Knowing when to worry about your investment strategies

Knowing when to worry about your investment strategies

Indicators flashed danger signals on stocks last quarter, prompting headlines that asked, “Is it time to worry?” What does that mean, exactly? Will lying awake nights improve investment performance? Is “worry” something we can turn on and off? And what good does it do to worry after the market has already begun to decline?

Investment managers are all too familiar with the two top rules of investing: Rule #1—Don’t lose money. Rule #2—Don’t forget rule #1.

In keeping with these rules, one of the core objectives of active investment management is to strive to protect the value of a portfolio during market declines. There is, of course, no magic formula for risk management with inherently risky assets, so managers employ a variety of techniques.

Risk, however, is a slippery creature that doesn’t always give precise, actionable warnings and often gives false ones. You would expect that active risk management has to involve being on continual alert—and the everyday word for this is “worry.” But how much do we know about worry and how to manage it?

The notion that an active manager can somehow rely on their innate ability to “know when to worry” or to know when significant declines are about to occur is a bold statement—supported by little evidence beyond the anecdotal reports of investment managers who speculated that a decline was coming and just happened to be right.

Of course, there are more “flavors” of active investment management styles than one can imagine: fundamentalists versus technicians, value versus growth, managers who specialize in one asset class versus “go anywhere” managers, trend followers versus contrarians, alpha seekers versus those with a more conservative risk-management style, stock-pickers versus holistic portfolio managers, or those using traditional asset classes versus others in the alternatives space. Perhaps one of the biggest differentiators is the degree to which an active investment manager uses “manager discretion,” ranging from those with wide latitude to strict, rules-based managers.

No matter what type of investment manager we are talking about, they will have their own distinct “worry points.” The aggressive alpha seeker making large “bets” will have to possess a greater risk tolerance, suffer larger drawdowns at times, and will worry about steep losses if their core thesis is wrong. The more conservative, rules-based risk manager may be able to significantly mitigate market losses but will likely worry about underperformance in raging bull markets or getting “whipsawed” by sudden trend changes. The most disciplined manager using time-tested models and algorithms recognizes that even the most sophisticated strategy “works until it doesn’t.”

There are numerous indicators that investment and portfolio managers watch, and these do provide valuable clues. But they will never tell you exactly where or when a sell-off may occur, or its magnitude. In addition, there are always indicators that don’t agree and there are numerous false positives. What’s more, people are highly prone to misinterpret statistics, and a common behavioral flaw is to infer things from market indicators that are not scientifically valid.

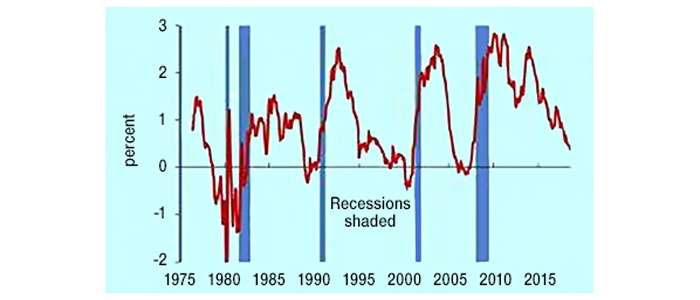

Take the yield curve for example. An inversion on the two-year and 10-year Treasurys has preceded every U.S. recession since 1971 (Figure 1). Sounds convincing, doesn’t it? But it also gave several false signals, didn’t always lead to bear markets even when it did invert, and preceded recessions by time periods ranging from several months to two years. A statistician would ascribe little confidence to such an indicator. I have yet to see anyone demonstrate that a specific action taken every time the yield curve inverted would have reliably yielded positive alpha in a broad portfolio.

Source: Forbes, Dr. Bill Conerly article, based on Federal Reserve data, July 2018.

The common retort to this would be that most active investment managers don’t rely on a single indicator. They weigh a confluence of indicators and use that to make decisions based on either their models or their experience and their overall sense of the risks at any point in time. Unfortunately, for discretionary managers, this now injects the totally unscientific notion that some people have a bona fide sixth sense about when to buy and sell stocks. The number of notable managers that have historically exemplified such a skill (like Bill Miller, Peter Lynch, and Warren Buffet) is so small within the total universe of managers as to be quite low in statistical terms.

That leads back to the original question of how worrying fits into all of this.

A brief look into the concept of worry reveals that as with concepts such as happiness, greed, and fairness, worry is much easier to describe than to specifically define, and pretty much impossible to measure.

The consensus among common definitions suggests that normal worry is our brain’s way of raising questions about potential danger, harm, or threat and is usually associated with a specific situation. If, for example, you are worried about missing an upcoming flight due to traffic, you weigh the risk of a missed flight against alternative measures such as leaving your home earlier or taking public transportation. You rationally think through that decision and then either take one of the alternative actions or simply decide you are already planning to leave in plenty of time and that, even with a little traffic, it is not going to be an issue. Worry over.

Implicit to this view is the idea that you actually can control low-level worrisome thoughts to some degree by either addressing them or simply thinking through them and dismissing them. Given the risks involved in stocks, a little worry is bound to be a normal everyday activity for an investment manager or financial advisor as new information rolls in about specific securities or the market in general.

Returning to the flight analogy, it is now the morning of your trip. You required more time to pack than you thought. You are now on your way to the airport, and you find yourself sitting in the rain with heavy traffic. Making your flight is now in jeopardy, and there is an acute sense of urgency. Your subconscious takes this information and turns your low level of worry into something decidedly different. You are nervous, upset, and anxious, and you have very few options. You pull frustratingly into the valet parking area, which will cost you far more than the economy lot, and you make a dash for the gate.

Your worry has now expanded from your brain into a more robust physical reaction psychologists classify as stress or anxiety. You are feeling physically agitated and compelled to do something. The only something available is now the expense of valet parking, so you bite the bullet. At this point, you might still consider yourself to be worried, but your worry has different characteristics. Among other things, it is now very difficult to entertain the option of deciding simply not to worry about it.

Psychologists view worry as a cerebral or cognitive function, essentially a state of concern, analysis, questioning, and risk assessing—activities that are normal and physically benign in most situations. The important distinction between worry and stress occurs when the brain goes into defensive mode, sending chemical signals to other parts of the body. These chemicals do not distinguish between missing a plane, watching a stock go down, or seeing a bear running toward you.

Once released, the hormones and other chemicals that characterize a stress response will run their course. The transition from worry to stress tends to occur subtly and with great speed. And once a worry escalates to a stress, it cannot easily be dismissed as a nonissue. Your subconscious perceives it as a threat. At this point, when decision-making skills are needed most, the notion that you might be able to “know when to worry” becomes moot.

The fact that everyone reacts differently to both worry and stress means there are no universal solutions to when they occur. Even financial professionals such as investment managers or financial advisors may not be able to predict how they will feel in stressful situations. What we do know is that the option to dismiss the issue completely (i.e., not worry about it at all) is likely going to have evaporated for many people at this point. Some may even have passed from worry into stress, making a dismissal of the issue all but impossible.

Worry is a natural human mechanism. It is the product of our brain’s evolution that protects us by continually wondering whether we might come to harm in some way. It is the continuous and subliminal work of our internal sentry, keeping us alert to things that might affect our survival. Psychologists don’t see worry as a problem until it gets excessive or chronic (which may deserve treatment), or until it escalates into stress, whereupon it threatens our health.

The investment manager’s or financial advisor’s concern about worry is quite different. A little worry must be expected at almost all times.

How a financial advisor can get ahead of ‘the worry curve’

Within their relationships with third-party investment managers, what steps can a financial advisor take to alleviate their own personal worry, allowing them to speak with a greater deal of authority and confidence to their clients when stress and volatility inevitably crop up in the markets?

- It starts by conducting extensive due diligence in the selection process of third-party investment managers. Do you have a strong comfort level in their infrastructure, reporting, management team, and services?

- Are they primarily rules-based in trading and strategy implementation or do they have wide latitude for manager discretion? Do you understand the parameters in either case?

- Is their track record compliant with the Global Investment Performance Standards (GIPS) and can it be verified? Can they provide you with audited figures?

- As you work with the manager over time, do their strategies perform generally as expected in different market conditions? If not, can they provide detailed explanations as to why not? Are they proactive in discussing variations from expected performance? Do they continually refine their strategic development process?

- Is a knowledgeable resource at the management firm available when needed to answer specific questions concerning performance?

It’s a serious challenge for any investor to determine just how to protect against downside risk without sacrificing too much upside or risking whipsaw trading during recoveries. Just as problematic is trying to devise precautionary actions before declines occur.

If there were easy answers to risk management, we wouldn’t need active investment managers and their sophisticated methodologies.

To cloud the picture further by trying to decide “when it’s time to worry” and when it’s not is a foolish premise. My advice to financial advisors and their clients is to ignore the financial news headlines and focus on making their decision process as sound, objective, and replicable as possible. If you work with a third-party investment manager, make sure you first fully understand and have confidence in their process—and then trust that process until you have evidence to the contrary. When performance questions arise, communication between all parties is paramount—not worry.

Richard Lehman is an adjunct finance professor at Cal Poly. He specializes in behavioral finance and financial derivatives, and has authored three books. He has more than 40 years of experience in financial services, working for major Wall Street firms, banks, and financial-data companies.

Richard Lehman is an adjunct finance professor at Cal Poly. He specializes in behavioral finance and financial derivatives, and has authored three books. He has more than 40 years of experience in financial services, working for major Wall Street firms, banks, and financial-data companies.