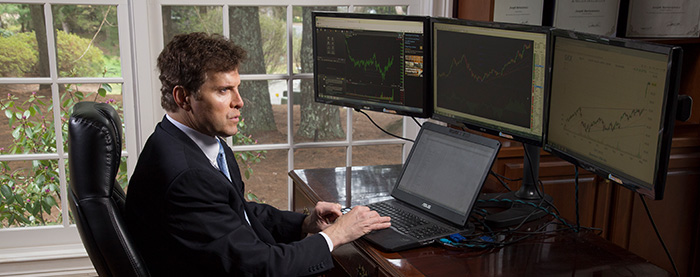

Technicals tell the story

Technicals tell the story

Joseph Bartosiewicz • Avon, CT

SagePoint Financial

Read full biography below

Applying technical analysis to risk-managed portfolios.

I bring a very technical and quantitative approach to the analysis of market trends and various sectors within different asset classes. My client focus is based on the suitability for a specific client’s planning and investment needs. This provides another advantage for my clients, as I am able to offer deep insight and appreciation for the sophisticated models and analysis used by outside strategists and third-party managers.

I take an analytical assessment of my clients—I want to dig deep to understand their investment style, in addition to their investment goals and needs. What is their personality type? Are they an analytical type of individual? Maybe this is an individual who needs to receive a lot of information and wants to get into the details of every strategy we use. Or are they an expressive type who doesn’t want the details but is comfortable with bottom-line information? If they have the personality profile of being a driver, I will let them take more control of the conversation; if they are passive, I will take the lead. I am firmly convinced that it is not only important to meet the tangible planning and investment needs of clients; it is equally important to meet their emotional and behavioral needs.

When we are comfortable with all of the data-gathering, resources, and objectives for retirement, I develop an overall detailed plan with recommendations and present it in a manner appropriate to their personality profile. For most clients in their late 50s or 60s, the primary concern is developing an income stream that we think they will not outlive and that will outperform inflation with a lower degree of volatility. I generally set up time-sensitive goals for different investment buckets as part of their overall financial strategy plan. I also look at several different sources from which to generate income. It starts with Social Security, but can cover areas such as mutual funds; ETFs; annuities; REITs; fixed income; dividend-paying stocks; and, hopefully, future asset growth out of their risk assets such as equities.

Again, by understanding their emotional personality and communication style, it can vary significantly from the traditional model based on a client’s age, their outlook on risk, their overall objectives and resources, their distribution needs, and their overall investment plan. Client A and Client B could each have $500,000 available for their investment piece, but their portfolios could look very different. Client A’s could even look very different in June from where it might have been had they come to me in January based on an assessment of current market conditions and the relative strength of various asset classes and sectors. For some clients, I use dollar-cost averaging, but for others I prefer value-cost averaging—raising or lowering new allocations to equities, for example, based on market valuations.

Again, by understanding their emotional personality and communication style, it can vary significantly from the traditional model based on a client’s age, their outlook on risk, their overall objectives and resources, their distribution needs, and their overall investment plan. Client A and Client B could each have $500,000 available for their investment piece, but their portfolios could look very different. Client A’s could even look very different in June from where it might have been had they come to me in January based on an assessment of current market conditions and the relative strength of various asset classes and sectors. For some clients, I use dollar-cost averaging, but for others I prefer value-cost averaging—raising or lowering new allocations to equities, for example, based on market valuations.

I spend a great deal of time in the beginning educating clients on my technical approach to the markets and the value of using of risk-management techniques. For example, the historical annual average return of the S&P 500 over the past 15 years, despite the current bull market, remains on the low side. According to research conducted by Morningstar, most investors did much worse than the market over this period. Obviously this is because of the huge market displacements of the early 2000s and 2007-2009—extreme circumstances for which few investors were prepared.

One of my goals for every client who has risk assets in their portfolio is to try to mitigate that market risk by repositioning their exposure—moving to cash or short-term bonds—by including noncorrelated assets such as hedge funds or managed futures or through other risk-management techniques such as option strategies. Being an independent advisor affords me the flexibility to provide this service through the use of technical and fundamental market analysis. I am able to reposition clients’ equity assets into more conducive investment models, thereby offering true money management.

My role is to offer my clients a concierge investment model by building customized portfolios that provide a higher probability to meet their overall plan objectives. Every person is unique: Their time horizons vary, their risk tolerances are different, their times of distribution fluctuate and their personalities and family circumstances are distinctive. I take a lot of pride in developing custom solutions for each and every client, and it takes a tremendous amount of work. Clients have shown their appreciation through their loyalty and trust in our firm and in being very generous with their referrals to friends and family.

Joseph Bartosiewicz is an investment advisor representative at SagePoint Financial Inc. in Avon, Connecticut. Mr. Bartosiewicz has more than 34 years of experience in the finance industry and has earned various securities and insurance licenses.

Joseph Bartosiewicz is an investment advisor representative at SagePoint Financial Inc. in Avon, Connecticut. Mr. Bartosiewicz has more than 34 years of experience in the finance industry and has earned various securities and insurance licenses.

A graduate of Western Connecticut State University, Mr. Bartosiewicz has had a “lifelong fascination” with the financial markets and became a financial advisor shortly after college. He started in the business with IDS Financial Services and began his own advisory firm in 1988. His practice offers a variety of services to clients, including financial planning, asset management, tax-reduction strategies, insurance, estate planning, and retirement planning.

Mr. Bartosiewicz avidly practices technical and quantitative analysis and applies many of its principles to the management of client investment accounts. He was introduced to the markets at an early age, purchasing his first stock “with money from [his] paper route under the guidance of a relative.” Mr. Bartosiewicz writes a monthly newsletter and publishes various online articles for his clients and the industry, educating readers on how to identify technical patterns and opportunities based on his own observations using technical analytics.

Mr. Bartosiewicz is a lifelong resident of Connecticut and resides in Avon with his wife and three children. He has a deep passion “for music in all forms” and “has been in a number of bands as a singer and bass player since college.”

Disclosure: Joseph Bartosiewicz is an investment advisor representative offering securities and advisory services through SagePoint Financial Inc., member FINRA, SIPC, and a registered investment advisor. Registered branch office: 5 Colby Way, Avon, CT 06001.

Photography by Christopher Beauchamp