Volatility remains bullish.

There really isn’t much else to say other than that.

$VIX has drifted back below 14, and that is causing the usual amount of worry and consternation that it is “too low.” In reality, a low $VIX is benign as far as the stock market goes; stocks can continue to rise for a long time while $VIX is low. The danger occurs when $VIX begins to rise. Currently, if $VIX were to climb above 17, that would be cause for stock traders to worry. Otherwise, it’s in a bullish condition.

However, the question is “Are longer-term volatility indexes ‘too low’?”

They might be.

The “mistake” that the market often makes is getting too complacent during rally phases. One of the signs of complacency is extremely low volatility.

Part of this is unavoidable because the calculation of historical volatility necessarily yields lower numbers as the market trades at higher prices. Furthermore, short-term implied volatility will not deviate too much from realized volatility, for there are quasi-arbitrage strategies that will be put in place, holding implied volatility down. Longer-term volatilities can remain higher, though—not adhering to realized volatility but normally trading more toward the long-term average volatility of the underlying index.

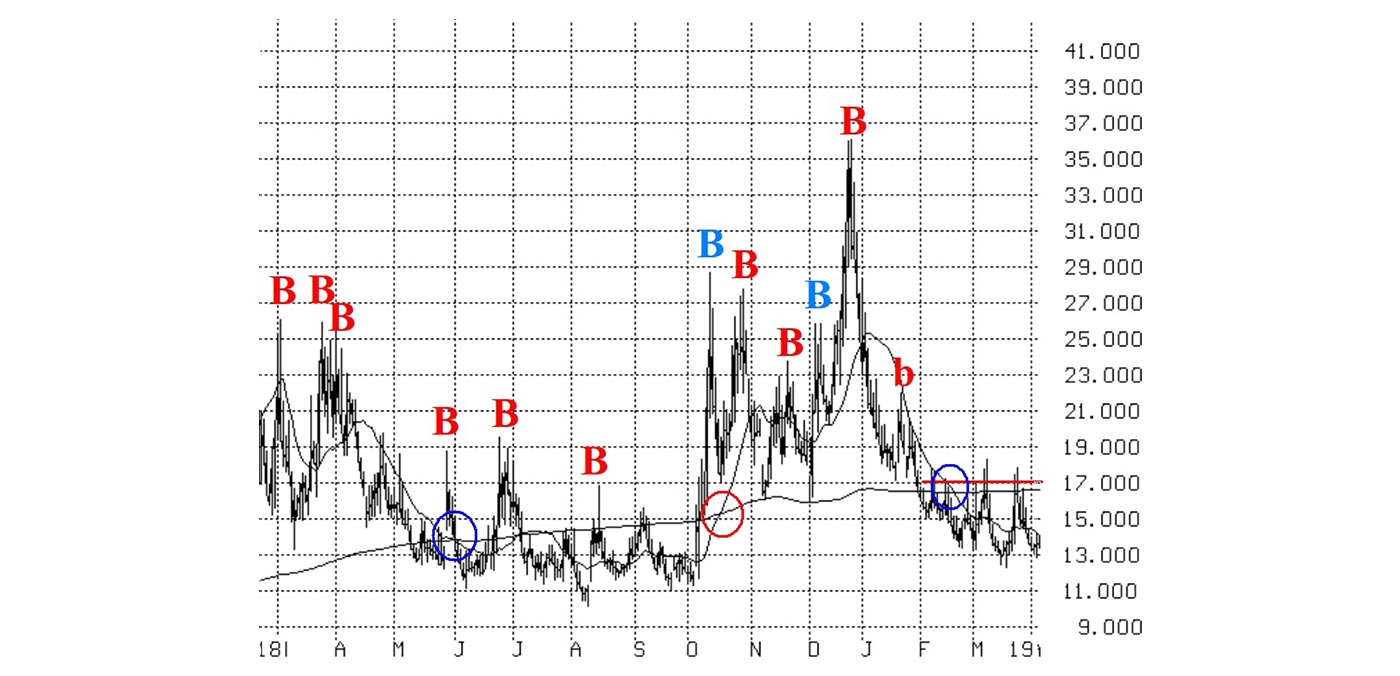

At the current time, $VIX is just below 14. That’s low but not “too low.” However, if one looks at the longer-term volatilities as calculated by the Cboe’s Volatility Indexes, signs of complacency are beginning to appear. Specifically, the longest-term Cboe Volatility Index is for the one-year duration (symbol: $VIX1Y). It is currently trading at about 17.50—quite low for long-term implied volatility estimates.

FIGURE 1: ONE-YEAR TREND OF $VIX

Source: McMillan Analysis Corporation, market data.

Typically, if a trader asks a market maker for a quote on a one-year option, the market maker would price the option at an average long-term volatility. The long-term volatility of $SPX and other broad-based indexes is normally at least 20, or even higher. That’s why volatility term structures slope upward in bull markets—because the farther out one goes, the more weight is placed on longer-term (average) volatility than on near-term (low) volatility.

Currently, this low $VIX1Y price is why the current term structure doesn’t slope upward more steeply than it does. At this point in other bull markets, with $VIX having dropped below 14, the slope of the term structure would be steeper than this.

Is this a sign of complacency? Well, it’s certainly not the opposite.

Consider this: The price of a one-year, at-the-money SPY call is about 22.60, and its “Vega” is 1.13. That is, the option price would increase by 1.13 if implied volatility rose one point. So, if implied volatility were to rise from its current level of 17.50 (the price of $VIX1Y) to, say, 22.5, the option price would rise by 5.65, or about 25% of its current value. That’s great if you’re long the option, but not so good if you’re short. It just seems to me that some traders are being overly complacent by selling one-year SPX options at a volatility of 17.50.

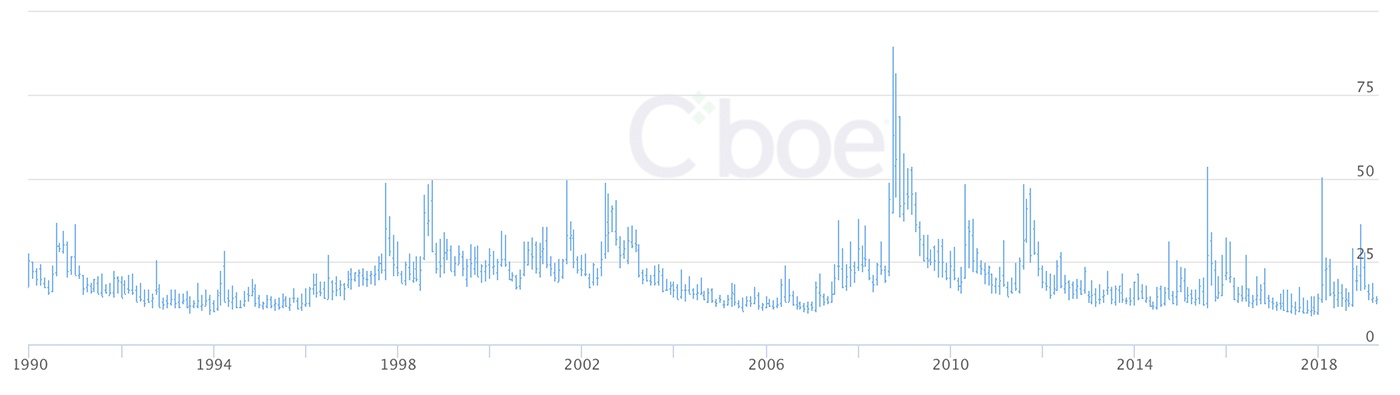

FIGURE 2: VIX INDEX TREND SINCE 1990

Source: Cboe

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

This article is an edited version of market commentary that was first published at optionstrategist.com on April 5, 2019.

Professional trader Lawrence G. McMillan is perhaps best known as the author of “Options as a Strategic Investment,” the best-selling work on stock and index options strategies, which has sold over 350,000 copies. An active trader of his own account, he also manages option-oriented accounts for clients. As president of McMillan Analysis Corporation, he edits and does research for the firm’s newsletter publications. optionstrategist.com

Professional trader Lawrence G. McMillan is perhaps best known as the author of “Options as a Strategic Investment,” the best-selling work on stock and index options strategies, which has sold over 350,000 copies. An active trader of his own account, he also manages option-oriented accounts for clients. As president of McMillan Analysis Corporation, he edits and does research for the firm’s newsletter publications. optionstrategist.com