Impact investing and active management are not mutually exclusive strategies

Impact investing and active management are not mutually exclusive strategies

Financial advisors can apply the discipline of risk management within active strategies that focus on impact investing.

Impact investing, also known as socially responsible investing (SRI) or sustainable investing, and active management can go hand in hand to address a more holistic view of clients’ investment priorities, say financial advisors and investment managers who adhere to both strategies.

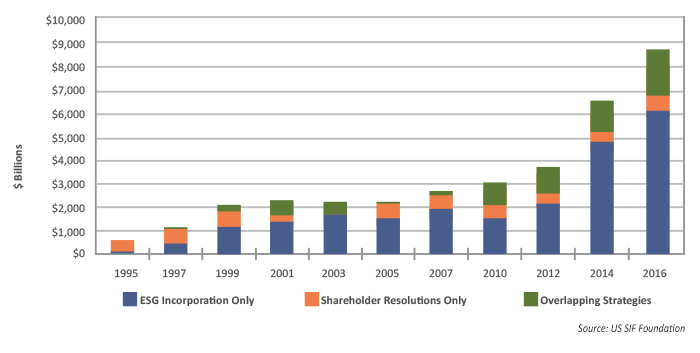

The demand for impact investing is growing. Investment firms now consider environmental, social, and governance (ESG) factors across $8.72 trillion of professionally managed assets, a 33% increase since 2014, according to the 2016 “Report on US Sustainable, Responsible and Impact Investing Trends” by the US SIF Foundation. These assets now account for more than one out of every five dollars under professional management in the U.S.

The US SIF Foundation’s 2016 research identified the following:

- At the beginning of 2016, $8.10 trillion in U.S.-domiciled assets held by 477 institutional investors, 300 money managers, and 1,043 community investment institutions applied various ESG criteria in their investment analysis and portfolio selection.

- $2.56 trillion in U.S.-domiciled assets were held at the beginning of 2016 by 225 institutional investors or money managers that had filed or co-filed shareholder resolutions on ESG issues at publicly traded companies from 2014 through 2016.

- Eliminating double counting of assets involved in both strategies, and for assets managed by money managers on behalf of institutional investors, results in the overall total of $8.72 trillion at the beginning of 2016.

One firm offering impact investment alternatives is Pax World, which in 1971 launched the first socially responsible mutual fund in the country and is widely considered a leader in the field of sustainable investing (the full integration of ESG factors into investment analysis, security selection, and portfolio construction). (See Proactive Advisor Magazine article, “Impact: The next stage of sustainable investing,” by Joseph Keefe, president and CEO of Pax World Management LLC.). At the end of 2016, Pax World advised funds with roughly $4.1 billion in assets under management for individuals, financial advisors, and institutional investors.

Mr. Keefe acknowledges in his article that the world of sustainable, impact investing has come a long way but still has much room for further evolution and growing sophistication. SRI strategies are increasingly used by demanding investors who want performance and risk management in equal doses with social responsibility.

“Investing is no longer about style boxes. In the period ahead, it will increasingly be about goals, and about solutions. It will not be just about equities versus fixed income, or large cap versus small cap, or core versus value versus growth, or correlated versus noncorrelated. …

“Today, if we want to serve investors, we need to address the question of trust and the related issue of risk—which is always at the heart of investing. One way to do that is to speak to investors’ goals, which go beyond diversification and asset allocation. Their goals ultimately involve the way they want to live and what they want to accomplish—and how their money relates to that. While there is no single answer, I think sustainable investing, particularly as it enters its next stage, can be part of the solution.”

Flexible Plan Investments, Ltd., which uses Pax World funds, is an example of an investment management firm that incorporates active management tools and risk management. Its For A Better World strategy applies a “proprietary risk-managed allocation methodology to a universe of socially responsible funds. … Tested on a parallel style of funds back to 1972, For A Better World has a time-tested history since 1998 as an effective investment management strategy that hasn’t forgotten the planet.” The strategy family has several actively managed features, including (a) a dynamic, quantitative methodology for fund ranking and exposure; (b) the ability to move 100% to cash; (c) the availability of inverse/short funds; and (d) different risk exposure profiles responsive to investors’ specific needs.

Globally, the amount of assets being professionally managed under responsible investment strategies in 2016 rose 25%, to $22.89 trillion, from 2014, according to the Global Sustainable Investment Alliance. More than half of U.S. retail investors say ESG factors will be increasingly important to them in the next five years, as a growing number of empirical studies show a positive relationship between ESG factors and corporate financial performance, according to a State Street March 2017 report, “The Investing Enlightenment: How Principle and Pragmatism Can Create Sustainable Value through ESG.”

“Financial advisors should be prepared with concrete solutions for these investors, which are only set to grow,” wrote the authors of the State Street report, Robert G. Eccles and Mirtha D. Kastrapeli. The goal of the research, they said, “was to provide a pragmatic approach to ESG integration that delivers on the principle of sustainable value creation through risk-adjusted returns.” As part of their findings, they saw ESG factors becoming increasingly recognized by institutional investors as important “signaling tools for volatility and risk.” They also found that retail clients increasingly say they want more information about ESG investment options from their financial advisors: 83% of respondents said that they researched ESG investing on their own, with only slightly more than a third saying their advisor was the source of information on the topic.

50% of retail investors want their advisor to communicate more about ESG investing

— State Street, “The Investing Enlightenment”

Lay incorporates impact investing into active portfolio management by using active managers who are skilled at conducting the appropriate research and who may offer several different investment options that incorporate SRI or faith-based parameters.

“As an Accredited Investment Fiduciary, I have the primary focus of recommending what is in my clients’ best interest,” he says. “There are several factors that pertain to making that recommendation, and a client’s values and goals are paramount in that process.”

Lay believes that active management and impact investing are not two mutually exclusive goals, but that they both can work well together when properly balanced. Market conditions, he says, typically determine the direction and overall tactical adjustments to the overall portfolio; investment strategists can actively manage those SRI and faith-based elements representing either a portion of or the entire portfolio.

“You can also have a portion of the portfolio actively managed and a portion in more of the traditional investment models,” he says. “Each strategy and each client may have different goals and objectives, and you can achieve those utilizing any number of methods.”

The impact investing space is growing in awareness, and there are several good platforms that offer SRI and faith-based investments, Lay says. “If you don’t currently offer SRI or faith-based options, my question would be why not? We have a duty to know what is out there and to be able to address the needs of our clients and future clients,” he says. “Ask questions! If you don’t ask your clients if SRI or faith-based investing is important to them, chances are they don’t even know it’s an option.”

Divam N. Mehta, CFP, ChFC, and founder of Mehta Financial Group, LLC, in Glen Allen, Virginia, says his team incorporates impact investing within the firm’s investment policy guidelines in the interest of meeting his clients’ specific interests and fostering strong client relationships. His team does not view impact investing as a different asset class, but rather a varying component to the investment strategy itself.

“For example, if the client is comfortable with a specific asset-allocation model, then we strive to find SRI investments that will meet the strategic asset class,” says Mehta. “If this is not possible, then we use either individual equities, ETFs, mutual funds, or sectors to complete the asset-allocation model.”

Advisors who adhere to active management strategies should remember that clients who desire impact investing ultimately do because of philosophical viewpoints, and not necessarily for the highest returns, he says. “With this in mind, it is important to consider that chasing the highest returns is not the end goal for many clients who want to participate in impact investing,” Mehta says. “Many clients would prefer to invest with their conscience rather than striving for the highest returns possible.”

However, Mehta does not believe that active management and impact investing are necessarily mutually exclusive. “You can definitely have both aspects of wealth accumulation accompany one another,” he says. “Moreover, risk is subjective from one client relationship to the next.”

During the discovery phase of the relationship, Mehta and his team discuss the risk parameters of all investment strategies that they will develop for the client. Once the risk parameters have been quantified and established, the team will often begin to build the portfolio with SRI investments as an important component. “We always err on the side of caution when it comes to SRI investments in the portfolio—meaning we will take a conservative approach rather than add a position that might push the risk parameter to an unwanted level,” he says.

If a client decides that SRI investing is a strategy he or she wishes to strongly pursue, the team will generally build a custom portfolio that is in line with their philosophical views, Mehta says. “The process and mechanics of the portfolio usually will not change,” he says. “We will continue to make tactical and active changes to the portfolio based on market performance and/or external factors, along with periodic rebalancing.”

The presence or absence of an SRI investment strategy should not alter this process unless requested by the client. The idea, he says, is to incorporate his firm’s dedication to the principles of risk management, diversification, and tactical portfolio management with all client portfolios. SRI investing and active management, he believes, can coexist well in that context, and all client portfolio strategies, he says, “are founded in ongoing quantitative and qualitative analysis.”

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

This article first published in Proactive Advisor Magazine on June 15, 2017, Volume 14, Issue 9.

Katie Kuehner-Hebert is an award-winning journalist with more than three decades of experience writing about the financial-services industry. She has expertise in banking, insurance, financial planning, economic development, and employee benefits. Her work has appeared in many leading publications.

Katie Kuehner-Hebert is an award-winning journalist with more than three decades of experience writing about the financial-services industry. She has expertise in banking, insurance, financial planning, economic development, and employee benefits. Her work has appeared in many leading publications.