Editor’s note: Tony Dwyer, U.S. portfolio strategist for Canaccord Genuity, and his colleagues author a widely respected monthly overview of market conditions, technical factors, and future market outlook called the “Strategy Picture Book.” The following provides an excerpt from their May 10, 2017, report on the short-term market outlook.

Our recent market upgrade was more about becoming offensively positioned vs. expecting a big near-term market ramp

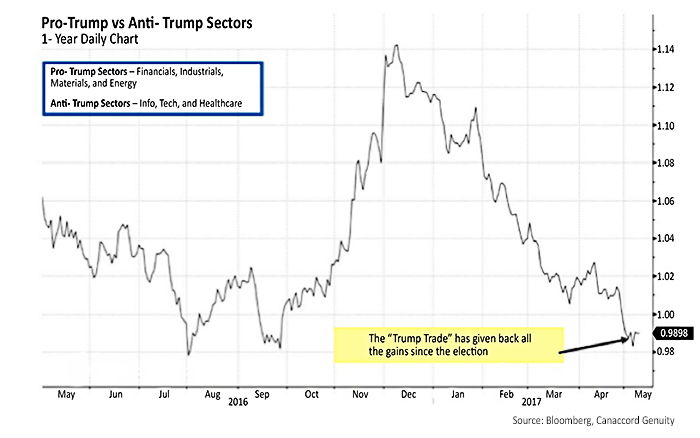

Some have suggested that disappointment in the Trump agenda could have a negative market impact, but we would argue the pro-Trump sectors have already been beaten down versus the anti-Trump sectors (Figure 1). In fact, they have given back all the post-election gains relative to the anti-Trump sectors despite (1) a solid domestic and global economic outlook, (2) still-accommodative Fed policy as seen through the positive-sloped yield curve, (3) the demographic tailwind of millennials that should drive housing, and (4) continued earnings-per-share (EPS) recovery that could ramp up if any of the proposed tax cuts occur.

FIGURE 1: ‘TRUMP TRADE’ GIVING BACK GAINS

We remain focused on intermediate-term potential and recently adopted a more offensive position

While our key tactical indicators have not reached a level that typically pulls us off the sidelines, the combination of several factors causes us to turn our attention to the intermediate-term opportunity rather than the near-term risk:

1. Our positive fundamental core thesis remains in place regarding factors such as inflation, interest rates, economic growth, a positive EPS trend, and valuations.

2. The synchronized global recovery and improvement in the domestic economic data and EPS.

3. The generally positive market history following long-duration, low-volatility periods.

4. Increased probability of corporate tax cuts.

We believe our SPX 2017 and 2018 targets of 2,470 and 2,720, respectively, may prove to be conservative. We would add to positions in the Financial and Industrial sectors, and begin stepping into Energy and Materials sectors, on further weakness.

We expect several continued macro-economic tailwinds will help in keeping animal spirits in the markets alive: (1) historic global monetary accommodation, (2) improving commodities and stable emerging currencies, (3) positive trending U.S. economic growth, and (4) an acceleration in the global economy. Only a real Fed Funds rate above 2%, an inversion of the U.S. Treasury yield curve, and significant stress in the Chicago Fed National Financial Conditions Index would command a long-term change in our positive economic view.

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

Tony Dwyer is the head of the U.S. Macro Group and chief market strategist at Canaccord Genuity. He also sits on the firm’s U.S. operating committee. Mr. Dwyer joined Canaccord Genuity in 2012 and is known for the practical application of macroeconomic and tactical market indicators. Mr. Dwyer was previously equity strategist and director of research at Collins Stewart and a member of the firm's executive committee. Mr. Dwyer is a frequent guest on many financial news networks. canaccordgenuity.com

Tony Dwyer is the head of the U.S. Macro Group and chief market strategist at Canaccord Genuity. He also sits on the firm’s U.S. operating committee. Mr. Dwyer joined Canaccord Genuity in 2012 and is known for the practical application of macroeconomic and tactical market indicators. Mr. Dwyer was previously equity strategist and director of research at Collins Stewart and a member of the firm's executive committee. Mr. Dwyer is a frequent guest on many financial news networks. canaccordgenuity.com