The correlation conundrum

Traditional risk management fails investors in both up and down markets

While equity investing always carries risk, there has been an implied promise in modern portfolio theory (MPT), and the financial advice of the media, that diversification will moderate that risk.

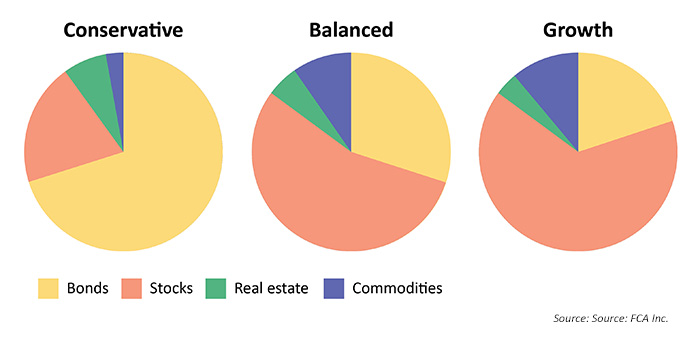

EXHIBIT 1: TRADITIONAL PASSIVE ALLOCATION

Under MPT, risk is managed through diversification. Individual-security risk is managed by diversifying among multiple companies. Interest-rate risk is managed through the balance of equities and bonds and diversifying among bond classes. Sector risk is managed through diversification among sectors with inverse correlations. General market risk is again managed through diversification among non- or low-correlated asset classes (Exhibit 1). Within each major asset class, diversification among geographic and industry sectors expands the perceived portfolio risk management.

By using correlation in portfolio design, the goal is to have some asset classes rising when others are falling, thus reducing risk. Invest in non-correlated assets and, when one asset class falls, the other will rise, offsetting losses.

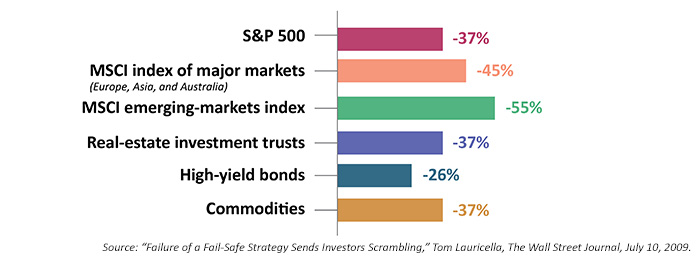

EXHIBIT 2: INDEX DECLINES IN CY 2008

Traditional passive allocation

In examining the problem with this approach, it is important to understand what modern portfolio theory does not do. MPT is designed to deal with unsystematic risk—the possibility that an investment or a category of investments will decline in value without having a major impact upon the entire market. Diversification typically does not protect against systemic risk, or market risk—the possibility that the entire market and economy will show losses negatively affecting nearly every investment. A portfolio may be considered well diversified because it holds assets with fairly low correlation to each other, when in fact these assets are only uncorrelated in relatively unstressed markets.

In major market downturns, asset classes tend to become highly correlated, moving together rather than offsetting the declines in other asset classes. Just when investors need risk management the most, diversification has limited value.

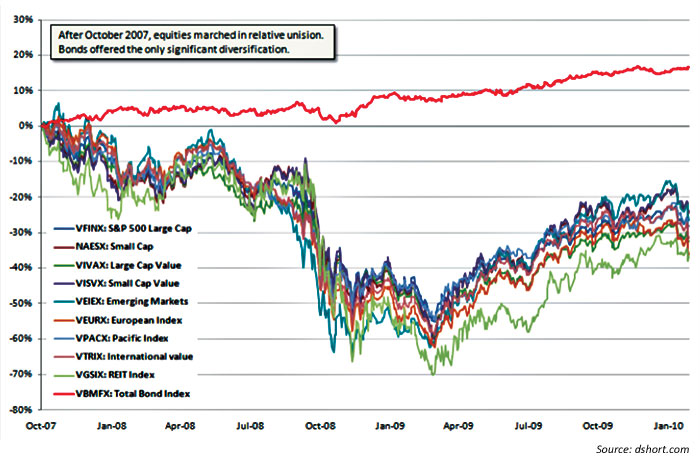

In 2008, the major indexes became highly correlated (Exhibit 2). In the first full week of January 2016, correlations again approached 1.0—perfect correlation—across nearly every major global equity index as they almost universally reported losses. In the aftermath of the 2008 market decline, author and analyst Doug Short published the chart shown in Exhibit 3. Will this scenario play out again? Only time will fully answer that question. But if it does, diversification will once more likely fail as a risk-management tool.

The chart dramatically depicts the positive correlation of diverse asset classes and geographic sectors during a major market decline. Only the Vanguard Total Bond Index stayed in positive territory, but the level of returns was insufficient to prevent even a conservative portfolio from experiencing a loss during the downturn. As a risk-management tool, passive diversification fails when it is needed most—in major downturns. But perhaps the greatest cost of diversification is its broken promise of risk management.

EXHIBIT 3: DIVERSIFICATION WORKS-UNTIL IT DOESN’T

There’s no shortage of studies showing that investors have traditionally fared best with a buy-and-hold approach to investing. Purchase a “low-cost” S&P 500 index, hold on through the ups and downs, and, over time, the investor may theoretically outperform active investment strategies. But real investors rarely manage to buy and hold through a full market cycle. Watching years of savings disappear—along with one’s hope of financial security and no guarantee that the market will recover in time—has shaken the most stalwart of investors. Just as there are a multitude of studies showing buy and hold works, there are a multitude of studies showing investors tend to buy high and sell low, underperforming in both rising and falling markets.

With the next major market decline, investors need real risk management, not the failed promise of passive diversification. Active investment management, with its market-driven approach to buy-and-sell decisions, may be an effective tool to benefit from the market’s ability to create wealth, while limiting the impact of its destructive downturns.

At this point, the proponents of passive diversification typically jump up to exclaim, “Yes, but no one has ever been able to predict the market, so active management can’t possibly work.”

If active management functions properly as “risk management,” limiting drawdowns in market declines and keeping individuals invested for the long term, it has succeeded.

After every major market decline, many individuals give up on investing, moving to the sidelines for years until the rising market finally overcomes the pain of losing money. If active management can keep those individuals from fleeing the market—if losses can be minimized and investors return to the market early in the upswing—that is real risk management.

Linda Ferentchak is the president of Financial Communications Associates. Ms. Ferentchak has worked in financial industry communications since 1979 and has an extensive background in investment and money-management philosophies and strategies. She is a member of the Business Marketing Association and holds the APR accreditation from the Public Relations Society of America. Her work has received numerous awards, including the American Marketing Association’s Gold Peak award. activemanagersresource.com

Linda Ferentchak is the president of Financial Communications Associates. Ms. Ferentchak has worked in financial industry communications since 1979 and has an extensive background in investment and money-management philosophies and strategies. She is a member of the Business Marketing Association and holds the APR accreditation from the Public Relations Society of America. Her work has received numerous awards, including the American Marketing Association’s Gold Peak award. activemanagersresource.com