Last week’s U.S. economic data painted a mixed but still reasonably resilient picture. Reports on employment, manufacturing, and retail sales all improved on the topline, though each data set included some caveats.

Employment situation

The clearest headline was Friday’s Labor Department jobs report: Nonfarm payrolls rose by 178,000 in March, and the unemployment rate moved slightly lower to 4.3%. Gains were led by health care, construction, and transportation and warehousing, while federal government employment continued to decline. The total increase far surpassed consensus estimates of 59,000.

FIGURE 1: MONTHLY JOB CREATION IN THE U.S. (JAN. 2021–MARCH 2026)

Sources: Fox Business, U.S. Bureau of Labor Statistics

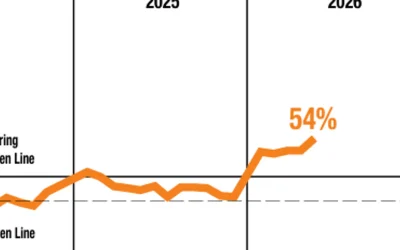

However, the labor news was not uniformly strong.

February payrolls were revised down to a loss of 133,000, labor-force participation slipped to 61.9%, and average hourly earnings rose just 0.2% in March, suggesting a job market that is holding up but not broadly accelerating. On an annualized basis, says CNBC, the 3.5% earnings increase from a year ago was the lowest since May 2021.

FIGURE 2: GROWTH IN AVERAGE HOURLY EARNINGS IN THE U.S. (YEAR-OVER-YEAR % CHANGE: JAN. 2022–MARCH 2026)

Note: All employees on private nonfarm payrolls.

Sources: CNBC, U.S. Bureau of Labor Statistics.

Earlier in the week, the Labor Department’s Job Openings and Labor Turnover Survey (JOLTS) report reinforced that more cautious interpretation: February job openings fell to 6.9 million, hiring dropped to 4.8 million, and quits remained subdued, pointing to a labor market that still looks more “low-hire, low-fire” than robust. According to Haver Analytics, the hiring rate slumped to 3.1%, the lowest since April 2020.

Initial jobless claims, however, stayed low at 202,000 for the week ended March 28, so there is still little sign of a broad-based wave of layoffs.

ISM Manufacturing Index improves

ISM’s March Manufacturing PMI showed factory activity still in expansion territory, though the report also highlighted rising price pressures and softer demand signals beneath the surface.

MarketWatch reported,

“American manufacturers grew in March at the fastest pace in 2½ years, by one measure, but the Iran war added fresh uncertainty and threatened to boost inflation just as the effects of the original Trump tariffs were fading.

“The Institute for Supply Management’s survey of manufacturers inched up to 52.7% in March. … It was the highest reading since August 2022. …

“Production rose in March as companies caught up on prior orders. Yet new orders, a sign of future sales, slowed for the third month in a row. …

“A measure of prices, meanwhile, leapt to a three-year high in a sign of stubborn inflation. Whether the price increases prove temporary will depend on how long the Iran conflict lasts and the levels of replacement tariffs.”

FIGURE 3: NEW CYCLE HIGH FOR ISM MANUFACTURING

Sources: Bespoke Investment Group, Institute for Supply Management

Bespoke Investment Group provided the following commentary on ISM data:

“The March ISM Manufacturing report provided one of the first major reads on the economy since the Iran war started. Despite the headwinds from fresh geopolitical chaos, March’s ISM Manufacturing reading was stronger than expected and rose to a new cycle high, holding on to the big recent gains. As one respondent put it, ‘We’re seeing steady increases in activity, but geopolitical issues and the Iran war are already waning sentiment.’

“That sentiment shift was most visible in prices which rose to the highest levels since 2022, with respondents citing price increases across a wide range of metals and industrial inputs. Delivery times are also accelerating: ‘Current Middle East unrest is already starting to impact business operations by increasing lead times, costs, container delays and the like.’ While the employment subindex has picked up, we also note that it remains below 50 and is not exactly the picture of strength given steady acceleration in the headline index.”

FIGURE 4: PRICES SURGE AS PETROLEUM COSTS SPIKE HIGHER

Sources: Bespoke Investment Group, Institute for Supply Management

![]() Related Article: QE may be bearish for T-bonds

Related Article: QE may be bearish for T-bonds

Retail sales higher in February

February retail sales were fairly solid. Advance retail and food services sales rose 0.6% from January to $738.4 billion and were up 3.7% from a year earlier, suggesting consumers were still spending despite broader growth concerns. Economists expected a 0.4% monthly increase.

FIGURE 5: U.S. RETAIL SALES (MONTH-OVER-MONTH % INCREASE FOR PAST YEAR)

Sources: Trading Economics, U.S. Census Bureau

First Trust commented on the data release, pointing out that the broad picture for retail sales remains unclear:

“Retail sales generated a strong headline for February, but the broader picture remains soft. Looking at the headline, overall retail sales beat expectations and rose 0.6% for the month—the largest increase since July—while previous activity was revised higher. However, much of that increase can be attributed to a bounce-back in sales after severe winter weather held back activity in January. Taking a step back, overall retail sales have risen 3.7% in the past twelve months, but are up just 1.8% annualized in the last six months. It’s also important to remember the impact of inflation. ‘Real’ inflation-adjusted sales are up 1.3% in the past twelve months, but are down at a 0.7% annualized rate over the last six months. …”

“We like to follow ‘core’ sales, which strip out the volatile categories for autos, building materials, and gas stations—important for estimating GDP. This measure rose 0.4% in February but was revised slightly lower in previous months. Within the core grouping, rising sales at nonstore retailers (+0.7%) contributed, along with a rebound across most brick-and-mortar categories. Meanwhile, the category for restaurants & bars—the only glimpse we get at services in this report—rose 0.4% in February after declining in three out of the four months prior. These sales are up 5.2% in the last year (above the increase for overall sales) but will be worth watching in the months ahead as a bellwether for the consumer’s overall well-being.”

RECENT POSTS