After the fastest entry to a bear market—ever—and record unemployment claims, what is in store for the Q1 2020 earnings season?

JPMorgan Chase’s Jamie Dimon sees significant risks to the U.S. and global economies.

According to CNBC’s recap, Mr. Dimon wrote,

To this point, some analysts, according to Bloomberg’s “Surveillance” radio program, currently expect to see companies cut dividends by 25% or more, and stock buybacks to fall by 50%.

For the full year, CNBC says Goldman Sachs is forecasting a 6.2% decline in U.S. GDP. This could include, according to Goldman, a drop of more than 30% in Q2 (“the worst period in post-World War II history”), but also the potential for a 19% surge in Q3 (“That would take the U.S. from the worst quarter in history to its best”).

Guggenheim has a somewhat more negative outlook on GDP, writing on April 5 in its Global CIO Outlook,

“We are currently estimating an economic contraction of well over 10 percent this year. … But one thing I would caution is that if earnings continue to fall as I expect them to, S&P earnings could get as low as $100 this year. Given the traditional market multiple of about 15 times earnings, that would put the S&P at about 1,500, still about a thousand points lower than we are today. … But someday the pandemic will end. In terms of output, it will take about four years to get U.S. GDP back to where it was at the end of the fourth quarter of 2019.”

Morgan Stanley’s outlook is far more positive. Although acknowledging that pandemic news may get far worse, MarketWatch noted the firm’s recent comments:

“Morgan Stanley’s chief U.S. equity strategist Mike Wilson said that for stocks and investors the worst was behind us. He said bear markets end with recessions and that stocks had reached a good entry point for investors. ‘With the forced liquidation of assets in the past month largely behind us, unprecedented and unbridled monetary and fiscal intervention led by the U.S. and the most attractive valuation we have seen since 2011, we stick to our recent view that the worst is behind us for this cyclical bear market that began two years ago, not last month.’”

Against this backdrop of commentary, what do estimates for Q1 earnings look like?

Bespoke Investment Group wrote on April 3,

“As investors try to navigate the various market swings that will continue as the spread and fallout from the virus continues its path, don’t forget the most basic of all data points: company earnings. So far, analyst estimates do not reflect anything close to the shock that’s pending . …

“It’s understandable why they would be so neutral; any guess at the downside is pure finger-in-the-air stuff at this point. But the hard impact will become more clear in coming weeks as reports for Q1 start; we are less than two weeks from JPM’s earnings on April 14th which will start what will be an ugly earnings season.

“Once earnings begin, investors will be forced to deal with the shock currently under way to corporate cash flow, and markets will be forced to process that new shock to sentiment on top of all the existing headlines related to COVID-19 and the collapse of the national economy in abstract terms.”

FactSet provided the following analysis, as of April 3:

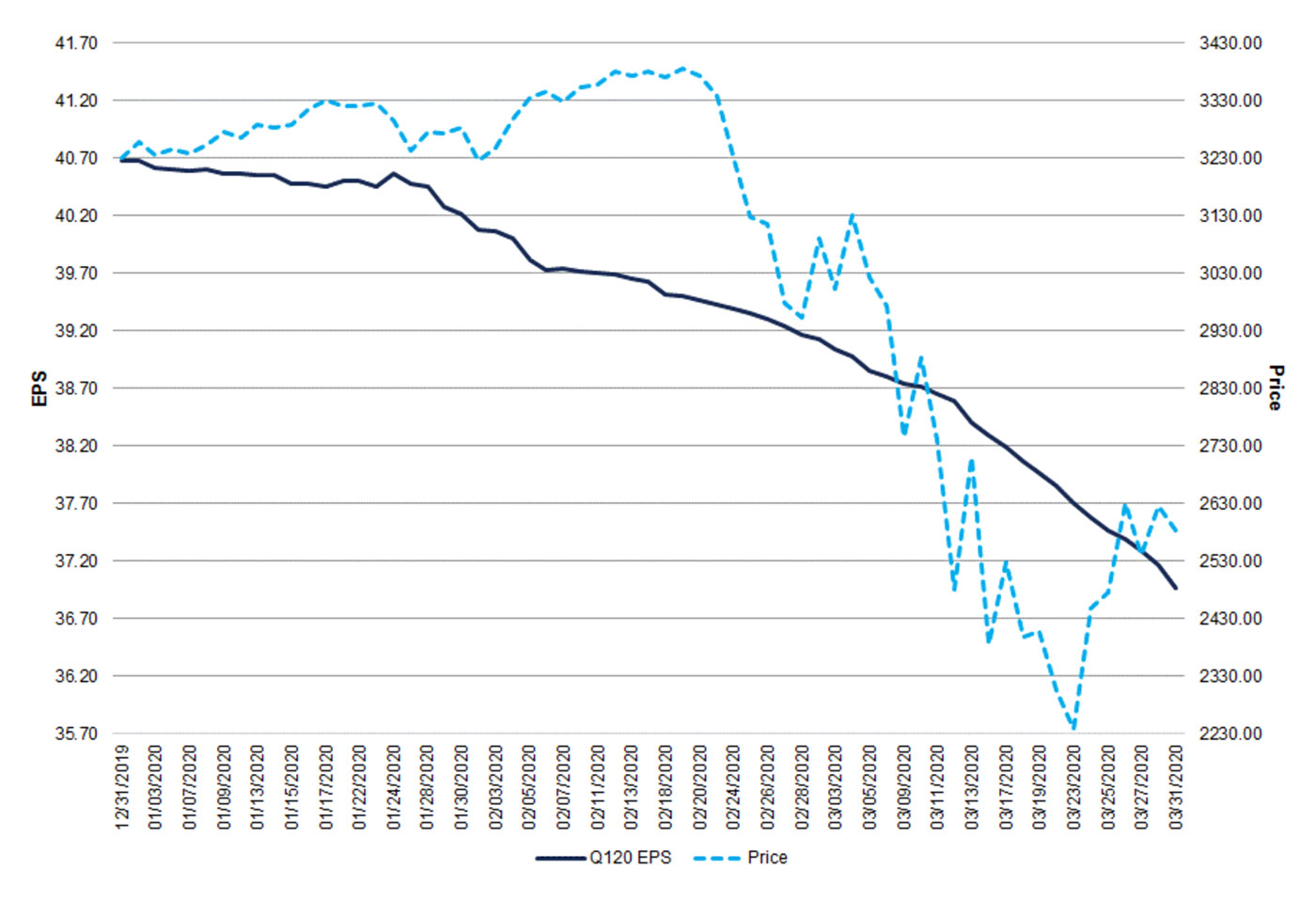

“With numerous industries in the U.S. forced to reduce capacity or close altogether due to social distancing policies implemented to help reduce the spread of the coronavirus, analysts made substantial cuts to earnings estimates for companies in the S&P 500 during the first quarter, particularly during the month of March. The Q1 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q1 for all the companies in the index) declined by 9.1% (to $36.97 from $40.68) from December 31 to March 31. …

“As the bottom-up EPS estimate for the index declined during the quarter, the value of the S&P 500 also decreased during this same period. From December 31 through March 31, the value of the index decreased by 20.0%. … The first quarter marked just the fourth time in the past 20 quarters in which both the bottom-up EPS estimate and the value of the index decreased in the quarter.”

Source: FactSet, as of 4/3/2020

FactSet provides an analysis of the following key metrics:

- “Earnings Growth: For Q1 2020, the estimated earnings decline for the S&P 500 is -7.3%. If -7.3% is the actual decline for the quarter, it will mark the largest year-over-year decline in the earnings reported by the index since Q3 2009 (-15.7%).

- Earnings Revisions: On December 31, the estimated earnings growth rate for Q1 2020 was 4.3%. All eleven sectors have lower growth rates today (compared to December 31) due to downward revisions to EPS estimates.

- Earnings Guidance: For Q1 2020, 72 S&P 500 companies have issued negative EPS guidance and 32 S&P 500 companies have issued positive EPS guidance.

- Valuation: The forward 12-month P/E ratio for the S&P 500 is 15.3. This P/E ratio is below the 5-year average (16.7) but above the 10-year average (15.0).

- Earnings Scorecard: For Q1 2020 (with 20 companies in the S&P 500 reporting actual results), 15 S&P 500 companies have reported a positive EPS surprise and 14 S&P 500 companies have reported a positive revenue surprise.”

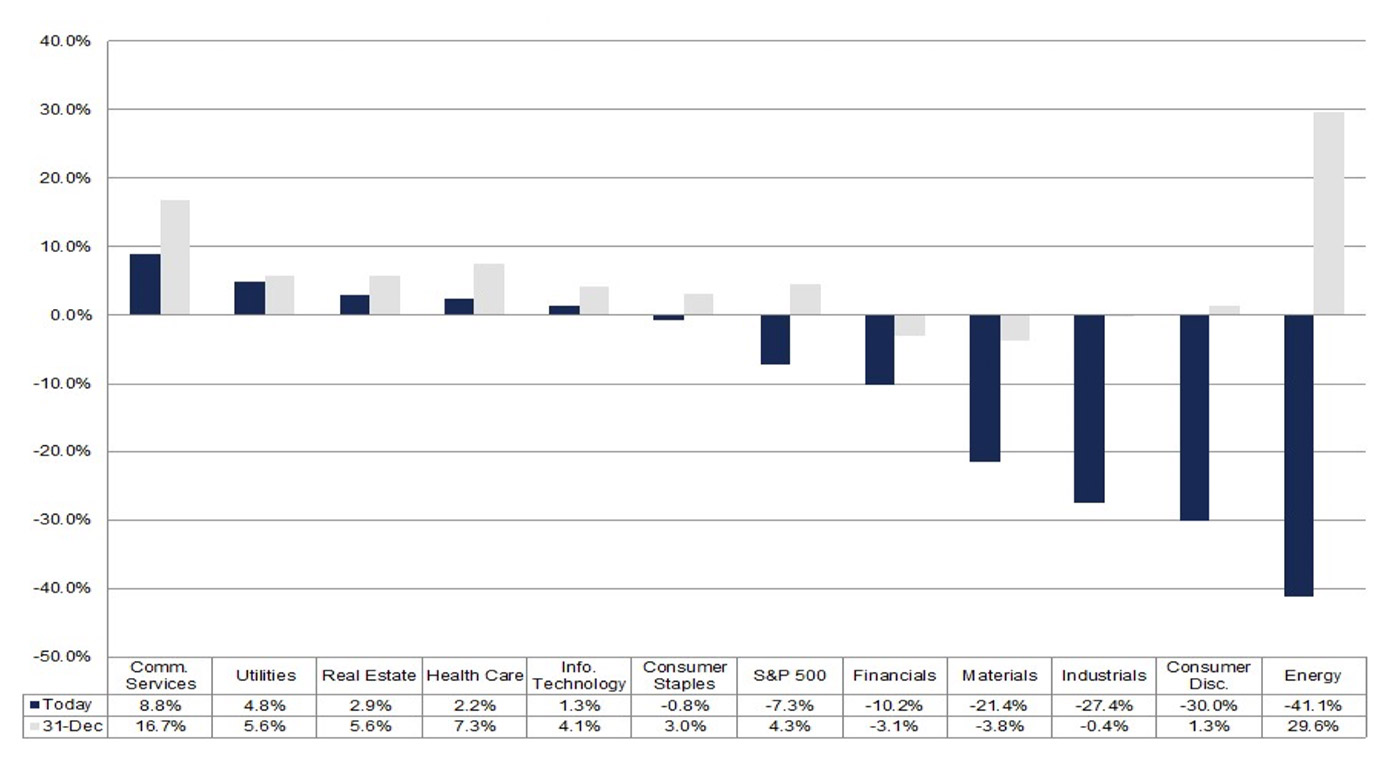

As far as sectors are concerned, FactSet notes the weakest sectors are likely to be Energy, Consumer Discretionary, Industrials, and Materials (in order of weakest first). The strongest sectors are expected to be Communication Services, Utilities, Real Estate, and Health Care.

Source: FactSet

For the overall calendar year 2020, FactSet’s analysis of analyst estimates is calling for a 4.5% decline in corporate earnings, although revenues are expected to increase by 0.8%.

The outlook by quarter varies widely. Says FactSet,

- “For the first quarter, analysts expect S&P 500 companies to report a decline in earnings of -7.3% and growth in revenues of 1.5%.

- For Q2 2020, analysts are projecting an earnings decline of -15.1% and a revenue decline of -2.1%.

- For Q3 2020, analysts are projecting an earnings decline of -4.8% and revenue growth of 0.9%.

- For Q4 2020, analysts are projecting earnings growth of 1.7% and revenue growth of 2.8%.”