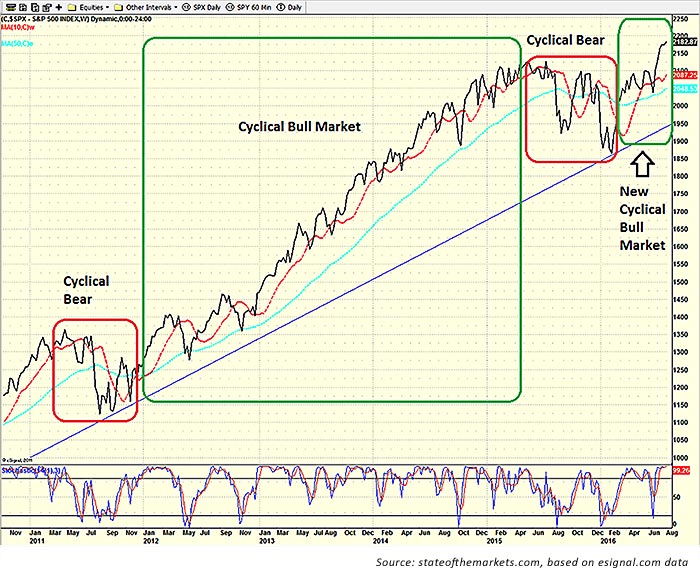

The major market indexes continued to power to new all-time highs last week, building on the momentum that took hold following the stronger-than-expected July employment report released August 5.

In fact, last Thursday (August 11), all three of the most-watched U.S. stock market indexes closed at new all-time highs, the first time for that simultaneous event, says StateoftheMarkets.com, since December 31, 1999. The S&P 500, according to The Wall Street Journal, entered this week with nine new record highs in 2016.

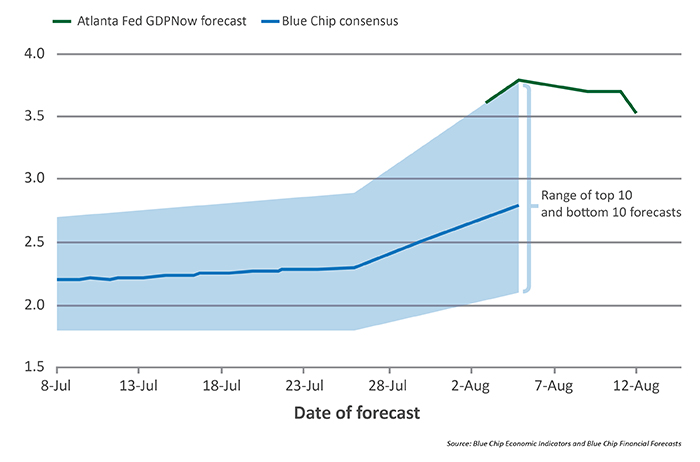

The bulls argue that more jobs and higher wages mean a brighter outlook for both the economy and corporate earnings going forward. Those market skeptics who had been pointing to the very poor Q2 GDP report (showing 1.2% year-over-year U.S. economic growth) are now seeing far more upbeat projections for Q3 GDP. Barron’s notes that the Atlanta Fed’s GDPNow tracking estimate is projecting a Q3 GDP figure of 3.8%, and the New York Fed has a “more modest, but still respectable 2.6% growth rate.”