Crude oil prices have moved higher in February, with Brent crude and WTI (West Texas Intermediate) recently reaching their highest closes in roughly six months.

Reuters reported on Feb. 22, “Growing concern over potential military conflict between the U.S. and Iran pushed Brent prices up more than 5% last week to their highest since July 2025 at $72.34.”

As markets repriced the probability of supply disruptions tied to U.S.–Iran tensions, the move has implications for U.S inflation estimates, consumer sentiment, sector leadership, and supply-chain costs.

Despite this, Bespoke Investment Group struck a more positive tone last weekend when assessing crude’s price action relative to the dollar and Treasury yields:

“While US stocks have underperformed their global peers this year (and last), the outlook for US stocks remains moderately positive. One reason is the levels of our three-headed monster relative to their one-year ranges. As of Thursday’s close, both the Dollar Index and the 10-year US Treasury yield were in the lower quintiles of their respective one-year ranges while crude oil was just barely in the upper half of its one-year range, largely due to fears of a flare-up in Iran. While an actual military strike will likely cause prices to spike even more, if negotiations are successful, you could expect to see prices quickly revert lower.

“Two out of three isn’t bad, and there’s a good chance that even the third (crude oil) could pull back in the coming weeks. Historically when each component of the three-headed monster has been low or declining, it has been a positive tailwind for equities, while high or increasing levels act as headwinds for stocks.”

FIGURE 1: WTI CRUDE OIL—PAST 12 MONTHS

Source: Bespoke Investment Group

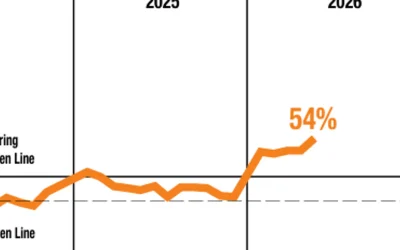

FIGURE 2: ‘3-HEADED MONSTERS’ AVG. LEVEL RELATIVE TO 52-WEEK RANGE (PAST YEAR)

Avg. combined level of U.S. Dollar Index, 10-year Treasury yield, and crude oil price

Source: Bespoke Investment Group

A closer look at what is behind crude oil’s move higher

1. The return of a Middle East ‘tail-risk’ premium

The dominant driver of higher oil prices has been geopolitics rather than a sudden surge in demand. MarketWatch notes that markets have been reacting to escalating U.S.–Iran tensions and the unpredictable risk of shipping disruptions through the Strait of Hormuz, a critical chokepoint for global crude and products. Analysts regularly cite Hormuz as handling roughly one-fifth of global oil flows; even the threat of disruption can lift prices.

The IEA described how prices reversed sharply higher after the U.S. advised ships to avoid Iranian waters while navigating Hormuz, underscoring how quickly “risk premium” can reenter the curve even if physical balances haven’t fundamentally tightened.

2. Sanctions enforcement and ‘constrained’ barrels

Another contributor has been tighter enforcement of sanctions affecting Russian and Iranian flows. According to Reuters, Citi analysts flagged that Brent’s move from around $60 toward $70 over the past month partially reflects stricter sanctions enforcement alongside other disruptions. Global supply may look ample on paper, but when barrels are sanctioned, rerouted, or sitting offshore, pricing can remain tighter than global supply totals imply.

3. Short-term supply interruptions

Physical disruptions have also mattered at the margin. The IEA reported that world oil supply was affected as severe winter weather disrupted North American operations and outages and export constraints hit Kazakhstan, Russia, and Venezuela.

4. Policy and production signals remain fluid

OPEC+ remains the key swing supplier, with Reuters citing a potential resumption of increased oil output. Markets have been weighing the potential for higher output later this spring against the incentive to manage volatility during a geopolitical flare-up. Shifting expectations for production and export levels among major producers have added to uncertainty.

![]() Related Article: ‘Hindenburg Omen’ signals are back

Related Article: ‘Hindenburg Omen’ signals are back

Current situation and future outlook

At the time of this writing, ongoing nuclear negotiations between the U.S. and Iran are set to resume on Thursday, Feb. 26.

CNBC assessed the situation early Monday, Feb. 23:

“Tensions have remained on high alert throughout the Middle East for weeks after U.S. President Donald Trump indicated a strike on Iran could be imminent.

“Since then, a sense of calm has returned to oil markets, after reports on Friday indicated that any strike would be limited to military installations or government sites, reducing the risk for a protracted conflict between the two countries, and retaliation by Iran towards U.S. bases in the region.

“‘The geopolitical atmosphere, at least for today, has moderated a little bit, and I think that’s what we’re seeing being reflected in the pullback in prices,’ Edward Bell, acting chief economist at Emirates NBD, told CNBC’s Dan Murphy on Monday.”

However, volatility in oil markets remains the base case for most analysts. If tensions persist around Hormuz, crude can remain higher even if the underlying supply-demand balance is supportive of lower prices. Conversely, credible de-escalation can remove risk premium quickly.

In a February report, the IEA stated,

The IEA foresees a similar decline for WTI crude prices if the political situation between the U.S. and Iran reaches more stable ground.

FIGURE 3: WEST TEXAS INTERMEDIATE (WTI) SPOT PRICE AND FUTURES PROJECTIONS ($ PER BARREL)

Sources: U.S. Energy Information Administration, Bloomberg, LSEG Data

RECENT POSTS