The S&P 500’s capitulation day on April 8, 2025, saw the Index closing below 5,000 at 4,982.77, its lowest finish of the year amid tariff headlines. By the market close on Aug. 15, the S&P 500 stood at 6,449.80—a gain of roughly 29.4% from the April 8 close.

The rally pushed the Index to a string of fresh record highs in August, as traders became increasingly confident that the next Federal Reserve move will be an interest-rate cut. Market volatility, as measured by the CBOE VIX Index, has fallen to benign levels around 15.

FIGURE 1: CBOE VOLATILITY INDEX (VIX)—PAST SIX MONTHS

Source: Cboe Exchange Inc.

CNN’s Fear and Greed Index, while below its peak for the year, remains firmly in “Greed” territory.

FIGURE 2: CNN FEAR AND GREED INDEX—YTD 2025

Sources: CNN, MacroMicro

What’s been driving the rally?

The rally has been underpinned by a mix of macroeconomic shifts, corporate strength, and investor behavior, each reinforcing confidence despite policy noise.

Cooling inflation and rising rate-cut odds

A key support has been a run of consumer inflation data consistent with gradual disinflation, which boosted market-implied odds of a September rate cut by the Federal Open Market Committee (FOMC). Combined with a disappointing July employment report and revisions to prior months, inflation data might prompt the Federal Reserve to finally lower rates. However, hopes for a half-point rate cut were tempered by last week’s producer price data.

Newsweek noted, “The Producer Price Index (PPI) rose by 0.9 percent on the month in July, the U.S. Bureau of Labor Statistics (BLS) said on Thursday, and by 3.3 percent on the year. Both were much higher readings than the markets were expecting.”

Earnings resilience—especially in mega-cap tech

Heading into earnings season, growth estimates were generally below 5%. Yet Q2 earnings have significantly beaten expectations.

Creative Planning’s Charlie Bilello recently reported, “Corporate earnings have continued to climb, with S&P 500 profits hitting another new high in the second quarter, up 11% year-over-year.”

However, he also noted, “With stock prices up over 20% in the past year, we are once again seeing multiple expansion. The price to peak earnings ratio for the S&P 500 has climbed to 26.7, over 50% above the historical median and at its highest level since 2000.”

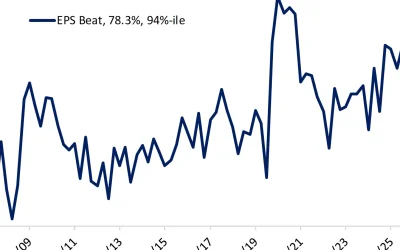

FIGURE 3: S&P 500 OPERATING EARNINGS PER SHARE—TRAILING 12 MONTHS

Sources: S&P Dow Jones, Creative Planning (Charlie Bilello)

Much of the earnings strength has come from large technology and AI-driven firms. Barron’s wrote that tech’s index share has swelled to record levels and that valuations in the group are rich—both a driver of gains and a source of risk.

Barron’s reported,

“This past week, tech accounted for a record 34.5% of the index’s total market capitalization of $54 trillion. That’s up from 32% at the end of 2024 and 20% in 2018.

“The current figure understates the true tech weighting because S&P Dow Jones Indices, which oversees the benchmark, categorizes Meta Platforms and Alphabet as communication services stocks. Add that pair to Amazon.com (classified as a consumer discretionary stock) and Tesla (an artificial-intelligence, robotics, and autonomous-driving play) and the ‘tech’ sector weighting is about 45%. …

“America’s tech leaders are dominant, with lucrative business models and wide moats. But the recent rally has raised risks, with tech stocks trading at an average of 30 times forward earnings and 10 times sales.

“Healthcare, energy, and financials are valued at closer to 15 times earnings. Ten times sales used to be viewed as an outlandish valuation, but Nvidia now trades for 20 times 2025 sales, and Palantir for almost 100 times.”

Retail participation and dip-buying

Barclays analysts estimate retail investors injected approximately $50 billion into global equities over a recent month, helping propel U.S. benchmarks back to highs after April’s downdraft.

MarketWatch commented in late July,

“But make no mistake, right now it’s the retail investors that are in control. That’s the conclusion from strategists across Wall Street. …

“Liz Ann Sonders, chief investment strategist at Charles Schwab, agrees. Since the April 9 closing low following the introduction of ‘Liberation Day’ tariffs, the best performers have been unprofitable tech stocks and heavily shorted stocks. She said on the Excess Returns podcast that those moves are evidence of ‘retail investor fingerprints.’ …

“JPMorgan analysts led by Nikolaos Panigirtzoglou say that retail investors, as well as corporate buybacks, are providing a backstop to markets.”

A macro ‘wall of worry’ that markets are climbing

Despite policy noise around tariffs and political uncertainty, analysts and the financial media have noted the market’s resilience. Investors appear to be more focused on earnings power and the policy path than on headlines.

The Financial Times observed last week,

“Stocks have staged a recovery from the turmoil that convulsed markets in early April, when Trump launched his trade war, as the fears of immediate damage to the global economy have receded. The extension of a US-China trade truce on Tuesday has also lifted investor sentiment.

“‘The wave of money that’s coming into the market just dwarfs all negative sentiment, especially for the AI boom,’” said Wee Khoon Chong, a senior strategist at BNY. ‘Obviously tariffs matter, but the influx of money matters even more when it’s such a large scale.’”

The strength of the rally has prompted some analysts to raise price targets for year-end 2025 and into 2026. Oppenheimer now cites an aggressive target of 7,100 for the S&P 500 in 2025, which Reuters called the highest among major Wall Street brokerages. Most other targets range from 6,400 to 6,900.

![]() Related Article: Today’s market calls for a multidimensional investment approach

Related Article: Today’s market calls for a multidimensional investment approach

Despite the one-way price action, prominent risks remain front and center

Even as markets climb, analysts warn that several risks could disrupt the rally.

Valuation and concentration risk

Analysts echo Barron’s point that tech’s weight in the S&P 500 is at a record and that many leaders trade at stretched multiples on forward earnings and sales. A narrow market leaves the Index more exposed to disappointment in a handful of names. While market breadth showed signs of improvement in the first half of the year, current signals are less encouraging.

Investopedia wrote last week, “Market breadth, a technical indicator used to measure market momentum, has declined since mid-July, and defensive sectors, like staples, have been advancing. The latter, [Fundstrat’s head of technical strategy Mark Newton] said, is what technical analysts tend to see before a correction.”

Macro and policy fragility

According to MarketWatch, analysts at Stifel have warned that the current market setup could produce a 14% pullback before year-end, citing elevated valuations, lingering inflation pressures from tariffs, and evidence of cooling activity in some macro data series. Their downside target stands around 5,500 on the S&P 500.

Fed path dependency

While softer inflation bolstered cut expectations, the hotter-than-expected July PPI temporarily lowered risk appetite. The Wall Street Journal said this was a reminder that the “last mile” of inflation can be bumpy and that the path of policy remains a swing factor for equities.

Geopolitics and tariff policy

The April sell-off was itself policy-induced, and renewed tariff iterations or geopolitical flare-ups could quickly reset the outlook for risk. The market remains vulnerable to headline-driven swings—especially related to the conflicts in Ukraine and the Middle East.

Main Street sentiment remains relatively weak

Retail sales have been stronger recently, but sentiment surveys suggest consumers remain cautious.

First Trust reported, “Consumers started the second half of the year on a good note, with retail sales rising for the second month in a row. The 0.5% gain in July slightly lagged the consensus expected +0.6%, but factoring in upward revisions to previous months, retail sales rose a solid 0.9%.”

However, MarketWatch noted that the first reading of the University of Michigan’s consumer-sentiment survey for August dropped to a three-month low of 57.2 from 61.8 in July. Surveys of Consumers Director Joanne Hsu said, “Overall, consumers are no longer bracing for the worst-case scenario for the economy feared in April when reciprocal tariffs were announced and then paused. However, consumers continue to expect both inflation and unemployment to deteriorate in the future.”

RECENT POSTS