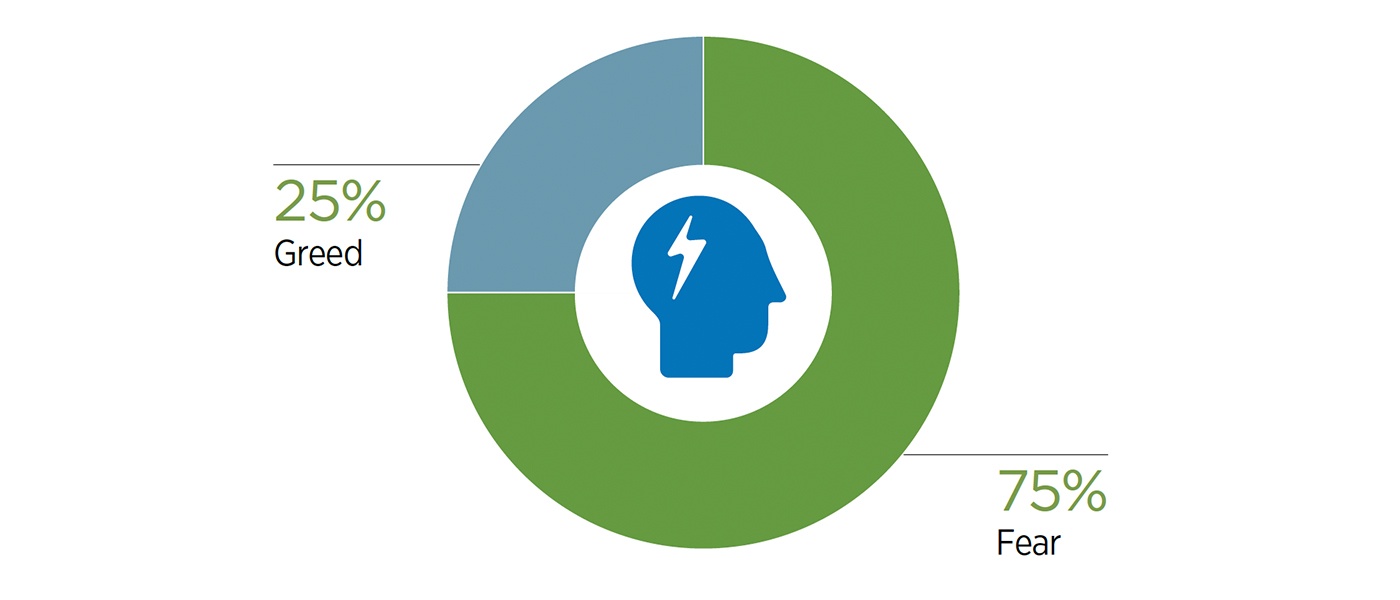

When advisors were asked to characterize current client attitudes toward the financial markets in the spring of 2019, it was clear that they believed capital preservation was top-of-mind for clients. While advisors largely described themselves as bullish on the market and optimistic, they saw clients as being “wary and anxious.”

Source: Eaton Vance Advisor Top-of-Mind Index (ATOMIX), Spring 2019

According to Natixis’ 2019 Global Survey of Individual Investors, “Investors expect greater returns than professionals say is realistic.”

This presents a thorny challenge for financial advisors, as investors tend to exhibit a strong recency bias. For example, the same study says, “While nearly 2/3 of investors felt they were prepared for market risks at the start of 2018, in hindsight, only 59% say they were actually prepared for last year’s downturn.”

Another example from the study states the following:

- 8 in 10 financial professionals say the bull market has made investors too complacent about risk.

- However, 8 in 10 investors claim to understand the risks posed by the market environment in 2019.

And, while 9 in 10 investors say it is important to protect their assets in volatile times, they have investment performance expectations that are seemingly out of sync with their risk tolerance—as well as the performance expectations of their financial advisors.

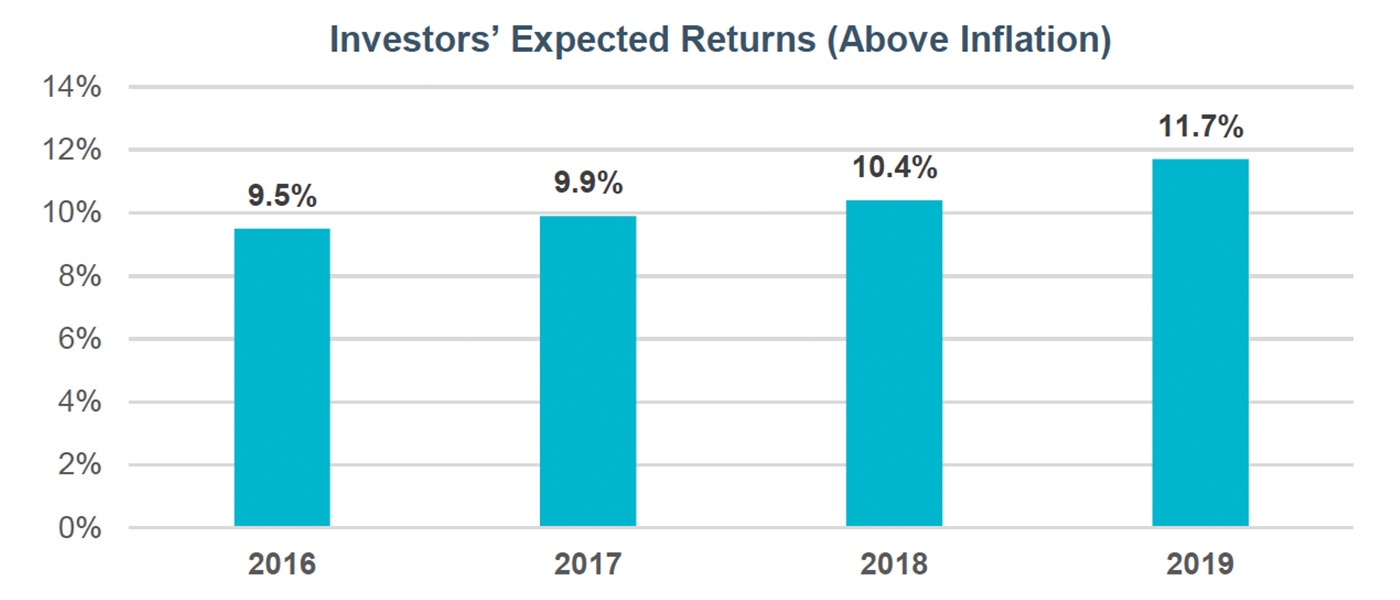

In the U.S., investors now expect an average annual return of 10.9% above inflation, while their advisors see 6.3% as more realistic. That represents a 73% “expectation gap.”

Globally, the expectation gap is even more pronounced, as seen in Figure 5.

Source: Natixis Investment Managers 2019 Global Survey of Individual Investors;

Natixis Global Survey of Financial Professionals, 2018

Source: Natixis Investment Managers 2019 Global Survey of Individual Investors

The survey notes, “Investors need to realize that pursuing these greater returns will likely mean taking on more risk—as well as significant exposure to the volatility they see as a threat to their savings goals.”

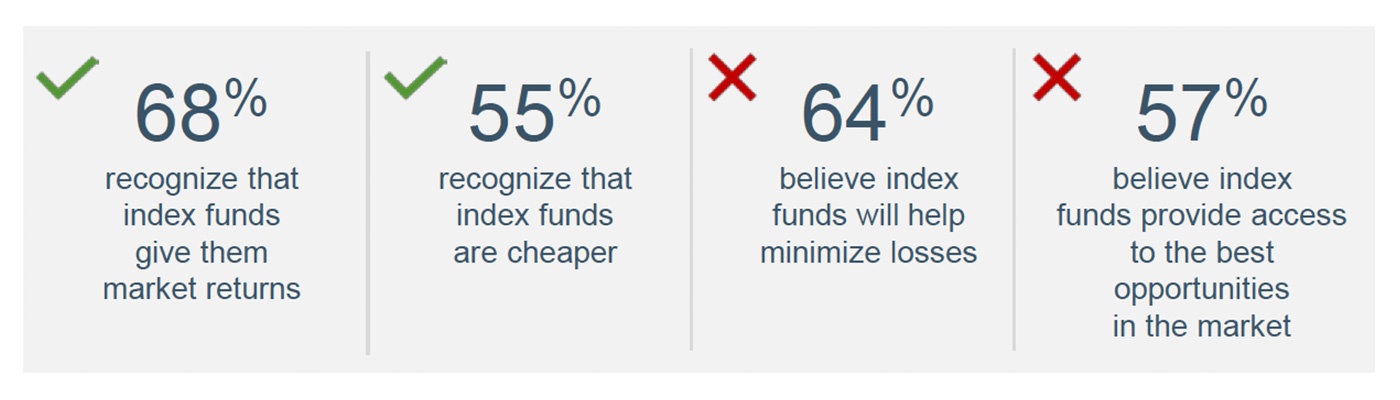

On a related topic, the Natixis survey shows that many investors are “confused about the fundamental differences between active and passive investing.” The survey further states the following:

- “68% of investors claim to know the difference between active and passive investments, yet one-third of investors did not recognize that index funds give them market returns.

- “2/3 of investors said the volatility made them realize that index funds were riskier than they thought.

- “A surprising 62% of investors ignore that experience and still say they believe index funds are less risky.”

Source: Natixis Investment Managers 2019 Global Survey of Individual Investors.

For a majority of investors, Natixis says, index funds “may actually run counter to their investment expectations.”

The study finds that roughly 7 in 10 investors worldwide:

- “Believe it is important that their investments give them a chance to beat the benchmark (71%).

- “Say it’s important to have the ability to take advantage of short-term market movements (70%).

- “Expect their mutual fund to have a portfolio that’s different from the index (68%).”

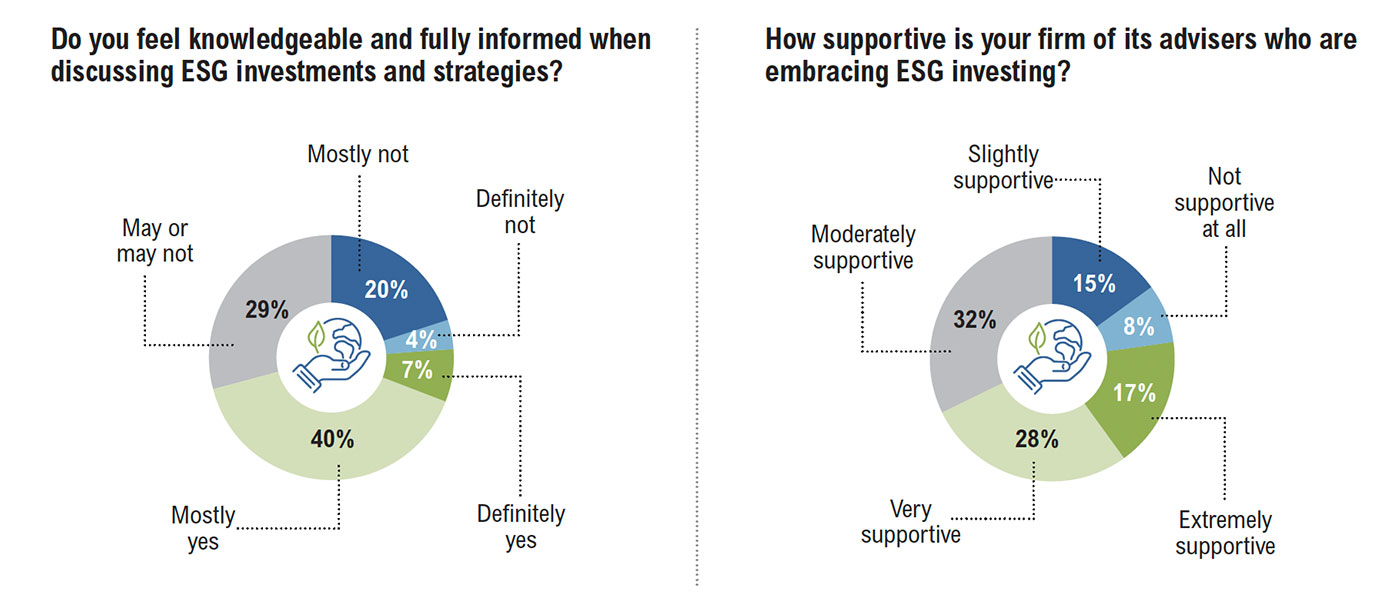

The InvestmentNews white paper, “Opportunity Knocks: How Advisers Can Capitalize on Growing ESG Interest,”states, “As interest in Environmental, Social and Governance investing grows, so too has the business opportunity for advisers. The window to seize it remains wide open. … While advisers anticipate growing ESG demand from their clients, relatively few are using ESG to attract new clients or create a niche for their business. And fewer than half of advisers said they feel knowledgeable about ESG investing.”

FIGURE 8: ADVISOR KNOWLEDGE/FIRM SUPPORT CONCERNING

ESG INVESTMENTS/STRATEGIES

Source: InvestmentNews Research, “How advisers can capitalize on growing ESG interest.”

InvestmentNews adds, “Only 32% of advisers use ESG to attract new clients and only 25% utilize it to create a niche for their business. Further, only 44% of advisers take ESG factors into account when constructing portfolios, which is in line with last year’s survey.”

Perhaps the most powerful evidence of the opportunity for advisors lies in these two findings:

- Advisors are tending to let clients take the lead in ESG discussions. Only 21% of advisors said their firm “is proactive in initiating ESG conversations.”

- Advisors are consistently underestimating ESG across many different demographics and wealth sectors. For example, advisors perceive that only a third of mass affluent clients would be interested in ESG investing, while 50% of clients in this segment report that they have an interest.

While 84% of advisors recognize the growing interest of their client base in specific social and environmental issues, the challenge is translating that into confident knowledge in the space and the ability to provide sound ESG investment strategies.

According to 2018 research sponsored by Natixis and summarized in an article by WealthManagement, financial advisors “are as keen as ever on active management,” especially in an environment characterized by uncertain interest-rate policy and increased market volatility.

The article says, in part,

“Advisors who participated in the annual survey said they allocated roughly two-thirds (67 percent) of client portfolios to actively managed strategies and one-third to passive. … They also projected that active management would account for 62 percent of allocations in 2021.

“David Goodsell (the executive director of Natixis Investment Managers’ Center for Investor Insight) said advisors, and their clients, have pursued passive investments for their lower fees, especially considering their relative performance through the recent bull market. But most advisors (74 percent) believe individual investors are unaware of the risks of passive strategies, according to the recent survey, and they will need to convince them that now is the time for active management and to effectively deliver it.”

Research sponsored by AMG Funds among individuals with over $1 million in investable assets portrays the investment role advisors should play in the eyes of such clients:

- 85% say, “Make sure my portfolio is appropriately diversified.”

- 82% say, “Monitor my portfolio and make adjustments if market conditions change.”

- 76% say, “Explain complex investments or strategies to me so I understand them.”

- 76% say, “Explain changes in the economic environment and how they impact me.”

- 68% say, “Generate ideas/keep me informed of the latest in investing.”

- 66% say, “Introduce me to investments or strategies I may not be familiar with.”

Within the context, advisors have the challenge and opportunity to further educate their clients, pointing out the respective benefits and potential shortcomings of both active and passive investments and strategies. The key, say many industry experts, is having clients focus on the long-term and full market cycles, not chasing the best-performing strategies of the last year or three years.

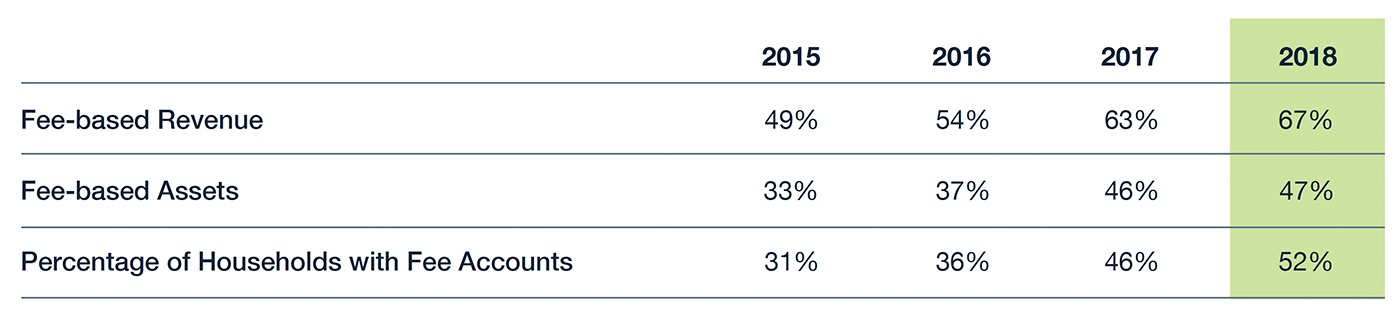

PriceMetrix, a leading research, data, and consulting firm focusing on the financial advisor segment, says that a key driver of advisor revenue growth was “the continued proliferation of fee-based accounts.” Revenues from fee accounts grew by 17% in 2018 over 2017.

PriceMetrix reports,

Source: PriceMetrix, “The State of Retail Wealth Management 2018,” April 2019.

In line with these findings, research sponsored by Northern Trust in 2016 finds that 41% of financial advisors use external investment-management firms for more than 75% of client assets under management (AUM). Some of the key reasons are related to portfolio services, with respondents citing the following factors:

- Portfolio construction expertise (76%).

- Access to investment managers (67%).

- Asset allocation (64%).

- Portfolio monitoring (57%).

Another area of importance is how the use of third-party managers allows advisors to free up their time. The survey finds advisors value this time savings for direct client interaction (61%), business development (53%), and providing a higher level of personalized service (50%).

***

The research cited here is consistent with Proactive Advisor Magazine’s discussions with independent financial advisors around the country. The trends are clearly toward the growth of fee-based practices, the use of third-party money managers who provide strategies geared toward risk management, and a healthy mix of both passive and active strategies for clients to provide further diversification and mitigate the risk from market shocks. Many advisors feel most comfortable diversifying client portfolios along numerous dimensions, including by time horizons, asset classes, strategies, and asset managers.

Advisors have numerous opportunities in 2019 for client development, revenue growth, and enhancing their current client relationships—despite all of the uncertainties of the markets and the external environment. We hope the six key trends examined in this article provide insights directly tied to achieving those important objectives.

David Wismer is editor of Proactive Advisor Magazine. Mr. Wismer has deep experience in the communications field and content/editorial development. He has worked across many financial-services categories, including asset management, banking, insurance, financial media, exchange-traded products, and wealth management.

David Wismer is editor of Proactive Advisor Magazine. Mr. Wismer has deep experience in the communications field and content/editorial development. He has worked across many financial-services categories, including asset management, banking, insurance, financial media, exchange-traded products, and wealth management.