Options provide a layer of tools beyond the “buy it, short it, or stand aside” choices available when limited to plain vanilla stock plays. The added dynamism created with options can be used to ward off risk, as well as to bring in extra income. With options, you are only limited by your imagination and, of course, liquidity.

One risk-management tool that uses options is called a conversion, or collar, strategy. This strategy combines puts, calls, and a long position in an underlying stock or ETF. (The collar strategy can also be used for bonds, futures, or any investment vehicle that has options.) This approach can lock in a final sale price for the security, usually limiting potential upside on the position, but offering protection in the event of a pullback. If you are clever, it is also possible to collect the dividend on the issue while waiting for the options to expire.

Here is how it works.

Say you are long a stock at $10 a share. The stock pays a quarterly dividend in April, July, November, and February. You buy the April put and sell the April call both with a strike price of $10.

The put is a short-term insurance contract that gives you the opportunity to sell the stock at $10; the call gives the buyer of the call the right to buy the stock from you in April for $10. Basically, you are out of the stock in April.

This is about the closest thing you can get to a riskless strategy. One potential issue is that the stock can be called from you before the dividend is paid because it likely is an American-style option. What is an American option? One that can be exercised at any time before expiration. A European-style option can only be exercised at the expiration date, though it can be bought or sold at any time up to expiration.

This conversion or collar strategy caps any upside you might have gotten, but it also caps the downside. And, yes, you get the dividend (so long as the strategy expires after the dividend is paid).

Let’s use Cisco Systems (CSCO) as an example.

The stock was trading at $52.43 on May 15, 2019, and pays a dividend of $0.36 in July. Assume you are long 100 shares of CSCO. You could buy the August 52.50 put for $1.88, and you could sell the August 52.50 call for $1.80. (As for the cost of the options, all figures must be multiplied by 100, so an option quoted at $1.80 has an actual cost of $180.)

This entire transaction will cost you $0.08 ($8.00) plus brokerage commission, which can be very reasonable if you use the right trading platform. You will receive a $0.36 dividend on the stock plus $0.07 profit on the share minus commission.

An alternative to this approach would be to buy a lower strike put for protection while simultaneously selling a higher-priced call, allowing for more potential upside profit. While this alternative is completely acceptable, there is a trade-off for the greater profit potential: greater risk with the put at a lower strike price. Remember, the put is a short-term insurance policy on the underlying stock or ETF, paid for with the premium from selling a call.

Why would you want to do this when the transaction offers a relatively modest return?

If you have been in a position in a stock or ETF for some time and have a profit on the position, you are able to generate additional dividend income while protecting your position’s profit. This might be especially attractive if your stock or ETF has seen significant price appreciation and the overall equity market is in the mature phase of a bull market—as it is now.

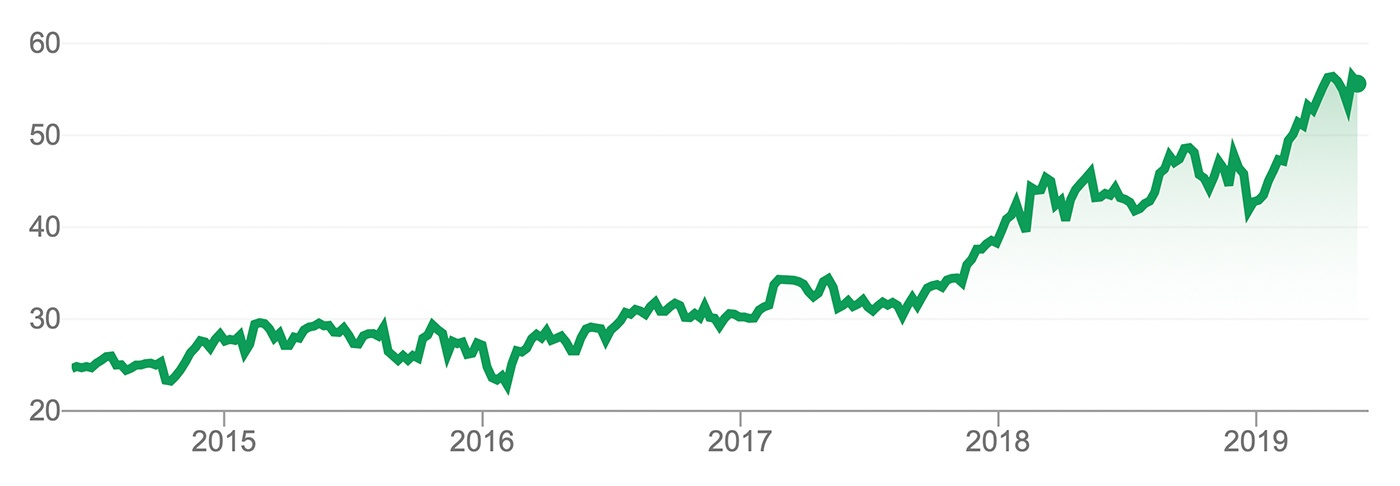

In the case of CSCO, the stock has shown significant growth over the past three years, moving from under $30 to over $50.

Source: Nasdaq.com

While CSCO is a good example of a stock where investors may hold a significant profit they wish to protect, the dividend yield is not particularly attractive. The same conversion or collar strategy can obviously be used for stocks or ETFs with much higher yields. Verizon Communications (VZ) is one such stock. It has shown price appreciation over the past year from the $45 range to about $58, and it has a dividend yield of over 4%.

This is not rocket science! Using a simple options strategy can protect investors from downside risk at a minimal cost and can provide a relatively risk-free profit.

(Note: The author does not hold positions in the stocks mentioned.)

Jeanette Schwarz Young, CFP, CMT, CFTe, is the author of the Option Queen Letter, a weekly newsletter issued and published every Sunday, and "The Options Doctor," published by John Wiley & Son in 2007. She was the first director of the CMT program for the CMT Association (formerly Market Technicians Association) and is currently a board member and the vice president of the Americas for the International Federation of Technical Analysts (IFTA). www.optnqueen.com

Jeanette Schwarz Young, CFP, CMT, CFTe, is the author of the Option Queen Letter, a weekly newsletter issued and published every Sunday, and "The Options Doctor," published by John Wiley & Son in 2007. She was the first director of the CMT program for the CMT Association (formerly Market Technicians Association) and is currently a board member and the vice president of the Americas for the International Federation of Technical Analysts (IFTA). www.optnqueen.com