‘Buy and hope’ investing versus active management

‘Buy and hope’ investing versus active management

When running the market gauntlet over the long term, there are two vastly different options: purely passive investing or using a professionally managed account that employs active, risk-managed strategies.

From our clients’ point of view, there are at least two choices of buy-and-hold strategies. The first we call “buy and hope” investing—acquiring a portfolio of stocks, bonds, or mutual funds and then passively holding on to them through all of the vicissitudes of the market. The other is committing to an actively managed account run by a professional advisor. Both require a long-term commitment to work.

Let’s see how they differ to help you determine which type of buy-and-hold investor you would rather be.

There is an allure to buy-and-hold investing—just invest and then forget it. Passive, “buy and hope” investing is for many a matter of faith—a secular faith that over time a well-diversified investment portfolio will appreciate in value regardless of the short-term market volatility. However, for that faith to have even a chance to be borne, two requirements must be satisfied that often are not focused on by “buy and hope” investors.

First, it assumes that you invest for a very long time. Last century, the time horizon required to have a 100% chance of achieving a profit was more than 20 years. And that brings up the second requirement: that you won’t need to use the funds invested throughout that waiting period. Unfortunately, that need can and often does surface when the market is falling.

Over 35-plus years on the financial-management scene, we have seen few investors who could live with either of these requirements, let alone both. But for those who can, the market has rewarded them with the following advantages:

- When the market cycle bottoms and then moves to a new market top, the average gain in the S&P 500 Index (since its inception) has been about 177%. Those invested in an index fund tracking the S&P 500 would secure nearly all of that gain.

- While not as big of an issue for those investing in a tax-deferred retirement account, the “buy and hope” investor can be tax- and cost-efficient.

- When the markets are especially volatile but still maintaining a bullish tilt, if you can grit your teeth and hold on, you can come out the other side with a gain … as long as one of those volatile downswings doesn’t turn really ugly and become another bear market crash.

That, of course, brings up one of the chief disadvantages of “buy and hope” investing—the suffering inflicted by a bear market.

One has had to invest for more than 20 years to achieve a “buy and hope” profit over the last 100 years because when these bear market crashes occur, it can take a very long time to return to breakeven, let alone acquire a decent profit.

The occurrence of two of these bear markets in the last decade resulted in a “lost decade” for most investors. As Figure 1 shows, even if you focus only on the most recent bear market (2007–2008), it took an investor in the S&P 500 over five years to break even from the market top of 2007.

A “buy and hope” strategy has no room for anticipating or even reacting to a bear market. You simply suffer through it. Of course, human nature being what it is, when the average investor is faced with a 20% to 70% loss, somewhere along the way they throw in the towel and give up on the strategy. Then, once the bottom is reached, they are not invested to benefit from any gains generated on the way back up.

Now, you will recall that we said the best way to participate in a “buy and hope” strategy is with a well-diversified investment portfolio. That’s how “buy and hope” investors try to hold down the losses so that they can stay invested. But realize that by doing that, they cannot achieve the more than 100% gains that a stock index might average in a rally from a market bottom. Most of the holdings in well-diversified portfolios will gain less and some will fall in value. As a result, just as the losses are more moderate, so, too, are the gains.

This is why comparing your returns to a stock market index such as the S&P 500 makes no sense at all. No serious investor would risk all of their money in a portfolio made up solely of such an index and expose themselves to the 50%-plus losses experienced during just the last two market crashes.

Source: macrotrends.com

While a “buy and hope” investor must substantially reduce returns as he or she relies upon diversification as their sole way of dealing with risk, buying and holding a managed account with a registered investment advisor provides additional risk-management tools. The advisor can be responsive to the markets’ directions, capturing uptrends and avoiding downtrends, employing stop-loss tools and using many active strategies in a strategically diversified portfolio of strategies, not just asset classes.

But just as diversification reduces the “buy and hope” investor’s returns, and market crash environments can devastate a portfolio and challenge the sustainability of a client’s commitment to the “buy and hope” strategy, there are market environments that are not favorable to active investing. For example, few strategies can generate buy signals at the bottom—ground zero of a market rally. Therefore, they will often trail a “buy and hope” portfolio’s return when measured from that point in time forward.

In a different environment, where the markets are captured by conflicting news events that quickly buffet them from downdrafts to updrafts, active investors will get whipsawed and show small losses for the duration.

The European crisis a few years ago brought on such a market. One day the news from the continent was good and stocks soared; then the latest “solution” fell through and prices plunged. The latter part of 2018 was another such example, with a volatile market rising and falling on the latest news out of Washington, the status of various trade deals, and the market’s anticipation of the Fed’s next move on interest rates.

Despite this, by focusing on reducing losses during those market crashes where the “buy and hope” strategy is so vulnerable, the active manager can outperform even the market index—over a complete market cycle. In other words, over the same “long run” that is necessary for the “buy and hope” approach to work.

Here’s a simple way to illustrate this. Back in 1998, our firm began offering an active, multiple-strategy program for non-401(k) accounts—Strategic Solutions. Among the strategies offered were one pure bond and one mostly equity mutual fund trading strategy. The rest of the offerings were specialty or niche products. To test our proposition, let’s create a portfolio with 50% of the bond strategy (Managed Income, or MI) and 50% of the stock strategy (Evolution II, or EV II). Both strategies are still offered at Flexible Plan.

How did they do during the “lost decade” and its aftermath?

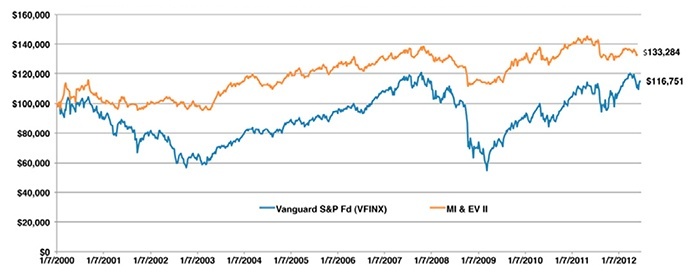

As Figure 2 shows, the managed strategy portfolio (MI & EV II) did pretty well—outperforming the S&P 500 Index fund. (You can’t invest in an index; you have to use a fund, and funds have costs. This example reflects the performance of what has always been one of the least expensive S&P 500 Index funds). This performance was accomplished even after maximum advisory fees on a $100,000 account. The two strategy returns used to construct the managed account portion of this chart (MI & EV II) are taken from actual accounts—none of them are hypothetical.

This brings up another point. Remember that one of the advantages of the “buy and hope” strategy is that you can use low-cost index funds. Conversely, a disadvantage of active investing is that you must use the more-expensive funds that allow more active trading. Yet, here we have one of the lowest-cost index funds compared to our higher-cost actively managed portfolio of strategies and, as the French would say, voilà—the higher-cost funds with active management perform better.

Source: Flexible Plan Investments Research. Actual results after all advisory fees and fund costs. Growth of $100,000.

Let’s point out a couple of facts that may not be obvious just looking at Figure 2. The first is the maximum loss that an investor was exposed to in the two approaches. The “buy and hope” approach experienced a 54.7% loss. Even though the managed account outperformed, its investors were only exposed to a maximum loss of 17%. Which better served the purposes of an investor who needed their investment funds in the short run, rather than the long run?

Also, investment professionals often talk these days of alpha—the extra return that you achieve for the risk taken. The “buy and hope” investor achieved none, while positive alpha was captured by the managed account holders in this difficult market period.

Lastly, remember that one of the advantages of the “buy and hope” strategy is that it will perform better in advancing markets because, obviously, it is fully invested during all of that advance.

We checked the returns of the index fund versus the managed accounts for each of the 13 years shown.

You know what? The index fund beat the managed account portfolio in every up year. And the managed account portfolio of strategies outperformed the index fund in every down market year. At the finish line, which came out ahead?

Today’s actively managed investor must carefully pick his or her way across the financial market minefield to avoid stepping on a live one—the next market crash. The “buy and hope” investor just charges across the minefield because it is assumed that they can withstand the risk.

And that’s what the choice between the two buy-and-hold approaches comes down to, isn’t it?

One seeks to make sure you make it to the other side; the other assumes you can pull together the pieces after the market explodes and somehow carry on. Underperformance in up markets versus near ruin in down markets—what will it be the next time you’re searching for an investment strategy?

Which type of buy-and-hold investor would you rather be?

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

This article is an abbreviated and updated version of a white paper by the founder and president of Flexible Plan Investments Ltd., Jerry Wagner, in July 2012. The original version can be found here.

Since 1981, Flexible Plan Investments (FPI) has been dedicated to preserving and growing wealth through dynamic risk management. FPI is a turnkey asset management program (TAMP), which means advisors can access and combine FPI’s many risk-managed strategies within a single account. FPI’s fee-based separately managed accounts can provide diversified portfolios of actively managed strategies within equity, debt, and alternative asset classes on an array of different platforms. FPI also offers advisors the OnTarget Investing tool to help set realistic, custom benchmarks for clients and regularly measure progress. flexibleplan.com