There are three Super Sectors used in the financial markets, and each has three to four major subsectors. Each of those subsectors is composed of several industry classifications.

The Defensive Super Sector is composed of the Consumer Defensive, Health Care, and Utilities subsectors. Defensive stocks are primarily companies that distribute products for consumers that are in demand regardless of economic cycle and will usually outperform during a recession.

The Cyclical Super Sector is composed of the Basic Materials, Consumer Cyclical, Financial Services, and Real Estate subsectors. This cyclical grouping has a heavy weighting toward consumer discretionary goods and services. Based on theory, this sector should outperform as the economy expands and employment rises.

The Sensitive Super Sector is composed of the Communication Services, Energy, Industrials, and Technology subsectors. The Sensitive Super Sector tends to cycle last in a bull market. Theory considers it to be primarily economically sensitive stocks associated with expansion and business investment. The grouping also has a leaning toward new technologies for both businesses and consumers. However, purchase or investment in technology tends to occur most heavily at the peak of bull markets.

SUPER SECTOR INDEX RELATIVE PERFORMANCE

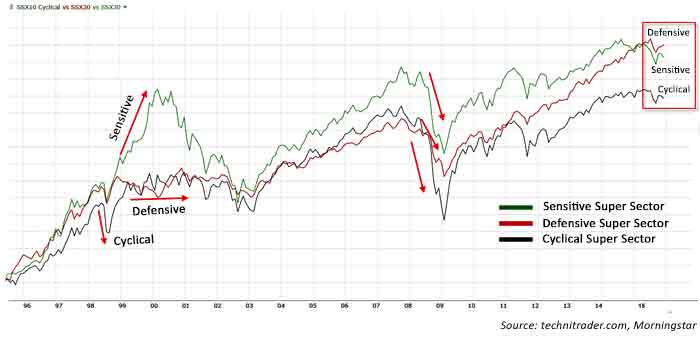

A major deviation has occurred in the overall Super Sector cycle, presenting some heightened risk for investors. The exhibit shows all three Super Sector trends over a 20-year time frame.

The normal cycle would maintain a separation between the sectors. Theoretically, each should cycle sequentially through the life of a bull market. A good example of a strong sector rotation cycle is mid-1998, when the Sensitive Super Sector rose, while the Cyclical Super Sector fell and the Defensive Super Sector shifted sideways. However, deviations began shortly thereafter. Harmonious patterns then began again in 2002.

All three Super Sectors collapsed in unison during the banking/credit/real estate debacle, and all recovered at the identical time. The Sensitive Super Sector gained faster than the Defensive Super Sector during 2009–12, when the recession was deepest. The opposite should have occurred.

Since 2012, all three sectors were in normal harmony until 2014, when the Defensive Super Sector advanced on the Sensitive Super Sector, which is an anomaly in sector rotation cycle theory. The economic recession ended in 2012, and the economy has been expanding. The Defensive Super Sector should be trending down, the Cyclical Super Sector should be peaking, and the Sensitive Super Sector should be leading, based on theory.

This is a major deviation of the sector rotation cycle theory. This poses hidden risk factors in 2016 for investors who adhere strictly to the sector rotation cycle as an investment methodology.

Martha Stokes, CMT, is the co-founder and CEO of TechniTrader and a former buy-side technical analyst. Since 1998, she has developed over 40 TechniTrader stock and option courses. She specializes in relational analysis for stocks and options, as well as market condition analysis. An industry speaker and writer, Ms. Stokes is a member of the CMT Association and earned the Chartered Market Technician designation with her thesis, "Cycle Evolution Theory." technitrader.com

Martha Stokes, CMT, is the co-founder and CEO of TechniTrader and a former buy-side technical analyst. Since 1998, she has developed over 40 TechniTrader stock and option courses. She specializes in relational analysis for stocks and options, as well as market condition analysis. An industry speaker and writer, Ms. Stokes is a member of the CMT Association and earned the Chartered Market Technician designation with her thesis, "Cycle Evolution Theory." technitrader.com