Active managers debate: ETFs vs. mutual funds?

Active managers debate: ETFs vs. mutual funds?

ETFs continue to gain popularity with fund managers, investment advisors, and investors—reflecting ever-increasing familiarity and diversication—but they also have their drawbacks.

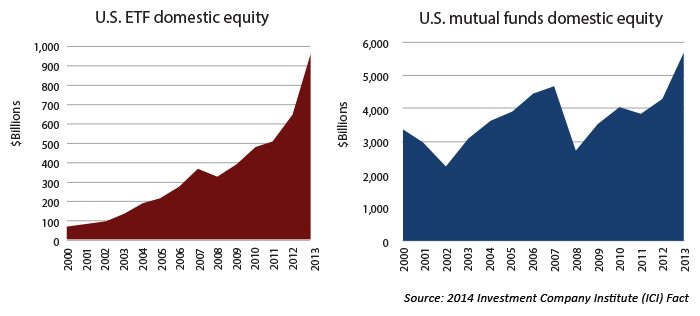

The mutual fund industry is still the 800-pound gorilla of the financial market, but it is a gorilla on a diet. The growth trajectories of domestic-equity mutual funds and exchange-traded funds (ETFs) are dramatically different. Since 2000, domestic-equity-ETF assets have increased by more than 1,520%. Comparable mutual fund assets are up 70%.

Naturally, those numbers represent a fallacy that every small-cap investor can explain: It is much easier to exponentially grow from a small beginning than as an established mammoth. But the growth in ETFs is undeniable, with a recent Ernst and Young report calling for “annual growth rates of 15-30% globally in the next five years … with active and smart beta ETFs two of the hottest growth areas.”

Growth trajectory of ETFs vs. mutual funds

Jeremy Siegel, senior strategy advisor with WisdomTree Investments, currently the industry’s fifth-largest ETF provider in the U.S., foresees a time when ETFs will overshadow mutual funds. Driving that growth, he maintains, will be the ETF design compatibility in the indexing space and tax advantages, and—most of all—the flexibility people want in managing their money.

Mutual funds were the original investment vehicle of choice for active managers and remain so for many. As the fund families added investment categories and balanced equity funds with bond and money-market funds, reallocating client assets in response to market conditions became cost-efficient. No-fee mutual fund platforms allowed managers to move beyond using the funds of a single investment company to use the funds of several different companies, picking and choosing among the best-performing options.

The key idea is that buy-and-hold strategies and active trading strategies can have very different cost profiles.

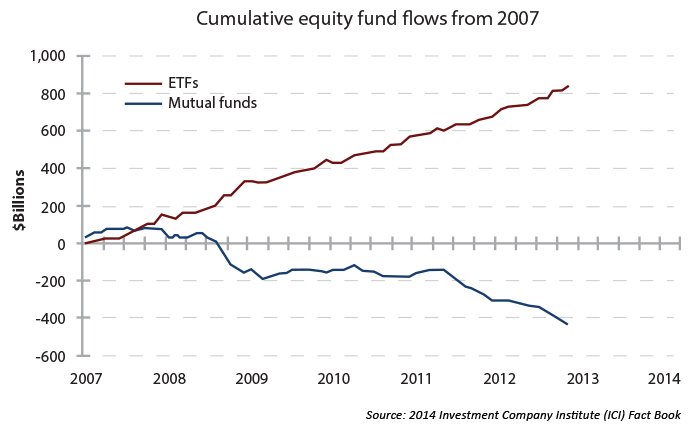

But the popularity of using mutual funds for active management suffered a setback from the “timing” scandal of 2003. Mutual funds began imposing restrictions and early-redemption penalties designed to limit the frequency of exchanges between funds. Even some brokerage firms began imposing penalties for frequent trading in mutual funds, regardless of whether or not the fund itself restricted trading frequency.

The timing was perfect for the emerging ETF industry. Investors still wanted to be able to buy and sell at their discretion. The structure of an ETF removed the potential for a fast-trading investor to impact the returns of longer-term holders. Because ETFs trade similar to stocks, with prices continually adjusting to market conditions and the funds’ underlying holdings, late trading and stale price arbitrage became a non-issue. In addition to trading flexibility, ETFs offered tax advantages and lower expense ratios. By late 2007, ETFs were outpacing the mutual fund industry in terms of equity fund flows.

Equity holdings shift from mutual funds to ETFs

In the active-management arena, the trading flexibility of the ETF has made them the go-to tool for many strategies. But whether they are a superior trading vehicle is far from consensus opinion. “The reflexive notion that ETFs cost less simply based on their low expense ratios, and are more cost-effective than mutual funds, is not entirely true,” Guggenheim Investments points out in its Rydex Funds report “A Comparison of ETFs and Mutual Funds—The True Cost of Investing.” (Note: Guggenheim provides a variety of both ETFs and mutual funds.)

Guggenheim acknowledges the significance of the “ETF versus mutual fund” debate for managers and investors, saying, “The key idea here is that buy-and-hold strategies and active trading strategies can have different cost profiles when taking into account all of the relevant costs and the trading frequency.”

What is the answer to the ETF vs. mutual fund debate? “It all depends.”

In addition to internal expense ratios, the report explains, ETF investors typically must navigate transaction or brokerage commission fees to purchase and sell ETFs, bid/ask spreads (which represents the cost for selling and buying the ETF), and the potential for intraday pricing premiums or discounts based on supply and demand.¹

When comparing the cost of using mutual funds versus ETFs in an active strategy it is easy to focus on the known costs—expense ratios and commission costs. The expense ratio includes management fees, 12b-1 fees and other expenses that are deducted from a fund’s assets or charged to all shareholder accounts. ETFs, because they trade on exchanges similar to stocks, incur a sales commission, while no transaction fee (NTF) mutual funds can be traded commission-free. Not all funds are NTF, however, but these costs can still be known in advance and factored into an investment decision.

Other costs mutual fund investors need to consider include whether or not the fund imposes transaction fees if shares are not bought and sold directly through the mutual fund provider or on an NTF platform, holding period penalties such as redemption fees, sales charges, exchange fees, and account-related fees.

For mutual funds, the biggest unknown is the actual cost of the fund’s shares at the market’s close. Because mutual fund orders are processed based on the net asset value (NAV) at the U.S. market’s close at 4 p.m. EST, the final transaction could be priced higher or lower than the manager might have anticipated.

With ETFs, the share cost is known at the time the order is executed; however, other costs come into play. The price of a particular ETF is based on supply and demand. The ETF could trade at a premium or a discount to its underlying NAV depending on market conditions. Bid-ask spreads also influence the price of an ETF. This is the difference between the price a buyer is willing to pay (bid) for a security and the seller’s offering (ask) price. Bid-ask spreads can vary considerably based on market volatility, the underlying stocks that make up the ETF, liquidity, the issuing company and other factors. One effect of the bid-ask spread is that a buyer may pay more than the value of the individual stocks that make up the ETF. These unknowns make “best execution” practices for trading ETFs essential.

The issue of end-of-day pricing and volatility into the market close is an important one, as many fund managers find the “one price a day” nature of mutual funds more conducive to consistent strategy and trading execution—and “cleaner” for backtesting strategies—than intraday-traded ETFs.

Regardless of supporting factors and costs, ETFs are transforming the active manager’s trading arsenal. As managed equity ETFs proliferate, reflecting the investor’s desire to have a manager actively selecting investments he or she believes are best-of-class, active managers may find less reason to actively trade mutual funds to manage market risk and target opportunities.

Then again, one certainty in life is uncertainty. The giants of the mutual fund industry, Vanguard, Fidelity, and others, have moved to develop their own ETF products, inherently recognizing that each product has suitability depending on a manager’s or investor’s needs and strategies. So the answer to the “ETF versus mutual fund” debate is an inconclusive draw—an unexciting but sensible response of “it all depends.”

¹For a more in-depth look at these costs, the full report can be found at https://www.guggenheiminvestments.com/rydex

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

Linda Ferentchak is the president of Financial Communications Associates. Ms. Ferentchak has worked in financial industry communications since 1979 and has an extensive background in investment and money-management philosophies and strategies. She is a member of the Business Marketing Association and holds the APR accreditation from the Public Relations Society of America. Her work has received numerous awards, including the American Marketing Association’s Gold Peak award. activemanagersresource.com

Linda Ferentchak is the president of Financial Communications Associates. Ms. Ferentchak has worked in financial industry communications since 1979 and has an extensive background in investment and money-management philosophies and strategies. She is a member of the Business Marketing Association and holds the APR accreditation from the Public Relations Society of America. Her work has received numerous awards, including the American Marketing Association’s Gold Peak award. activemanagersresource.com