Time flies when you’re having fun. Although 2015–2016 was certainly a turbulent time to be in the stock market, and despite a somewhat surprising U.S. presidential election result (to most), the Dow Jones Industrial Average, S&P 500, and NASDAQ have all managed to find repeated new highs over the last six months. This, indeed, is fun! However, as one of my mentors, Charles Kirkpatrick II, told me this past year, “Every bull market ends with a bear market.”

Human beings are the most sophisticated living organisms on Earth. Our brains, infinitely complex and ever-evolving, have learned how to generate fire and produce fuel. We have combined these discoveries with combustion and physics and attached turbine engines to the plane on which I’m flying at roughly 30,000 feet in the air at approximately 415 mph. The cabin is pressurized, heated (since we’d all freeze at this altitude), and I have a cord plugged into an electrical socket that is charging the battery that powers my laptop computer that I’m using to type up this article.

We are truly amazing mammals, but we have our shortcomings. One of the pitfalls of our complex craniums is a little phenomenon called recency bias. Recency bias is the emotional tendency to forget—or put less weight on—events that have taken place in the distant past. Of course, “distant past” can be defined in many ways. For the sake of this article, we’ll say that recency bias causes us to put more weight on what’s happened to us in the last couple of years, while storing our experiences from three to four years ago (and beyond) somewhere in a dusty, dark corner in a filing cabinet within our brain.

Point being, we tend to care less about what happened long ago and favor information we can readily bring to consciousness using shorter-term memory in our decision-making processes.

It’s sometimes mind-bending when I consider the fact that I’ve been in this field for almost 16 years now. Starting my career just a couple of weeks before the World Trade Center attack, I’ve had the fortunate or unfortunate experience (depending on how you look at it) of living through, and taking our clients through, not one, but two stock market crashes—and those experiences have taught me a lot more than any financial class or book could teach.

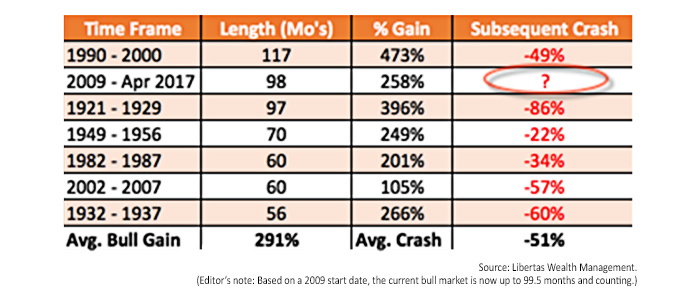

Below is a table that illustrates every bull (up) market since the Great Depression, the length of each bull market (in months), the total cumulative gain, and the market crash that took place after. Notice that we’re living in the second-longest bull market in history.

TABLE 1: LENGTH OF BULL MARKETS SINCE GREAT DEPRESSION

According to the figures in the table, the average bull market lasts just under seven years and has an average gain of 291%. The average subsequent crash results in a loss equivalent to roughly half of what you started with. Said another way, if an investor managed to grow his or her retirement savings to $1,000,000, the average market crash (which only takes about 18 months, by the way) would wipe out an average of $510,000, leaving only $490,000.

Another thing to keep in mind is that these are just averages. This means that half of the expected outcomes are better and half are worse. We can only hope that the next crash (and the one after that) will be “better” than the average.

Because I live, breathe, and many times dream about my work, I don’t forget much about the past. However, the psychological phenomenon of recency bias still perplexes me as I observe the cycle of human behavior in real time.

The longer the market goes up, the more people seem to forget about how bad things can get. They become complacent, shun reality even when it’s written in plain English, and many professionals in the financial industry will become especially defensive when numbers like these are published—because even financial practitioners (most of them anyway) don’t want to accept reality.

As bull markets become more mature and long-in-the-tooth, we start to hear more people complaining about how their co-worker, sibling, or golfing buddy made more money than they did. In other words, greed starts to set in as bull markets get old. We also start to talk to more investors who say they’re “just going to manage their own money.”

When you consider the market goes up for roughly seven years on average before crashing, as well as the not-so-well-known fact that we’re living in the ninth year of this bull market (the second-longest in history), it only makes sense that the do-it-yourself investor might start to feel a little euphoric and even godlike. After all, they simply put their money into a portfolio of investments and let it ride with occasional, albeit small, changes … and it’s done nothing but rise in value for nine years. What could go wrong?

Ahhh … recency bias.

So, what’s the answer? When is the market going to crash? The truth is, I have no idea. Anyone who professes to know is lying to you, delusional, or both. However, there is a better way to protect principal against catastrophic market events.

I’m not talking about diversification. That can help a little, but honestly, it’s not going to protect a portfolio from a 30%–45% loss of a client’s hard-saved retirement assets.

I’m referring to trend following and technical analysis, which is the study of the recent past, current trends, and the prevailing “temperature” of the markets (stocks, bonds, commodities, currencies, etc.). When implementing a trend-following process, you’re not trying to predict what the market is going to do—you’re simply adjusting an investment portfolio based on the current (recent) trends in the market.

Understand that, using a trend-following strategy, one will not get all of the upside in the market. More importantly—and the whole purpose of using this type of strategy—is that investors won’t get all of the downside either.

The only way to get all of the upside gains in the market is to go “all-in,” buy a bunch of investments, and stay in them through the entire market cycle. Of course, it should go without saying that, by getting all of the upside, you also must accept all of the downside losses as well.

I believe working with an investment professional that has a risk-management strategy in place makes a great deal of sense—one who can adjust market exposure or exit the markets altogether when the market starts to throw up red flags.

There is no perfect investment strategy that achieves all of the gains in the market while also missing all of the losses. Desiring such an outcome is synonymous with chasing unicorns and Sasquatch. But one can certainly enhance the probabilities for long-term success.

When it comes to managing money, we focus first on defending portfolios from losses, and then on seeking competitive returns. We do not believe that strong risk management and portfolio growth are incompatible, and we spend a lot of time educating clients on our philosophy.

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. A version of this article first published on June 2, 2017, at http://libertaswealth.com/.

The opinions in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. The opinions expressed do not necessarily represent the views of TD Ameritrade and its affiliates. Investing involves risk, including loss of principal. Libertas Wealth Management Group, Inc., is a NAPFA-affiliated, fee-only registered investment advisory (RIA) firm.

Adam Koos, CFP, CMT, CFTe, CEPA, is the president and portfolio manager at Libertas Wealth Management Group Inc., a NAPFA-affiliated, fiduciary registered investment advisor firm in Columbus, Ohio. Since founding the firm in 2001, he has earned local and national recognition, including being named one of the Top 100 Most Influential Financial Advisors in the U.S. by Investopedia and receiving the Torch Award for Ethics and Trust from the Better Business Bureau. Mr. Koos holds B.S. degrees in finance and behavioral psychology from The Ohio State University. www.libertaswealth.com

Adam Koos, CFP, CMT, CFTe, CEPA, is the president and portfolio manager at Libertas Wealth Management Group Inc., a NAPFA-affiliated, fiduciary registered investment advisor firm in Columbus, Ohio. Since founding the firm in 2001, he has earned local and national recognition, including being named one of the Top 100 Most Influential Financial Advisors in the U.S. by Investopedia and receiving the Torch Award for Ethics and Trust from the Better Business Bureau. Mr. Koos holds B.S. degrees in finance and behavioral psychology from The Ohio State University. www.libertaswealth.com