Navigating the ‘trade-war market’ with active management

Navigating the ‘trade-war market’ with active management

Financial advisors share how their overall active management philosophy has handled months of wild swings in the market, as they strive to keep clients’ investment portfolios—and emotions—on track.

Financial advisors who use actively managed strategies are typically confident that risk will be mitigated for their clients during periods of market volatility.

But how have they—and their clients—handled the market’s wide swings, when it has bounced right back up after plunging 300 or more Dow points due to a presidential tweet or hints of favorable trade-deal talks between the U.S. and China? Or vice versa?

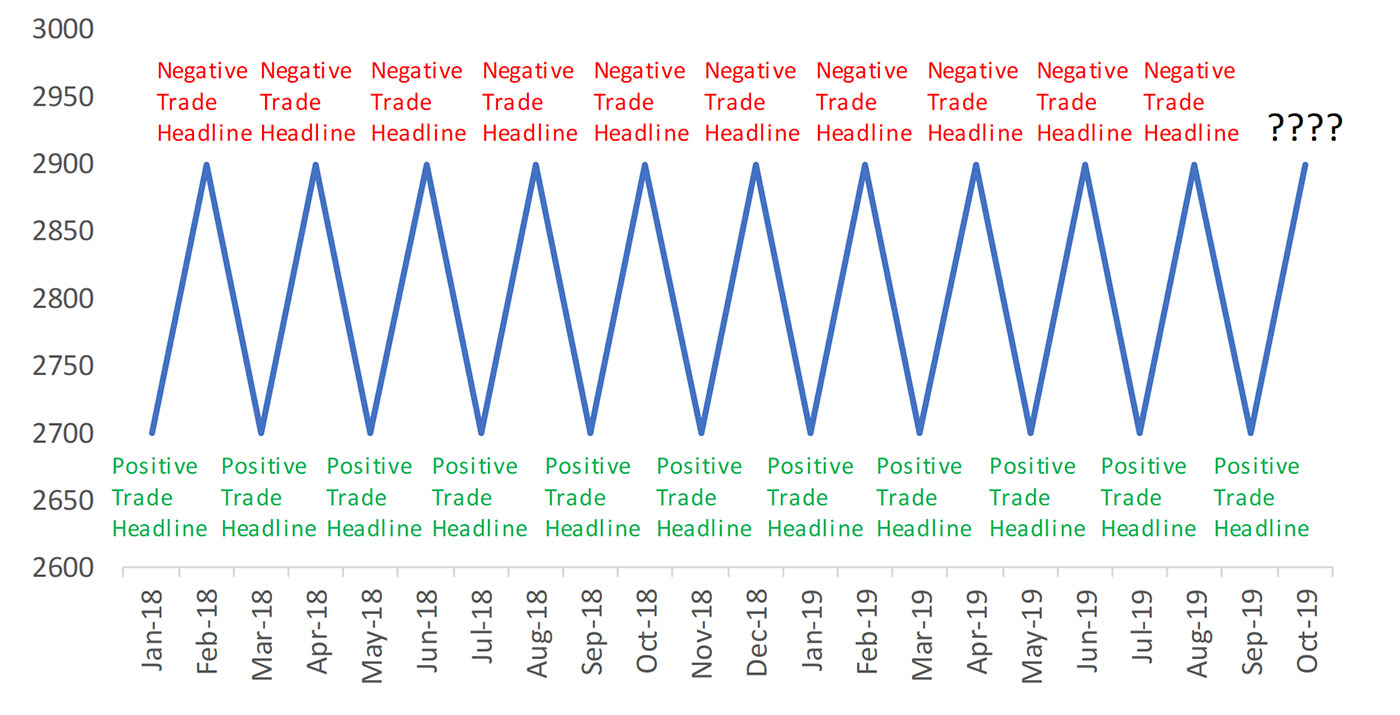

Highly regarded research and analytics firm Bespoke Investment Group half-jokingly put out the following chart in October showing the market’s behavior over the last 22 months.

Source: Bespoke Investment Group, 10/11/19

Depending on when and how trade talks are ultimately resolved, the market could go either direction—and in a big way!

If a market-calming China–U.S. trade deal is reached that buys time, forecasts of further gains of close to 15% in the market over the next 12 months are not uncommon.

However, more than one respected Wall Street analyst or fund manager has forecast a market plunge of 25% or more if the trade war with China moves to a higher level of escalation and further punitive tariffs come from both sides.

When you throw in the uncertainty of when the economy might take a downturn unrelated to the trade talks, taking the market with it, the recent volatility appears more threatening to many investors than would normal swings.

Three advisors recently spoke to Proactive Advisor Magazine about how the current market behavior relates to their overall active management philosophy—as they work to keep their clients’ portfolios and emotions above the turbulent waters.

Andrew Leithe, CFP, CEO

Marlton, NJ

Strategic Financial Advisors Corp. and Strategic Financial Services Corp.

“Currently, the United States and China continue the tug of war in negotiating a trade agreement. The question is, will the United States pull China through the mud, will China pull the United States through the mud, or will it be a draw and both sides will make concessions?

“While it is unclear what the ultimate resolution will be, we think the trade tensions will eventually stabilize or ease. The United States continues to demand fair market competition and trading policies, while China continues to hold out before the presidential election, in the hopes of putting more political pressure on Donald Trump. However, in the end, they both want to make a deal, and both sides will need to make sacrifices to reach an agreement. Until then, the markets are likely to experience a lot of short-term volatility.

“To navigate our clients through moments of heightened volatility like those we are currently experiencing, we think it is important to maintain a long-term investment approach and continuously review clients’ portfolio structures and risk profiles.

“In working with clients on their investment strategy, we stress the importance of maintaining a long-term investment approach. This allows their investments to compound over time while minimizing their tendency to overreact in periods of market volatility. Furthermore, it reduces the potential for mistiming the market by selling at market lows and crystallizing losses, and, alternatively, buying at market highs, making it more difficult to profit from an investment.

“When selecting tactical money managers, we utilize managers who share this same long-term investment approach and focus on the long-term health of the economies and markets while ignoring any short-term chatter. Managers who are utilized in our clients’ portfolios must go through a rigorous due diligence process and must demonstrate alpha generation through various market cycles. We select managers that are able to meet our clients’ return objectives while mitigating risk during longer and larger market corrections.

“To sustain this long-term approach, it is equally important that we help clients construct a portfolio that appropriately balances their unique return objectives and risk appetite. Clients who are accumulating assets typically have a higher level of risk, given that they have a longer time horizon. Retirees who are living off their portfolio alone, on the other hand, have a lower tolerance for risk. It follows that clients who are still building wealth can afford to be more aggressive in taking advantage of prolonged market declines by investing “drying powder” (excess cash) in equities, therefore increasing their market exposure. This often runs counter to an individual’s innate reaction, which may be to limit losses and reallocate money from risky to conservative investments in times of economic uncertainty.

“For clients who are utilizing their portfolio to meet their income needs and cannot afford to take on additional risk, we suggest that they maintain their current holdings during market turbulence. If a retiree does not have sufficient assets to produce an adequate level of interest and dividends to meet their income needs, we suggest they reallocate a portion of their riskier equity investments to conservative assets as the market appreciates to allow the client to weather a downturn as this probability increases. If their portfolio is large enough, I advise the client to distribute only interest and dividends to meet their needs. So, even if the market is trending down, they are not liquidating principal but rather living off the cash flow their portfolio is generating.

“Furthermore, regardless of the risk profile of our clients, we always advise clients to build a foundation within their overall portfolio with a mix of an emergency fund and conservative investments. This insulates the clients from immediate cash needs and the realization of losses should life events drive the need for large cash demands (i.e., job loss, unexpected medical expenses, and other catastrophic events).

“In summary, as an advisor providing guidance to clients, we must instill a long-term investment approach and provide guidance during moments of volatility to stay the course and not stray away from this investment style. For some clients, it may be appropriate to seek opportunities to invest while the market is trading at a discount. For others, it may be appropriate to take a few chips off the table while the market appreciates. This determination is all dependent upon the client’s individual portfolio structure, income needs, and risk tolerance.”

Steve Deppe, CMT, senior market strategist and wealth advisor

San Diego, CA

AlphaCore Wealth Advisory

“Our traditional strategy has been to identify the prevailing trends across asset categories, measured using both absolute and relative momentum, each and every month. This quantitative work then dictates our tactical asset-allocation decisions within portfolios.

“The key word here is month. The issue we’ve seen since the beginning of 2018 is the speed at which the market is now moving, making a month—what used to be a short period of time—seem like an eternity.

“There have been five periods since 2018 when the S&P 500 has declined by 5% or more in a matter of days. That’s causing shorter-term noise within a monthly-oriented system, which exacerbates emotions for investors—and even portfolio managers—and leads us to question whether we need to stick to the system or make a change.

“The way information is now disseminated into the marketplace has seemingly led to erratic markets. This has caused us to question whether our philosophy is no longer fast enough for the speed of the markets’ movements.

“We’re trying to take the long view, and discipline is the most important ingredient. We try to stick with an objective, quantitative process and not question why or when things need to change. But the last two years have left us with two choices: Do we stick with the strategy that earned for the long term, or do we alter the strategy to match the newfound market dynamics? Typically, the former is always better than the latter, because plotting a good course and staying the course is the best path to get where you’re going, rather than constantly changing the course.

“For us, the recent, chaotic, trendless climate has created a bit of pain with our monthly strategy, but hey—no pain, no gain. We prefer to stick to our strategy with maniacal discipline to earn the expected ‘gain’ of the approach, rather than only accept the ‘pain’ of the approach and then move on to a different approach.

“The volatility we’ve seen in the past 19 months and the characteristics exhibited in the equity markets made us increase our activity, especially in the fourth quarter of 2018 and the first quarter of 2019. Passive approaches worked well, relatively speaking, but for more active approaches, January didn’t feel so wonderful.

“Anytime we have a trendless climate like we’ve seen, the market will increase activity on a monthly rotational strategy. Increasing activity means increasing the frequency of buy/sell transactions on a monthly basis. For example, from March 2016 through September 2018, our strategy did absolutely nothing. Why? Because equities were in a persistent—and peaceful—uptrend. That uptrend vanished in October 2018, and we’ve since had transactions occur in October 2018, December 2018, January 2019, February 2019, and May 2019.

“The current volatility leaves the S&P 500 like a yo-yo spinning in place, but what I tell clients (and myself) is to maintain discipline—the way you behave in the present is what you can expect in the future. You don’t jump out of the plane because of turbulence, so you shouldn’t abandon a sound long-term investment strategy because of short-term volatility.

“If the U.S. makes a deal with China, from my perspective it will be a political win and nothing more. But any good news on the trade front will tend to move stocks higher, if for no other reason than the increased clarity it provides participants when attempting to discount the future for both earnings and the global economy.

“No matter how patient our clients say they are, no matter how long term they say they are, the volatility tends to tug at everyone’s emotions. As their advisors, it’s important to let our clients know that the volatility mostly is noise—and that exercising maniacal discipline with a prudent long-term investment strategy is always the best remedy to volatility.”

{kind=link}

Michael T. Kuczinski, CLU, ChFC, RICP, CFP, and principal

Millstone Township, NJ

Total Wealth Enhancement Group LLC

“The current volatility in the markets is like hanging onto a pull-up bar, but then suddenly you’ve got 200 feet below you—a second of hanging on that bar can feel like an eternity.

“With this volatility, we are more cautious than we normally would be, and we are moving positions to cash more quickly than we would have in the past during this point in a cycle.

“The talk of the trade war or a recession can dial the market up or down, and in a big way. The question is whether it will be a lasting move or like it’s been over the last year and a half, when the market went down heavily but then quickly recovered.

“That’s when active management really comes into play. You can say you are doing all of the active management you want, but you’re likely not making every call right on the money. You learn in hindsight that some moves weren’t the best decision that you could have made. True active management is key and the most beneficial when things go in a really bad direction—any shift in investment strategy to reduce risk allows clients to comfortably stay invested and not risk losing everything they’ve invested in the last seven to eight years.

“It can be very challenging in this environment trying to move things into and out of cash. The concern is that we may miss things going back up—or that we could ultimately end up losing money. Many times, I just like to stay put, as it’s more a matter of controlling the amount of decline rather than trying to avoid every decline.

“When we go back into the market, we use a little bit of leverage such as a leveraged ETF or a no-load mutual fund in a managed portfolio. Let’s say we moved into cash but the S&P 500 started going up again. Now, since we did not get right back in, when the market is clearly on firmer ground, many of our TPMs, or advisory accounts, will buy a leveraged ETF fund that returns 1.5 times whatever the S&P 500 is doing. This can allow the client to catch up faster when the market is doing well.

“I think the bull market is still intact, and if there is a deal with China, the bull market will continue. But regardless, at some point, the market will change again, as it’s done throughout the history of capitalism.

“Hardly anyone says we’re in the first or second inning—almost everyone says it’s more like the seventh or eighth inning. So, we’re getting close to the point when the market will experience a good-sized correction—i.e., a bear market.

“When it comes to doing things now, any new money is going into low volatility, stable, and/or high-dividend-paying types of strategies, and we’re going to avoid riskier highfliers.

“As far as communicating with clients, we want them to understand that we’re taking care of their portfolio in the right way. We’re managing risks to put them in the position that if the market is going to do well, then the clients have the opportunity to participate in that move to the upside. However, if the market is going to do terrible, we are actively managing those risks with a goal that nobody is going to have to have to start worrying about their financial future.”

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

Securities and investment advisory services are offered through FSC Securities Corporation (“FSC”), member FINRA/SIPC. Additional advisory services are offered through Strategic Financial Advisor Corp. and Strategic Financial Services Corp. FSC is separately owned, and other entities and/or marketing names, products, or services referenced here are independent of FSC. Address: 701 Rte. 73 South, Suite 125, Marlton, NJ 08053. Phone: 856-983-1001.

AlphaCore Capital LLC is an investment advisor firm located in La Jolla, California. AlphaCore Capital LLC and its investment advisor representatives are in compliance with the current registration requirements imposed upon registered investment advisor firms by those states in which we maintain clients. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital.

Total Wealth Enhancement Group is an independently owned and operated registered branch location of Garden State Securities Inc. (GSS). Securities are offered through GSS, member FINRA/SIPC. Advisory services offered through Garden State Investment Advisory Services LLC, an SEC registered investment advisor. Insurance products offered through Garden State Insurance Agency Inc.

Certified Financial Planner and CFP are trademarks or registered trademarks of The Certified Financial Planner Board of Standards Inc. Chartered Life Underwriter, CLU, Chartered Financial Consultant, ChFC, Retirement Income Certified Professional, and RICP are registered trademarks of The American College. CMT and Chartered Market Technician are registered trademarks owned by CMT Association.

Katie Kuehner-Hebert is an award-winning journalist with more than three decades of experience writing about financial services. She has expertise in banking, insurance, financial planning, economic development, and employee benefits. Her work has appeared in many leading publications.

Katie Kuehner-Hebert is an award-winning journalist with more than three decades of experience writing about financial services. She has expertise in banking, insurance, financial planning, economic development, and employee benefits. Her work has appeared in many leading publications.