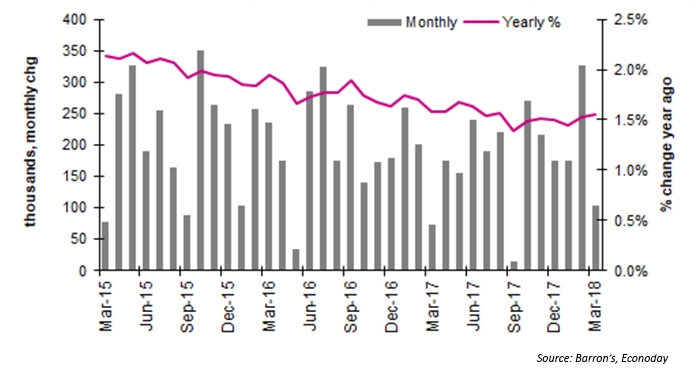

The March jobs report from the Bureau of Labor Statistics (BLS) missed estimates by a wide margin, with nonfarm payrolls rising 103,000 versus estimates of 180,000. However, an extremely strong February report was revised up to 326,000 total jobs, while January was revised downward by 63,000 jobs.

According to The Wall Street Journal, hiring has picked up overall in 2018. It reported this past weekend after Friday’s job report came in with gains and an unemployment rate of 4.1%,

“That extended a historic streak—employers have added to payrolls for 90 straight months in the longest continuous jobs expansion on record. And it picked up of late: For the first three months of the year, hiring averaged 202,000 a month, up from 182,000 a month in 2017.”

Note, however, that the average for Q1 of 202,000 monthly jobs growth is below the Q4 2017 average of 221,000.

FIGURE 1: NONFARM PAYROLLS (MONTHLY AND YEARLY CHANGE)

New Federal Reserve Chairman Jerome Powell was upbeat on the jobs recovery and the overall state of the economy in a speech to the Economic Club of Chicago on Friday, April 6, the same day as the March jobs report release. Powell said, in part,

“After what at times has been a slow recovery from the financial crisis and the Great Recession, growth has picked up. Unemployment has fallen from 10 percent at its peak in October 2009 to 4.1 percent, the lowest level in nearly two decades. Seventeen million jobs have been created in this expansion, and the monthly pace of job growth remains more than sufficient to employ new entrants to the labor force. The labor market has been strong, and my colleagues and I on the Federal Open Market Committee (FOMC) expect it to remain strong. Inflation has continued to run below the FOMC’s 2 percent objective, but we expect it to move up in coming months and to stabilize around 2 percent over the medium term.

“Beyond the labor market, there are other signs of economic strength. Steady income gains, rising household wealth, and elevated consumer confidence continue to support consumer spending, which accounts for about two thirds of economic output. Business investment improved markedly last year following two subpar years, and both business surveys and profit expectations point to further gains ahead. Fiscal stimulus and continued accommodative financial conditions are supporting both household spending and business investment, while strong global growth has boosted U.S. exports.”

Bespoke Investment Group highlighted two other aspects of the job report in their weekly market update:

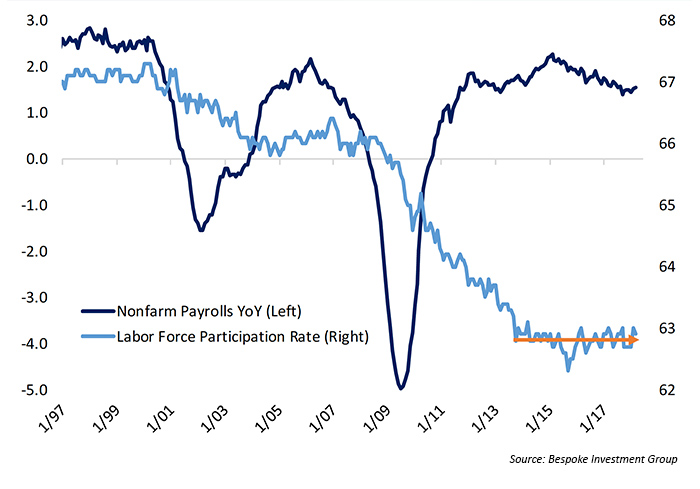

“The labor force participation rate (LFPR) continues to move sideways, but keep in mind that demographics should be driving it lower, so a sideways trend is actually quite positive from a cyclical perspective.”

FIGURE 2: JOBS GROWTH VS. LABOR FORCE PARTICIPATION RATE

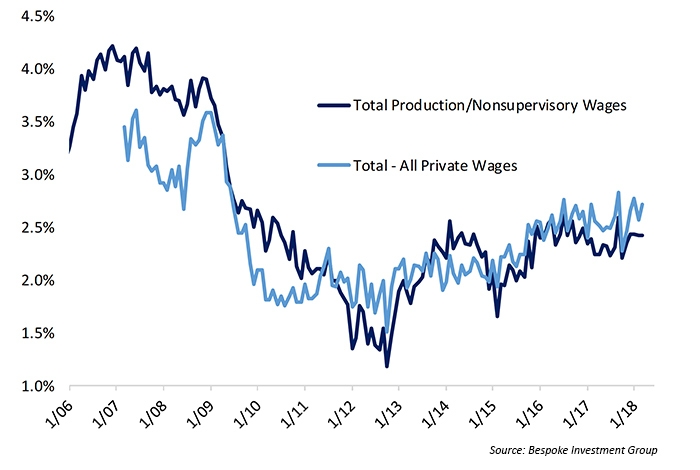

Bespoke also noted regarding wage growth, “It was also an okay month for wage growth. As shown in the chart (Figure 3), wage growth has continued to move higher over the last few years but is by no means accelerating dramatically.” Average hourly earnings for March were up 2.7% from the previous year, which was right about at expectations in a continuing slow, but steady, trend higher over the past two to three years.

FIGURE 3: WAGE GROWTH IMPROVES SLOWLY