Why passive investors get hammered

Why passive investors get hammered

“If all you have is a hammer, everything looks like a nail.”—Abraham Maslow

“If I had a hammer, I’d hammer in the morning, I’d hammer in the evening, all over this land.”—Pete Seeger and Lee Hays, 1949.

I don’t know if American psychologist Abraham Maslow ever met Pete Seeger, but they seem to agree about the use of a basic hand tool. Over the years, I have heard many variations of Maslow’s statement, though the meaning has remained the same—those good with a hammer tend to see every new challenge as a nail.

Unfortunately, many investors get caught up in Maslow’s limited tool selection by restricting their choice of investment strategies needed to reach their financial goals. In reality, investors would probably be better off if they could diversify their selection of investment strategies to add depth to their portfolios.

In today’s investment world, however, the “hammer” tends to be in the form of passive asset-allocation strategies that distribute portfolios among various stock and bond asset classes. A typical allocation might be 60% stocks and 40% bonds, usually based on computerized models following the concept of modern portfolio theory as developed in the 1950s by Dr. Harry Markowitz.

Using only asset allocation is like a toolbox containing only a hammer—useful in some applications, but hardly a universal wrench.

And what a hammer it is! Asset-allocation strategies using low-cost index funds, and now ETFs, have become the 800-pound gorilla of the investment world.

Don’t get me wrong. I’m not saying that asset-allocation strategies do not have a place in an investor’s portfolio. What I am saying is that asset allocation has its shortcomings and should not be the only strategy employed by investors who want to meet their financial goals. Using only asset allocation is like a toolbox containing only a hammer—useful in some applications, but hardly a universal wrench.

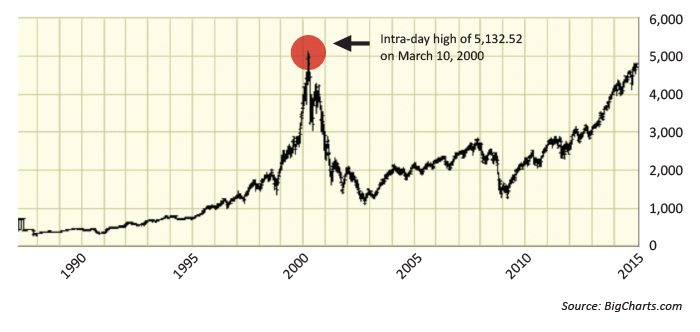

NASDAQ Composite historical performance

Unfortunately, limited tool selection can affect the quality of the investment. For example, risk management in a passive asset-allocation portfolio is generally expected to come from low correlations among the asset classes chosen. The only problem is that actual experience during bear markets has shown that these low correlations can increase during down market cycles (remember 2008?). The result is that asset allocation’s tool to manage risk may disappear just when you need it most.

The same goes for maximum portfolio drawdown, a statistic indicating the portfolio’s largest drop from a peak value to a subsequent valley. During the two bear markets that occurred in 2000–2002 and then again in 2007–2009, the S&P 500 Index dropped in value more than 40% and 50%, respectively. Since passive asset allocation was the only tool in many toolboxes, there was no way for portfolios to escape the carnage. What if you needed your money at the bottom of the drawdown? It would be your tough luck.

Asset allocation believers offer the standard line that the market will eventually regain value, and for proof, they point to the fact that every drawdown has eventually been erased by the market. Well, every one except for the NASDAQ Composite’s 75%-plus drawdown, which has still not been erased even after more than 14 years of market action. But buy-and-hold aficionados don’t talk much about that statistic.

But let’s appease the hammerheads and acknowledge that the stock market usually regains its losses eventually—but at what cost?

Unfortunately, the price paid by many investors for following a passive investment strategy is often the most valuable commodity of all: time.

While the financial press continues to gloat about hitting new highs, it conveniently ignores the fact that since the year 2000, the stock market has spent much of the time either losing money or regaining lost ground. And, when we talk about investors meeting their long-term financial goals, time is money.

Common sense tells us that time is an integral part of compounding’s ability to work its wonders. We’ve all seen the illustrations of how someone starting early with small contributions can end up with a larger nest egg than someone starting later, even though the latecomer may make larger contributions. That’s why we always counsel investors to start saving as soon as they can, even if it’s not a lot of money. Yet periodic significant losses can render the time advantage impotent.

The financial press conveniently ignores the fact that since the year 2000, the stock market has spent much of the time either losing money or regaining lost ground.

And it gets even worse: Not only do losses require you to use valuable time to recoup portfolio losses after a drawdown, but you have to earn a higher return to get there. As we all know, a 40% loss requires a 66% return just to break even. That’s a double whammy if I ever saw one.

What’s needed is a way to sidestep losses during bear markets and major corrections, while remaining invested during up markets. Active investment strategies provide the potential to do just that.

Investment professionals need to diversify their clients among different investment strategies—both passive and active—and not just within a selection of various equity and bond holdings. Doing so could help portfolios weather the next storm (which some say is overdue) rather than getting hammered.

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

Mike Posey is the director of marketing for Theta Research LLC, a third-party performance tracking and publishing firm. He is also membership director for the Retirement Industry Trust Association (RITA) Mr. Posey has over 35 years of experience in a variety of management roles in the financial-services industry. thetaresearch.com

Mike Posey is the director of marketing for Theta Research LLC, a third-party performance tracking and publishing firm. He is also membership director for the Retirement Industry Trust Association (RITA) Mr. Posey has over 35 years of experience in a variety of management roles in the financial-services industry. thetaresearch.com