Last week, the six largest U.S. banks reported third-quarter 2025 results that largely exceeded analysts’ expectations.

Robust trading and investment-banking fees drove outperformance at JPMorgan Chase, Citigroup, Goldman Sachs, and Wells Fargo, which reported results on Oct. 14. Healthy net interest income from an elevated rate environment added to the upside. However, several institutions noted ongoing investments in technology and compliance and maintained a cautious stance on credit costs.

Bank of America and Morgan Stanley posted better-than-forecast results on Oct. 15. Bank of America’s net interest income rose faster than expected, thanks in part to strong mortgage-banking gains. Morgan Stanley delivered record investment-banking fees alongside double-digit growth in its wealth-management and trading divisions. Both firms reaffirmed full-year guidance but noted that market volatility and higher funding costs warrant vigilance.

Despite the solid showing from major banks, the overall financial sector was “spooked” by several negative credit events last week, according to Schwab:

“Bank earnings took on new importance today [10/17] after credit concerns sent regional bank shares down 6% Thursday and spooked the market two weeks before Halloween. … Recent bankruptcies of two firms serving the auto industry raised questions about banks’ lending practices, leading to double-digit drops yesterday for shares of two banks that confirmed exposure to fraudulent loans.

“Ally Financial (ALLY), Fifth Third Bancorp (FITB), and Regions Financial (RF) all easily topped analysts’ earnings and revenue estimates this morning and saw their shares rise in pre-market trading, easing some fears. Still, their executives will likely face questions about loans as well as the general credit environment. In early 2023, the entire market suffered a blow from several regional bank failures.

“Banking concerns arose at a time when ‘speculative froth’ has developed in the market, said Liz Ann Sonders, chief investment strategist at Schwab, on CNBC’s ‘Closing Bell’ Thursday. ‘When you have that speculative froth and then you have sort of a bigger picture potential issue, those two can sometimes collide and cause an increase in volatility,’ she said.”

The KBW Nasdaq Bank Index (BKX) tracks the performance of 24 leading publicly traded U.S. banks and thrift institutions, including large national money centers, regional banks, and thrifts. The Index was down about 7% from its mid-September highs last week.

FIGURE 1: KBW BANK INDEX (BKX)—PAST THREE MONTHS

Source: MarketWatch. Data through 10.17.2025.

Outlook for the Q3 2025 earnings season

FactSet recently provided updated estimates for S&P 500 earnings growth for Q3 2025, noting that results are shaping up positively so far:

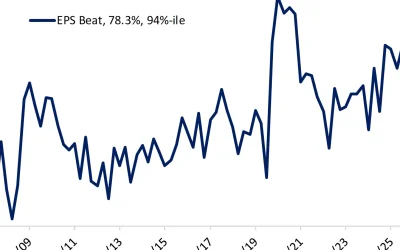

“The estimated earnings growth rate for the S&P 500 for the third quarter is 8.0%, which would mark the 9th consecutive quarter of (year-over-year) earnings growth reported by the index. Given that most S&P 500 companies report actual earnings above estimates, what is the likelihood the index will report earnings growth of 8.0% for the quarter?

“Based on the average improvement in the earnings growth rate during the earnings season, the index will likely report earnings growth above 13% for the third quarter, which would mark the 4th straight quarter of double-digit growth.”

Highlights for Q3 2025 earnings to date

In its Oct. 17 Earnings Insight, FactSet shared several key metrics on earnings progress through mid-month:

- “Earnings Scorecard: For Q3 2025 (with 12% of S&P 500 companies reporting actual results), 86% of S&P 500 companies have reported a positive EPS surprise and 84% of S&P 500 companies have reported a positive revenue surprise.

- “Earnings Growth: For Q3 2025, the blended (year-over-year) earnings growth rate for the S&P 500 is 8.5%. If 8.5% is the actual growth rate for the quarter, it will mark the ninth consecutive quarter of earnings growth for the index.

- “Earnings Revisions: On September 30, the estimated (year-over-year) earnings growth rate for the S&P 500 for Q3 2025 was 7.9%. Six sectors are reporting higher earnings today (compared to September 30) due to positive EPS surprises.

- “Earnings Guidance: For Q4 2025, 2 S&P 500 companies have issued negative EPS guidance and 8 S&P 500 companies have issued positive EPS guidance.

- “Valuation: The forward 12-month P/E ratio for the S&P 500 is 22.4. This P/E ratio is above the 5-year average (19.9) and above the 10-year average (18.6).”

FIGURE 2: S&P 500 CHANGE IN FORWARD 12-MONTH EPS VS.

CHANGE IN PRICE—10 YRS.

Source: FactSet

![]() Related Article: Is there a ‘right’ federal funds rate?

Related Article: Is there a ‘right’ federal funds rate?

FactSet observed that early results pointed to many companies outperforming expectations, though by narrower margins than in past quarters:

“At this early stage, the third quarter earnings season for the S&P 500 is off to a mixed start relative to analyst expectations. While the percentage of S&P 500 companies reporting positive earnings surprises is above recent averages, the magnitude of earnings surprises is below recent averages. …

“Overall, 12% of the companies in the S&P 500 have reported actual results for Q3 2025 to date. Of these companies, 86% have reported actual EPS above estimates, which is above the 5-year average of 78% and above the 10-year average of 75%. …

“During the past week, positive EPS surprises reported by companies in the Financials sector were the largest contributor to the increase in the overall earnings growth rate for the index over this period. Since September 30, positive EPS surprises reported by companies in the Financials sector, partially offset by downward revisions to EPS estimates for companies in the Health Care sector, have been the largest contributor to the increase in the overall earnings growth rate for the index over this period.”

RECENT POSTS