Is government spending inflationary?

Is government spending inflationary?

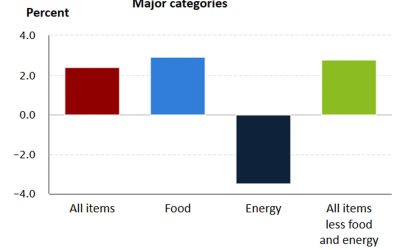

The stimulus bills approved by Congress starting in 2020 led to the largest surge in government spending in history, coinciding with a sharp rise in inflation. This has led many to assume that government spending itself caused inflation. But is that assumption correct?

In this “Three on Thursday,” we explore whether government spending inherently leads to inflation. Milton Friedman famously stated, “Inflation is always and everywhere a monetary phenomenon … produced only by a more rapid increase in the quantity of money than in output.” From this perspective, it’s not government spending alone that drives inflation, but how that spending is financed. If spending is funded through borrowing from the private sector, inflationary effects are limited because the overall money supply remains stable. However, when spending is financed by printing new money—expanding the money supply without a corresponding increase in economic output—inflation is inevitable. For a deeper understanding of this relationship, let’s explore three scenarios.

Scenario 1

Most federal government spending is financed by the private sector through taxation or borrowing. Consider an example: The government plans to spend $100. It raises $50 through taxes from Peter and borrows $50 from Paul. Is this inflationary? No, because the total money supply in the economy hasn’t changed—only its distribution has shifted. Think of the economy as a pool, with the water representing the total quantity of money. In this scenario, the government is simply scooping water from the shallow end (via taxes and borrowing) and pouring it back into the deep end (via spending). The total amount of water in the pool remains the same; only its location has been adjusted.

Source: First Trust

![]() Related Article: Inflation perceptions and the ‘money illusion’

Related Article: Inflation perceptions and the ‘money illusion’

Scenario 2

Occasionally, government spending is not only financed by the private sector but also by the Federal Reserve (“Fed”). This is where government spending becomes inflationary. Starting in 2020, government spending increased by over $5 trillion, much of it funded by the Federal Reserve creating money out of thin air to purchase Treasury bonds. This massive injection of newly created money caused the money supply to surge, driving the inflation that followed. Using the pool analogy, typically, the government borrows from the private sector, taking a bucket of water from the shallow end and pouring it into the deep end—leaving the overall water level unchanged. In this case, however, a water truck called the Fed backed up to the pool and dumped in vast amounts of new water (newly created money), causing the pool to overflow (inflation). This dramatic increase in the money supply is the primary driver of the inflation we experienced.

Source: First Trust

Scenario 3

How do you lower inflation? Think back to the pool analogy: The economy is the pool, and the water level represents the money supply. Inflation occurs when too much water (money) overflows the pool (economy). To fix this, you can either drain water (reduce the money supply) or expand the pool (grow the economy). Though the picture makes it look straightforward, draining money is difficult once the Fed puts it into the economy. It can’t confiscate money. However, the government can stop increasing the money supply and let the economy catch up. This will lower inflation. Deregulating or cutting taxes may incentivize business starts, innovation, and investment—all of which grow the size of the pool.

Source: First Trust

Editor’s note: Brian Wesbury is chief economist at First Trust Advisors LP. He and his team prepare a weekly market commentary titled “Monday Morning Outlook,” as well as frequent research reports and the recurring feature “Three on Thursday.” Proactive Advisor Magazine thanks First Trust for permission to republish an edited version of this commentary, which was first published on Jan. 16, 2025.

This report was prepared by First Trust Advisors LP and reflects the current opinion of the authors. It is based on sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

The opinions expressed in this article are those of the author and the sources cited and do not necessarily represent the views of Proactive Advisor Magazine. This material is presented for educational purposes only.

First Trust Portfolios LP and its affiliate First Trust Advisors LP (collectively “First Trust”) were established in 1991 with a mission to offer trusted investment products and advisory services. The firms provide a variety of financial solutions, including UITs, ETFs, CEFs, SMAs, and portfolios for variable annuities and mutual funds. www.ftportfolios.com

RECENT POSTS