Analyst Charlie Bilello summed up the first half of 2025 in a recent presentation: “From surprise tariff headlines and sticky inflation to tech’s continued dominance and a shifting Fed narrative—2025’s first half has been anything but quiet.”

However, “an upbeat start to earnings season has helped to quell tariff fears for now,” reports CNBC, adding,

“In particular, big banks such as JPMorgan Chase and Goldman Sachs, which serve as barometers for economic activity, had solid beats, boosting investor sentiment.

“Next in the spotlight are Big Tech earnings, which will be released in the weeks right before Aug. 1. If better than expected, they might dispel geopolitical jitters—or cause investors to dismiss trade fears too readily. In these stormy times, every silver lining has a dark cloud.”

The Q2 2025 earnings season for S&P 500 companies began in earnest during the second full week of July, with big banks such as JPMorgan, Citigroup, Wells Fargo, Bank of America, Goldman Sachs, and Morgan Stanley kicking things off with reports from July 15 through 18.

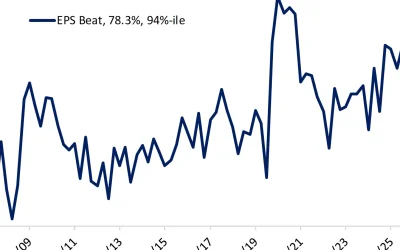

As of last week, about 12% of S&P 500 companies had reported results. Among those, roughly 83% beat earnings expectations, and the same percentage topped revenue forecasts. Although estimates had been lowered, this uptick is starting to push overall earnings expectations for the quarter back up.

The financial sector has been a standout. Every bank that has reported so far has exceeded earnings estimates, with 84%–85% beating revenue expectations. JPMorgan saw an 8% year-over-year boost in adjusted earnings, and Citi and Wells Fargo reported profit increases of 25% and 12%, respectively. Bank of America beat earnings-per-share (EPS) estimates and saw net interest income rise. Goldman Sachs posted record equity trading revenues, and net income surpassed expectations. Morgan Stanley also beat expectations, with strong earnings and a 15% year-over-year profit increase.

Despite some mixed signals—from Wells Fargo missing net interest income and Bank of America falling short on revenue—management of these companies remain upbeat, citing resilient consumer lending, strong trading volumes, and improved deal flow.

Still, the question remains: Will the “hard tariff deadline” of Aug. 1, 2025, and potential actions from the Trump administration on trade negotiations affect earnings for large companies through year-end and into 2026?

Lori Calvasina, head of U.S. equity strategy at RBC Capital Markets, told Bloomberg this week that many investors and companies are dialing back their expectations of tariff policy impact, while she believes tariffs will be more inflationary than expected. She noted,

![]() Related Article: Q1 real GDP growth revised lower to a -0.5% annualized rate

Related Article: Q1 real GDP growth revised lower to a -0.5% annualized rate

Highlights for Q2 2025 earnings to date: S&P 500 companies

FactSet offered the following topline findings in its July 18 Earnings Insight:

“Key Metrics

- “Earnings Scorecard: For Q2 2025 (with 12% of S&P 500 companies reporting actual results), 83% of S&P 500 companies have reported a positive EPS surprise and 83% of S&P 500 companies have reported a positive revenue surprise.

- “Earnings Growth: For Q2 2025, the blended (year-over-year) earnings growth rate for the S&P 500 is 5.6%. If 5.6% is the actual growth rate for the quarter, it will mark the lowest earnings growth reported by the index since Q4 2023 (4.0%).

- “Earnings Revisions: On June 30, the estimated (year-over-year) earnings growth rate for the S&P 500 for Q2 2025 was 4.9%. Seven sectors are reporting (or are expected to report) higher earnings today (compared to June 30) due to positive EPS surprises and upward revisions to EPS estimates.

- “Earnings Guidance: For Q3 2025, 3 S&P 500 companies have issued negative EPS guidance and 4 S&P 500 companies have issued positive EPS guidance.

- “Valuation: The forward 12-month P/E ratio for the S&P 500 is 22.2. This P/E ratio is above the 5-year average (19.9) and above the 10-year average (18.4).”

In its overview, FactSet also adds:

“At this early stage, the second quarter earnings season for the S&P 500 is off to a strong start compared to expectations. Both the percentage of S&P 500 companies reporting positive earnings surprises and the magnitude of earnings surprises are above their 10-year averages. As a result, the index is reporting higher earnings for the second quarter today relative to the end of last week and relative [to] the end of the quarter. However, the index is also reporting its lowest year-over-year earnings growth rate since Q4 2023 (4.0%).

“Overall, 12% of the companies in the S&P 500 have reported actual results for Q2 2025 to date. Of these companies, 83% have reported actual EPS above estimates, which is above the 5-year average of 78% and above the 10-year average of 75%. In aggregate, companies are reporting earnings that are 7.9% above estimates, which is below the 5-year average of 9.1% but above the 10-year average of 6.9%. Historical averages reflect actual results from all 500 companies, not the actual results from the percentage of companies that have reported through this point in time.

“During the past week, positive EPS surprises reported by companies in the Financials sector were the largest contributors to the increase in the overall earnings growth rate for the index over this period. Since June 30, positive EPS surprises reported by companies in the Financials sector, partially offset by downward revisions to EPS estimates for companies in the Health Care sector, have been the largest contributors to the increase in the overall earnings growth rate for the index over this period. …

“Six of the eleven sectors are reporting (or are projected to report) year-over-year growth, led by the Communication Services and Information Technology sectors. On the other hand, four sectors are reporting (or are predicted to report) a year-over-year decline in earnings, led by the Energy sector. One sector (Health Care) is reporting flat (0%) year-over-year earnings.”

FIGURE 1: PROJECTED S&P 500 EARNINGS GROWTH BY SECTOR (Y/Y)—

Q2 2025

Source: FactSet

FIGURE 2: S&P 500 CALENDAR YEAR BOTTOM-UP EPS ACTUALS AND ESTIMATES

Source: FactSet

RECENT POSTS