How does gold perform in different market scenarios?

How does gold perform in different market scenarios?

The role of gold in investment portfolios: Part I

Should an investment in gold be a key element of effectively diversified and risk-managed portfolios?

Editor’s note: A revised and updated version of this article can be found here.

Flexible Plan Investments, an active money manager and provider of investment risk-management services, first authored an extensive analysis of the role of gold in investment portfolios in 2013. This white paper has been recently updated and will be presented as a guest commentary in two parts in Proactive Advisor Magazine. We are pleased to present Part I here.

One thing is certain. Within the challenging environment we have all seen, it has become imperative to develop a portfolio approach that minimizes drawdowns and volatility while delivering respectable returns, and all within an individualized investor risk profile.

Perhaps nowhere has the debate raged more fiercely than in consideration of alternative asset classes, especially the role of commodities and precious metals, and most notably gold. Many traditional wealth and portfolio managers will begrudgingly acknowledge that gold should play a role in investors’ portfolios, but the rationale can seem quite thin and more instinctual than empirical.

This paper will present a brief discussion of the “gold debate,” a broad overview of the tangible benefits of portfolio diversification with gold, and some eye-opening data suggesting a much more important role for gold in portfolios that seek optimal risk-adjusted returns.

Gold has been used as a form of currency for thousands of years. Unlike paper or some electronic currency, gold has a fixed supply and as a physical commodity can be relatively difficult to obtain. As a result, gold has historically offered a natural hedge against inflation and provided an alternative to investors when the value of other forms of currency is depreciating.

But what does this mean for today’s investors and those entrusted to manage their portfolios?

One can find compelling arguments from respected investment professionals, economists, hedge fund managers, and major Wall Street strategists on all sides of the gold issue as it pertains to portfolio management.

The role of gold in

investment portfolios

by Flexible Plan Investments explores

why investors should reconsider

their portfolio’s allocation to gold.

“I think gold should be a part of everybody’s portfolio to some degree because it diversifies the portfolio—it is the alternative money. We have a situation where we have too much debt. Too much debt leads to the printing of money to make it easier to service. … Money can be produced, [but the supply of] gold is somewhat limited.”

The literature from academia, the financial press, respected Wall Street firms, and the investing community all generally come back to some basic assertions about the potential benefits of allocations to gold in a portfolio:

- As a hedge against inflation.

- As a hedge against deflation.

- As protection against a declining U.S. dollar (and other major global currencies).

- As a safe haven in times of geopolitical and financial-market instability.

- As a basic commodity, with its own supply-and-demand fundamentals.

- As a long-proven store of historical value.

- As an “insurance policy” against black swans and “left-tail” risk events.

- As an asset with negative (though not perfect) correlations with other asset classes.

- As an investment with an underlying global central bank and sovereign wealth demand.

- As an underowned investment class, suggesting future demand increases.

- As an important portfolio diversifier.

Each of these arguments can find its supporters and naysayers, all armed with their own particular analyses and biases. But even well-credentialed critics of gold grudgingly admit there is a place for it in most investor portfolios.

“The attractiveness of gold as an investment can generate heated arguments, many of which are based on wishful thinking rather than fact. … Most arguments for holding gold in a portfolio are not supported by an analysis of the data. Nonetheless, an argument can be made for including gold as a commodity in a well-diversified portfolio, particularly if investors and central banks increase their demand—even moderately—for gold.”

“We find that because of its lack of correlation with other financial assets, gold has a useful role to play in stabilizing the value of a portfolio even if the conservative assumption of a modest negative real annual return is made.”

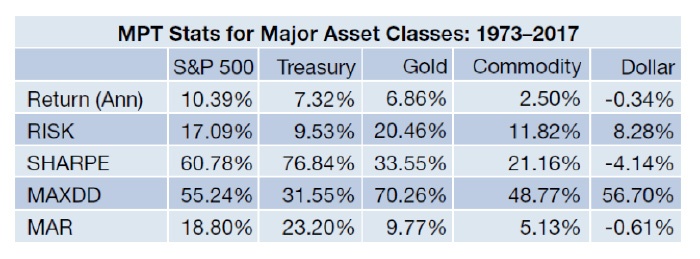

We will focus this quantitative assessment on a look at how gold has performed relative to other major asset classes since 1973 (the year in which the price of gold was finally unfrozen from its $35-per-ounce Great Depression status) under a variety of market and economic conditions. The global and U.S. economies since that time have thrown a multitude of challenging situations at investors, from several energy crises, to the interest-rate spikes of the 1970s, to any number of macro geopolitical situations—including the two great booms and busts of the stock market over the past two decades.

We have selected 1973 as the starting point for our analysis, as this represents what we believe to be the first “clean” calendar year for gold price performance following the momentous decisions of the Nixon administration in August 1971. Actions taken then effectively ended “ties” to the historic gold standard for the U.S. dollar and suspended convertibility of the dollar to gold.

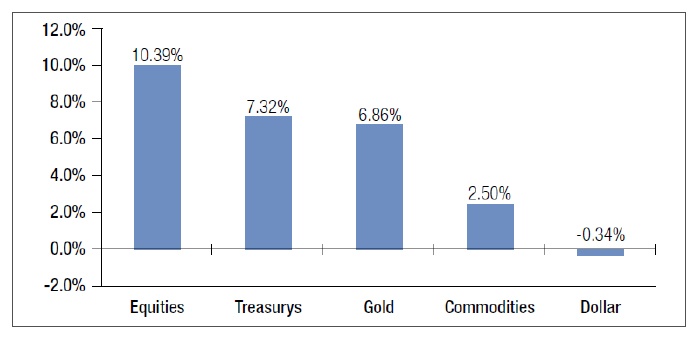

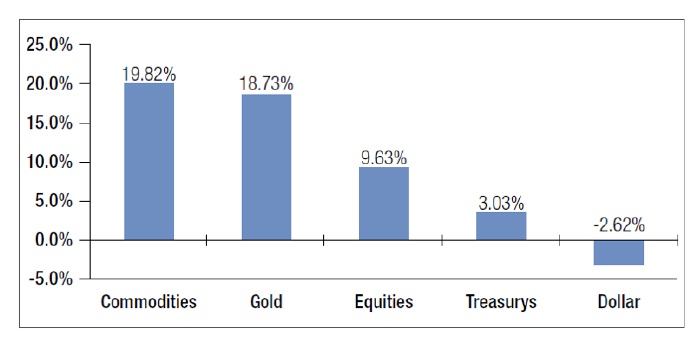

Let’s first look at the annualized rate of return of various asset classes from 1973 to December 31, 2017 (Figure 1).

Definition: Annualized returns of various asset classes over time. See source data.

Source: Flexible Plan Investments

It is also noteworthy that the dollar fell on average during the period. In addition, commodities rose, suggesting that the period was typically inflationary. These conditions provided a tailwind for both equities and gold.

Let’s examine several of these economic scenarios, again based on historical data from January 1973 to December 29, 2017. We will examine the performance of gold relative to other asset classes under seven different market environments that typically concern investors:

- Real returns on the 10-year Treasury bond are negative (real interest rates less than zero).

- Equities are in a bear market.

- Commodity prices are in a bull market.

- The U.S. dollar is in a bear market.

- U.S. Treasury bonds are in a bear market (rising interest-rate environment).

- Inflation is rising.

- Market volatility is high.

The method used in these comparisons was to first determine the dates during which each of these conditions existed. Then we calculated the daily rate of total return achieved by each asset class during these periods when these conditions were extant. An annualized return was then calculated by geometrically linking each period of daily returns for the various periods of the condition for each of the asset classes. Finally, a comparison of each asset class with the other was made for the entire time period studied.

Typically, when real yields are positive, equities and bonds tend to perform well as long-term investments. However, the nightmare scenario that keeps pension-fund and other asset managers up at night is when real yields are negative.

Under certain conditions, investors are willing to accept a negative real return in exchange for “safety” and the likelihood that they will recover most of the principal that they invest. This is most common for conservative investors that are near to or currently in retirement.

Negative real rates have been common throughout much of the era that has followed the financial crisis of 2007–2009. This is the result of the Federal Reserve systematically lowering interest rates to near-zero levels in order to boost the economy. Treasury yields had fallen so far that they were below the rate of inflation for much of 2011 and 2012—indicating that real yields were actually negative.

In such an environment, the question becomes, “How is an investor going to earn a real return on his or her investments?” This scenario deserves serious consideration. As it turns out, the great savior in this scenario has historically been gold.

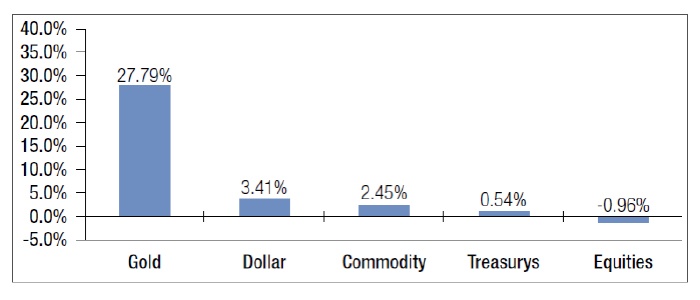

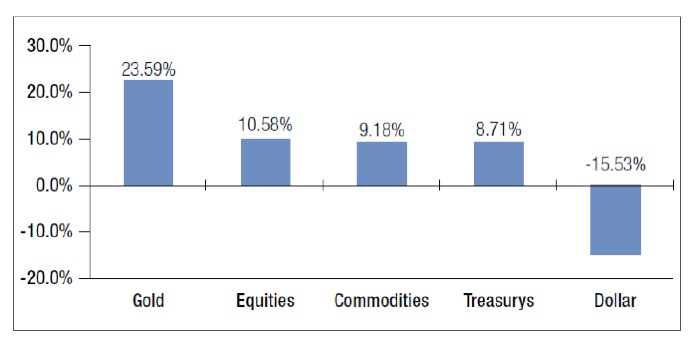

Figure 2 shows the compounded annual return for various asset classes when real 10-year yields are negative.

Definition: When the current total return of a 10-year Treasury bond minus the expected rate of inflation is less than zero.

Source: Flexible Plan Investments

Only gold and the U.S. dollar perform well in these instances. Real rates are negative particularly in times of market stress, leading to a flight to safe-haven assets. Additionally, a negative real-interest-rate environment can be caused by high inflation values. Both of these scenarios are positive for gold, giving it the highest return of any asset class in this scenario.

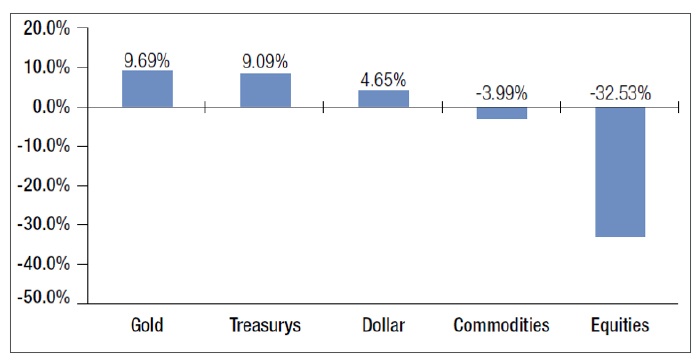

(1973–12/29/2017)

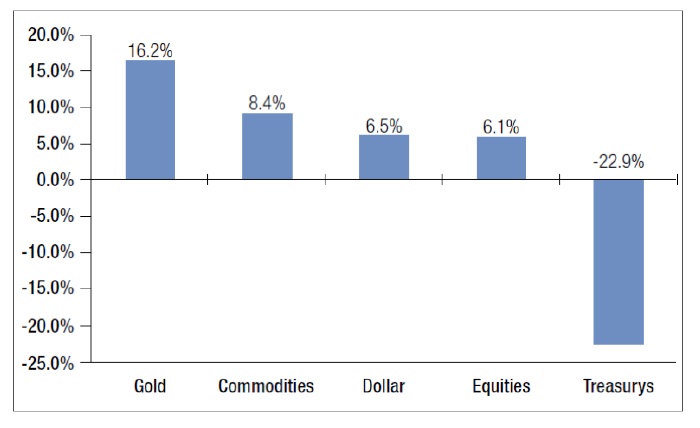

Definition: Equity bear markets are said to occur when equity prices decrease 20% or more. *See source data.

Source: Flexible Plan Investments

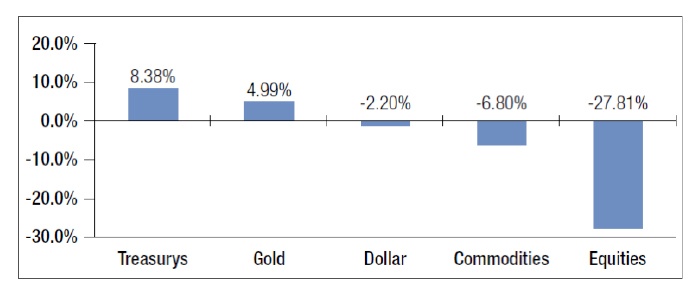

The period from 10/10/2007 through 3/9/2009 marked the recent credit crisis, and it was considered a major bear market, lasting 355 days. During this period, the equity market fell 55.2%. In contrast, gold rose 24.6%, more than both Treasurys and the U.S. dollar, which both gained 13.5%. Surprisingly, commodities as an asset class fell in value and did not prove to be a fully defensive allocation.

Definition: Commodity bull markets are said to occur when commodity prices rise 20%.

Source: Flexible Plan Investments

Definition: Bear markets for the U.S. dollar are said to occur when prices decrease 10%.

Source: Flexible Plan Investments

For example, the Bretton Woods agreement was a fixed-exchange-rate system where the U.S. dollar could be exchanged for gold at a fixed price of $35 per ounce, and other major world currencies had a fixed exchange rate to the dollar. As mentioned earlier, in response to a growing deficit in U.S. gold reserves versus U.S. dollars outstanding, President Nixon decided to break the agreement in 1971. In March 1973, the fixed-exchange-rate system officially became a floating exchange-rate system. The U.S. dollar was in a bear market from 1/22/1973 to 7/6/1973 and declined roughly 18% during that time frame. Gold gained 331% over that same time frame, reflecting the increased money supply that was not factored into the price.

Definition: Bear markets for U.S. Treasurys are said to occur when Treasury prices decrease 10%.

Source: Flexible Plan Investments

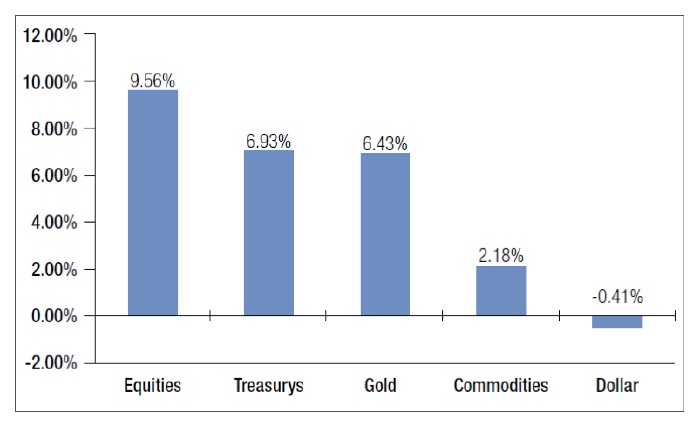

Within this type of environment, the U.S. dollar clearly weakened, in both “price” and purchasing power. Gold performed well. In fact, the yellow metal outperformed a basket of commodities, the usual safe harbor preferred by investors during inflationary times. At the same time, however, both equities and, surprisingly and ever so slightly, Treasurys have historically outperformed gold during these periods.

Definition: Rolling 12-month rate of change in the CPI is positive.

Source: Flexible Plan Investments

(1990–12/29/2017)

Definition: The VIX Index is in the top quintile of historical data.

Source: Flexible Plan Investments

But, how does gold perform under different classic economic regimes?

Part II of “The Role of Gold in Investment Portfolios” will examine this question in some detail, as well as provide overall conclusions surrounding optimal allocations to gold in a modern portfolio. Look for Part II in an upcoming issue of Proactive Advisor Magazine.

This article presents an excerpt of the white paper “The Role of Gold in Investment Portfolios.” The complete paper—including a list of source data— can be found here.

Past performance does not guarantee future results. Inherent in any investment is the potential for loss as well as profit. A list of all recommendations made within the immediately preceding 12 months is available upon written request.

This white paper is provided for information purposes only and should not be used or construed as an indicator of future performance, an offer to sell, a solicitation of an offer to buy, or a recommendation for any security. Flexible Plan Investments, Ltd., cannot guarantee the suitability or potential value of any particular investment. Information and data set forth herein have been obtained from sources believed to be reliable, but that cannot be guaranteed. Before investing, please read and understand Flexible Plan Investments, Ltd., ADV Part 2A and Part 2A Appendix 1.

The original white paper, published by Flexible Plan Investments in November 2013, was written by David Varadi, David Wismer, and Jerry C. Wagner. The updated white paper, published in June 2018, was revised by Jerry C. Wagner, Jason Teed, and Tim Hanna. flexibleplan.com

Since 1981, Flexible Plan Investments (FPI) has been dedicated to preserving and growing wealth through dynamic risk management. FPI is a turnkey asset management program (TAMP), which means advisors can access and combine FPI’s many risk-managed strategies within a single account. FPI’s fee-based separately managed accounts can provide diversified portfolios of actively managed strategies within equity, debt, and alternative asset classes on an array of different platforms. FPI also offers advisors the OnTarget Investing tool to help set realistic, custom benchmarks for clients and regularly measure progress. flexibleplan.com