Helping clients climb down the mountain

Behavioral research has documented many of the obstacles that trip up self-directed investors—the first step in gaining knowledge is often one of self-awareness.

As financial advisors, we wear many hats: detective, analyst, strategist, architect, salesperson, coach, and countless more. After days, weeks, months (and sometimes even years) of fighting our way to top-of-mind awareness with a potential client, we next have to overcome our main opponent: human nature.

As humans, we all come standard with various features—wonderful things like nurturing instincts, unstoppable creative powers, altruistic responses to protect those we care about. And then there’s the other side. The dark side.

The same fight-or-flight response that used to save us from saber-toothed tigers now leads us to panic and quit on our investments just when it’s prime time to own them. The same natural-born curiosity and confidence that nudged us to expand and explore when we were nomads today translates into a bias that, though humorous at times, is absolutely devastating to investors.

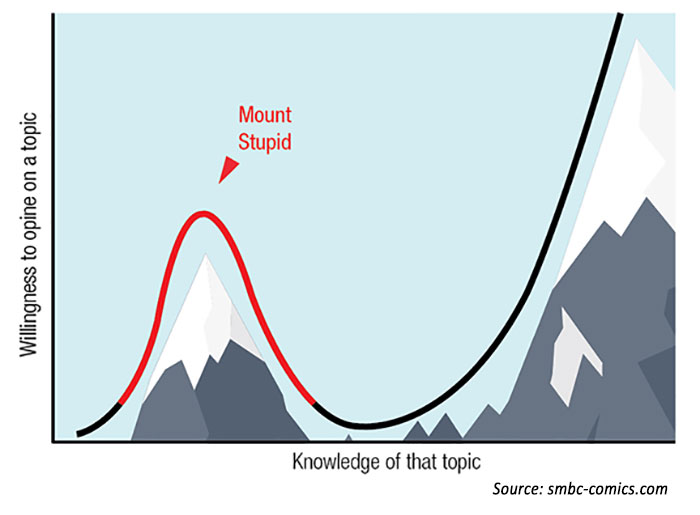

Climbing the mountain

In the world of investing, information is power. The comic sketch above (inspired by Zach Weiner’s original) sums up many of the conversations we all have when a highly trained—and for many of us, obsessed—advisor meets a client that spends hours each day poring over stock data, never misses an episode of “Mad Money,” and is a self-proclaimed financial guru.

In academia and most professions, the over-willingness to expound on a topic on which you are not an expert may be embarrassing and damaging to your reputation. In investing, the danger becomes not just opinion, but action. Instead of simply being bad for one’s reputation, “Mount Stupid” can crush an investor’s financial future.

4 levels of competence

Back in my coaching days, we used to talk about the four levels of competence:

1. Unconscious incompetence: “I don’t know that I don’t know.”

The peak of “Mount Stupid”—a lack of awareness of all that goes into a skill or particular expertise.

Example: “Why did he call a pass play there?! They should have run the ball!” In this case, the armchair football expert knows better than the coach with years of experience, a Super Bowl ring, and seven days of game planning and film study—and has no clue about the thought and analysis that went into that game-day decision

2. Conscious incompetence: “I know that I don’t know.”

The stage at which one becomes open to learning.

Example: Even very intelligent people realize that the ins-and-outs of the tax code or long-term health care planning might best be left to the experts.

3. Conscious competence: “I know that I know.”

Where a person can perform a skill reliably well, but needs to concentrate on it.

Example: An apprentice electrician who is well trained, but must consciously follow a mental checklist.

4. Unconscious competence: “I forgot that I know.”

A skill so ingrained that it is second nature and can be performed instinctively.

Example: You are reading this article without having to sound out the words. You are so competent a reader you no longer need to think about the reading process. The “natural” final stage of learning.

Many investors I meet for the first time are firmly still in Level 1 when it comes to just about anything related to their finances, much less sophisticated investing concepts. They simply don’t know that they don’t know. Even worse, many of them aren’t at all hesitant when it comes to expressing opinions and often taking action. As behavioral finance tells us, that is frequently the wrong action at precisely the wrong time.

Dunning-Kruger study

About a year ago, I came across a well-known study from 1999 by David Dunning and Justin Kruger at Cornell University, “Unskilled and Unaware of It: How Difficulties in Recognizing One’s Own Incompetence Lead to Inflated Self-Assessments,” first presented in The Journal of Personality and Social Psychology. Here’s a quick summary from the abstract:

“People tend to hold overly favorable views of their abilities in many social and intellectual domains. The authors suggest that this overestimation occurs, in part, because people who are unskilled in these domains suffer a dual burden: Not only do these people reach erroneous conclusions and make unfortunate choices, but their incompetence robs them of the metacognitive ability to realize it.

“Across four studies, the authors found that participants scoring in the bottom quartile on tests of humor, grammar, and logic grossly overestimated their test performance and ability. Although their test scores put them in the 12th percentile, they estimated themselves to be in the 62nd.”

This is like asking a room of people to close their eyes and raise their hand if they think they are an above-average driver. Usually around 95% of the room will say yes. That is not possible, unless you happen to be speaking to a room full of professional race-car drivers.

I have spent years trying to figure out a way to help the Level 1 investor. Not necessarily how to win the Level 1 investor over as a client, but simply to move them from Level 1 to Level 2 to get the learning process started. In other words, how to (politely) help them realize (on their own) they don’t really know what they’re doing. Around the time I read this study, I came up with the idea to give a short, 10-question quiz at the beginning of all of my seminars and speaking engagements.

The quiz

Before giving the quiz, I emphasize that members of the audience will not be turning in the quiz. Also, they won’t have to show their score to anyone else. It is strictly for their eyes only. (Do not skip this step.) Next, I ask the room to rate, in a box in the upper-right corner, how they think they will do on a basic 10-question, multiple-choice quiz about investing and financial planning issues.

Here are a few sample questions to give a flavor for the quiz. Answers can be found at the conclusion of the article.

How much greater are your Social Security benefits if you take them at age 70 rather than claiming at age 62?

A. 34%

B. 52%

C. 76%

D. 100%

What proportion of 65-year-olds will need long-term care in their life?

A. 28%

B. 46%

C. 68%

D. 94%

What is the cost of one year of semi-private (shared room) long-term care in Wisconsin?

A. $8,500

B. $34,600

C. $56,045

D. $90,064

What has been the real compound annual growth rate of the S&P 500 over the last 15 years?

A. -2.04%

B. 1.91%

C. 4.53%

D. 7.92%

Over a long period of time, which has a bigger impact on your investment results?

A. The negative impact of missing the 10 best days of the S&P 500

B. The positive impact of missing the 10 worst days of the S&P 500

Although they don’t have to turn in their quiz, from the many people who have approached me after my talks (and from papers left behind), I typically see a 9 or 10 expected score. The typical achieved score is usually between 2 and 5. This represents at least a 100% overestimation of “financial competence.”

After expecting to score a 10, and then scoring a 3, I find people to be much more open and engaged in an educational presentation that is truly focused on teaching some principles and concepts that can dramatically improve their financial outcomes.

Let me emphasize that I do not believe that the prospects I meet lack intelligence or the motivation to become more informed about their finances and investing. They would not come to a presentation in the first place if they were not interested in learning more.

But it is an unfortunate truth that many investors simply “do not know what they don’t know.” It is incumbent upon committed advisors to have the patience, skill, and tools to overcome that in a very professional manner.

I find that, especially in the area of investment risk management, some simple concepts can begin to demonstrate to clients why they should not allow their hard-earned assets to be at the mercy of volatile markets. I believe that if you can help investors make better, more informed decisions, you have succeeded in an extremely important aspect of the advisory profession.

Answers

C. 76% Source: Boston College Center for Retirement Research

C. 68% Source: LTC.gov

D. $90,064 Source: Annual Genworth LTC Study

B. 1.91% Source: moneychimp.com

B. The positive impact of missing the 10 worst days of the S&P 500 Source: Meb Faber Research

Tony Hellenbrand is president and partner at Fox River Capital, located in Appleton, Wisconsin. In addition to client-focused financial and investment planning, Mr. Hellenbrand is skilled at working with business owners on succession planning and exit strategies. He has earned the Retirement Income Certified Professional (RICP) designation from the American College. FoxRiverCapital.com.

Disclosure: The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Securities offered through ProEquities, Inc. a Registered Broker/Dealer, member of FINRA & SIPC Advisory Services offered through Investment Advisors, a division of ProEquities, Inc., a Registered Investment Advisor. Hellenbrand Financial is independent of ProEquities, Inc