The diversification dilemma

The diversification dilemma

Tactical management and today’s evolving markets.

How diversified are investor portfolios? The answer is that when diversification is needed most, portfolios may not be as diversified as investors assume.

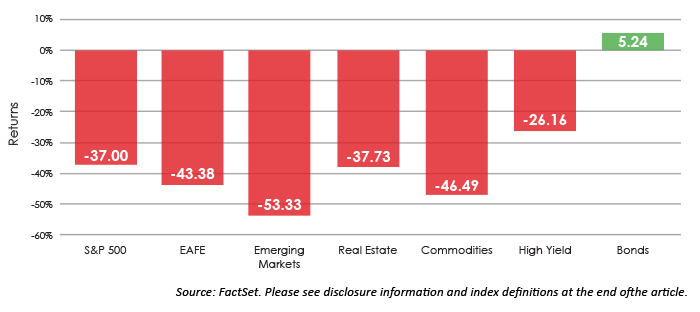

The Great Recession, which included 2008, taught investors this valuable lesson. When it was essential to be diversified, investor portfolios were often found lacking. In looking at Figure 1, we see that very few asset classes, other than high-quality bonds, provided investors a shelter from the storm.

We will explore the concept of portfolio diversification, the impact of evolving financial markets, and why we believe tactical management is playing an increasingly pivotal role.

Figure 1: Asset class returns (Calendar year 2008)

During the Great Recession, there were very few places for investors to turn.

The concept of diversification

Diversification can best be conveyed in the oft-repeated statement “don’t put all your eggs in one basket.” The concept underlying this statement assumes that all baskets will not break at the same time. Similarly, investors seek to diversify across multiple asset classes so they are protected when certain segments of the market take a downturn. But what happens when, like in the Great Recession, the majority of asset classes experience a severe downturn at the same time, undermining the benefit of diversification? To understand the limits of diversification, it is important to understand what investors are trying to achieve by investing across multiple asset classes and the forces determining asset class prices.

When investors speak of diversification, they typically mean diversifying away from large-cap U.S. equities, because the S&P 500 Index, which includes the 500 largest companies in America, has become a proxy for equity markets in general. We are reminded of this every time we turn on business news and listen to how much the market is up or down and why.

While this focus on large-cap U.S. equities may appear myopic, it’s interesting to note that the vast bulk of portfolio risk is generally related to U.S. equity volatility. Historically, at least 90% of a typical diversified portfolio’s volatility can be explained by large-cap U.S. equities. So, the desire to diversify away from this risk seems logical. Investors seek to invest in asset classes that they believe will zig when the S&P 500 Index zags.

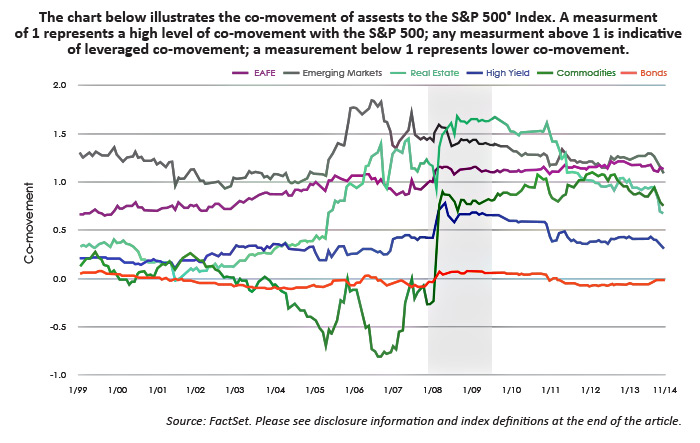

Figure 2: Co-movement of assets to the S&P 500 Index (Jan. 1999–Nov. 2014)

Now that we have identified what we believe investors are trying to achieve by investing across multiple asset classes, it would be helpful to understand what drives asset-class prices. Financial-asset-class prices are driven by buyer and seller behavior. Put simply, if there are more buyers than sellers, prices will generally increase. Likewise, if there are more sellers than buyers, prices will generally decrease. So, to understand the potential diversification benefits of investing across multiple asset classes, you need to anticipate buyer and seller behavior. For example, if you invest across five asset classes, all of which you expect investors to sell at the same time, it wouldn’t be logical to expect that allocating across those asset classes would provide meaningful diversification.

Investors experienced a real-life example of this in 2008. Fearful of a severe global economic downturn, investors did not just sell out of the S&P 500—they sold all asset classes they felt would be impacted by the downturn. Since money has to go somewhere, as investors sold “risky” asset classes most tied to the global economy, they bought perceived “less risky” or “safer” asset classes—like bonds backed by the U.S. government and issued by the most credit-worthy corporations. As a result, this buyer and seller behavior drove down the prices of perceived “riskier” asset classes while driving up the value of perceived “safer” asset classes.

After 2008, many investors suggested that diversification stopped working. We believe this suggestion is incorrect and is premised upon a misunderstanding of how asset-class diversification works. Most asset classes possess little inherent diversification quality. Their diversification benefits are derived from buyer and seller behavior, which can change over time. Diversification did not stop working in 2008; buyer and seller behavior adapted to evolving financial markets.

The impact of evolving financial markets

We believe that, over the last 20 years, two major interrelated developments have impacted asset-class diversification. The first is the increased integration of the global economy, and the second is financial product innovation or “financialization,” which has allowed buyers and sellers to express their behavior more uniformly across asset classes tied to the global economy. Consequently, as Figure 2 illustrates, leading up to 2008 and continuing in the current environment, there has been increased co-movement between a broad range of “risk” asset classes and the S&P 500. Driven by buyer and seller behavior, these increases in co-movement significantly reduced the ability to diversify away the risk associated with the S&P 500, which dominates portfolios.

Even subsequent to 2008, “risk” assets, which are more tied to the global economy, have maintained historically high co-movements with the S&P 500, suggesting the effects of globalization and financialization are structural and not an aberration. As long as these forces are in place, it is reasonable to assume that during economic stress periods, allocating across “risk” asset classes may provide limited diversification benefit. With this said, there is likely nothing preventing these relationships between the S&P 500 and these other asset classes from continuing to change. It is important to recognize that as global financial markets evolve, so will buyer and seller behavior.

Given these developments in the financial markets, what options are available to investors in search of an effectively diversified portfolio?

High-quality bonds?

Historically, high-quality bonds have maintained a low co-movement with the S&P 500, even in 2008. This is because as buyers and sellers sell “risk” assets, they buy perceived “safer” assets. This behavior seems logical and unlikely to change, so high-quality bonds should continue to be a good source of diversification from the risk associated with the S&P 500.

However, given low current interest rates, high-quality bonds may not be an attractive source of return. In addition to their low current yields, prices of high-quality bonds will fall if interest rates rise.

Over the coming years, investors needing more than minimal investment returns to reach their goals may find high-quality bonds lacking from a return perspective. For these investors, it will be difficult to avoid exposure to “risk” asset classes, including below-investment-grade bonds. However, as we have discussed, we should not expect “risk” asset classes to provide high levels of diversification during stress periods, which is when diversification is needed most.

The importance of tactical asset allocation

Given low interest rates and increased co-movement between “risk” asset classes and the S&P 500, it is more difficult than ever for investors to balance risk and return using traditional strategic asset-allocation strategies. Unlike strategic asset-allocation strategies, which maintain static allocations to bonds and “risk” asset classes in good times and bad, tactical asset-allocation strategies seek to increase or decrease a portfolio’s risk exposure based upon current market conditions.

While there are a number of different tactical approaches, most seek to capture the increased return potential of “risk” asset classes, including global equities, real estate, commodities, and high-yield bonds, while managing the risk associated with these asset classes. In essence, they seek to replace the reduced diversification benefit of allocating across multiple “risk” asset classes with modulation of market risk.

Due to the increased integration of the global economy, product innovation, and buyer and seller behavior, investors are finding it more difficult than ever to achieve effective diversification across “risk” asset classes. To complicate matters, while we believe high-quality bonds should continue to provide diversification, low yields and the potential negative impact of rising interest rates are return headwinds for bonds. This reality creates a dilemma for investors needing more than minimal returns to reach their goals.

In response, investors should consider more tactical asset-allocation strategies, which seek to replace the reduced diversification benefit of allocating across multiple “risk” asset classes with modulation of market risk.

Disclosures and Term and Index Definitions

Performance displayed represents past performance, which is no guarantee of future results. Index performance is for illustration purposes only and is not meant to represent any particular fund. Returns do not reflect any management fees, transaction costs, or expenses. The index is unmanaged and not available for direct investment.

The S&P 500 Index represents the large-cap equity market. The S&P 500 Index is an index of 500 stocks chosen for market size, liquidity, and industry grouping, among other factors. The index is viewed as a leading indicator of U.S. equities and is meant to reflect the risk-return characteristics of the large-cap universe.

EAFE is represented by the MSCI EAFE Index The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S., and Canada.

Emerging markets are represented by the MSCI EM Index. The MSCI EM (Emerging Markets) Europe, Middle East and Africa Index is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of the emerging market countries of Europe, the Middle East, and Africa.

Real estate is represented by the FTSE NAREIT All Equity REITs Index The FTSE NAREIT All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50% of total assets in qualifying real estate assets other than mortgages secured by real property.

Commodities are represented by the S&P GSCI Index. The S&P GSCI Index is a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities.

High yield is represented by the Barclays High Yield Index The Barclays High Yield Index is a universe of fixed-rate, non-investment grade corporate debt of issuers in non-emerging market countries. Eurobonds and debt issues from countries designated as emerging markets are excluded.

Bonds are represented by the Barclays Aggregate Bond Index The Barclays Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity.

Past performance is no guarantee of future results. Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

There can be no assurance that any investment product or strategy will achieve its investment objective(s). There are risks associated with investing, including the entire loss of principal invested. Investing involves market risk. The investment return and principal value of any investment product will fluctuate with changes in market conditions.

The opinions and forecasts expressed may not actually come to pass. This information is provided for informational purposes only and is subject to change at any time based on market and other conditions, and should not be construed as a recommendation of any specific security or strategy.

Guggenheim Investments represents the investment management business of Guggenheim Partners, LLC (“Guggenheim”). Securities offered through Guggenheim Funds Distributors, LLC. Guggenheim Funds Distributors, LLC is affiliated with Guggenheim Partners, LLC.

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.