The behavioral side of goals-based investing

The behavioral side of goals-based investing

As the advisory profession moves further into goals-based wealth management, advisors should prepare themselves for more frequent forays into behavioral psychology and human social behavior.

For nearly half a century, financial-planning and wealth-advisory professionals have been tirelessly telling the investing public that managing one’s wealth should not be about picking the hottest stocks, squeezing the last dollar of gains out of one’s portfolio, or finding the rare investment manager who can consistently beat the market year after year. It’s about your personal goals and your ability to meet them, both during and after your lifetime.

The message may be getting an additional lift through the implementation of what planners refer to as “goals-based investing,” a practice that is gaining in popularity. However, wealth managers are already aware that the role of a financial advisor frequently crosses the line into family counseling, career guidance, estate planning, and even divorce mediation. As the profession moves further into goals-based wealth management, advisors should prepare themselves for more frequent forays into behavioral psychology and human social behavior.

What is modern goals-based wealth management?

Goals-based investing is a lot different from, say, introducing a new investment vehicle or reallocating a client’s portfolio, and a lot more complicated from a behavioral perspective. In fact, it is less about investing at all and more about perceptions, dreams, legacies—in other words, subjective and emotional items.

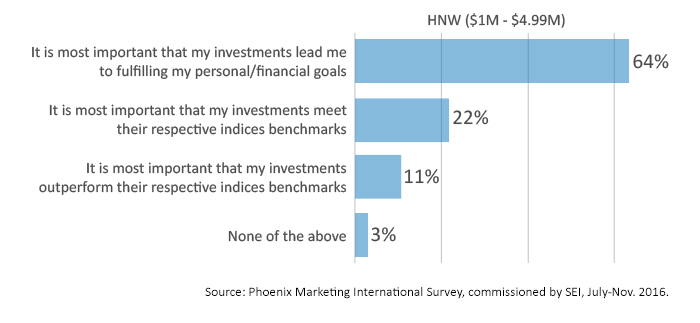

The goals-based approach is a welcome invention of the advisory and investment community, who sees it as a win-win for both clients and themselves in structuring a more relevant overall advisory relationship and an investing plan mapped to goals rather than strictly returns. One way it does this is by removing the traditional market benchmarks and replacing them with more personal, life-oriented benchmarks. These may be only indirectly quantitative (such as retiring in your late 50s) or more directly quantitative (such as the ability to donate a million dollars to your alumni fund). On the surface, the logic is sound and simple. The goals-based approach eliminates the problems associated with identifying an appropriate market benchmark, which can be highly challenging for portfolios with diversified assets, while also eliminating the need for potentially awkward conversations about why actual performance deviated from what advisors might see as an artificial and arbitrary benchmark.

What are some hurdles for the goals-based approach?

One would think that clients today aren’t really seeking out advisors who promise a consistent market-beating investment strategy, and are realizing that such a promise would be hollow, even if it wasn’t a regulatory no-no for the advisor anyway. For the most part, people come looking for advisors when they need holistic financial guidance to help them identify and meet their life goals. They are looking for an advisor or firm who provides them with the trust and confidence they require. So why not just play to that tune?

FIGURE 1: HIGH-NET-WORTH INVESTORS’ PERCEPTIONS OF INVESTMENT OBJECTIVES

The intuitive simplicity embedded into the goals-based rationale may well be its greatest strength. The problem is that while trying to deal with a behavioral issue, such as an overreliance on market benchmarks for performance monitoring, goals-based investing walks into a veritable thicket of other behavioral issues that advisors may not be aware of. More importantly, some of these issues are challenging and could become showstoppers for some clients, causing the goals-based approach to potentially backfire.

Goals-based investing walks into a veritable thicket of other behavioral issues that advisors may not be aware of.

One of the myths surrounding behavioral finance is that behavioral issues are somewhat trivial and a simple reframing of choices can cause a significant change in individual or mass behavior. This may occur now and then, but it is hardly the rule. Behavior modification is a complex affair, and some efforts will produce minimal results, while others can end up exacerbating the behavior in the wrong direction.

One example of the latter is that of a child-care center that was having continuing problems getting parents to pick up their kids on time. The center decided to ask parents in a nice way to be more diligent about being on time, and, as an added incentive, began charging parents a modest late fee. What happened? The problem got worse instead of better. Parents discovered they could now just pay their way out of their guilt and become even more lax about being on time.

One of the first things that goals-based advisors should recognize is that refocusing a client on life goals and away from market benchmarks may not be effective for all clients, even after they buy into the idea up front. Why? Because the market benchmark’s continual presence in the media may simply render it too difficult to ignore. Have you ever tried the little game where you ask someone not to think about something? Go ask a friend or family member not to think about polar bears. Then see how successful they are at not thinking about the very thing you suggested. You cannot tell someone not to watch the markets or not to read the news, or the same thing will happen. Many can’t ignore it. And when they pay any attention to it, the bias toward comparing their performance to that benchmark comes right back into the game.

With life-goal benchmarks substituted for a market index, several other behavioral issues will also tend to surface. Before advisors get too complacent about cutting the client’s cord to stock market performance, they may want to brush up on what the behavioral finance movement has taught us these past 30-plus years—that specific human biases germane to investing are both pervasive and deep-rooted.

One of these is the certainty bias. Humans like discreet things, hard facts, certainty. They deplore ambiguity as something that just doesn’t sit well with the human brain. The market benchmark may not be relevant to the client’s asset mix, but it does have something humans like—certainty. The well-studied effects of certainty bias show that people will accept less expected return in order to have greater certainty. (If they didn’t, the bond market would be in big trouble.) They also reach for certainty when making decisions or comparisons, even when it means sacrificing things like relevancy. It’s unconscious, and not necessarily rational, but it’s all too common. So despite all of the logic built around goals benchmarks, people may revert to their basic instincts when faced with unsettling, albeit inadvertent, market benchmark comparisons.

Another bias that will crop up is availability bias. The brain gets lots of input every day—enough to easily overload it if it tried to store it all. So it keeps the most recent information and keeps lopping off the older stuff. When you need to make a decision or a judgment on something, your brain will grab the most recent information. This can potentially lead to the notion that the goals-based approach is lagging the markets, even if that view is tainted by recent, rather than longer-term, performance.

Measuring how close or far you are from a life goal is not always feasible in financial terms, or even quantifiable at all.

Another problem is that in the absence of a quantifiable measure, people can’t easily determine whether they are truly better off this year than last. How do you reconcile a personal balance sheet that shows one new, completed college education for a child, but $150k less in family net worth? And will you feel you are better off if you have higher net worth but your health has deteriorated or your career is less fulfilling?

Measuring how close or far you are from a life goal is not always feasible in financial terms, or even quantifiable at all. How do you measure how happy you were with the first two years of your daughter’s college education? Are you disappointed that she went to a state university because you couldn’t afford her Ivy League preference? Would she have done as well with grades or had the same quality of professors and resources—or had the same future career options or networking opportunities? These are impossible to measure and, in many cases, revert to an overall determination of whether you are simply happier now than at some prior point in your life. Psychologists of all types can tell you that “measurement” of happiness is a very slippery slope.

What’s more, advisors who expect that an annual goals-based review might be a far more manageable and pleasant assessment of goals and performance could be in for some big surprises. With a market benchmark, advisors can prepare for the anticipated questions surrounding performance versus the benchmark and have some explanations readily at hand. With a goals-based review, the areas of ambiguity can be broader and more subjective if the goals are not carefully crafted.

None of this is meant to dissuade an advisor from taking a goals-based approach. It is meant instead as a wake-up call concerning issues that may surface as a result. Advisors will not experience these issues with all clients, but when these issues do surface, they are not necessarily trivial, and they can potentially throw a serious monkey wrench into the advisor-client relationship.

What can advisors do to prepare themselves?

Advisors are beginning to realize the importance of behavioral concepts in managing client relationships and setting expectations. A list of standard answers to the most common behavioral biases doesn’t exist, but there are plenty of good books that address the subject in language we can all understand. And there are formal certifications in behavioral finance available to advisors, as well as courses at various universities. An exposure to the most common biases can go a long way toward providing an advisor with a sense of confidence in dealing with them rather than getting caught off guard and potentially making the problem worse with a response that aggravates an issue rather than moving toward solving it.

Educating clients is not a bad idea either. It could be productive to substitute a good book on behavioral finance for that end-of-year bottle of wine or restaurant gift card. In addition, firms are now taking on behavioral coaches, both for themselves and their clients. The coach can be brought in only when needed or when the client elects to meet with them after being given the option. Not every client will feel the need, but for those that do, the intermediary could potentially have a huge impact on helping to save an advisor-client relationship that is having a rough period. Coaches and other third-parties versed in behavioral finance are also excellent choices for speakers at client events.

Managing the ongoing performance-evaluation process would be the next thing to focus on. To avoid the problems of availability bias, selective memory, and other behavioral issues, advisors might do well to create their own goal-centric evaluation mechanism. This might entail a list of goals, preferences, wish-list items, and so on, that is created when the client establishes their initial plan. Estimated time frames and any relevant milestones that can be identified up front toward the eventual fulfillment of those goals can also be included. Notes on each goal or milestone can be as elaborate as the client is willing to specify, and if the client has difficulty doing that, the advisor should prompt them as much as possible. Some advisors have created supporting visuals to direct their clients’ thinking process.

Other advisors, working with wealth-management firms and investment managers, have also taken the next big step toward more of a hybrid version of goals-based portfolio measurement. Here, performance evaluation is not only tied into life goals but also a personalized return benchmark identified in the financial-planning process as one that should adequately help the client meet their retirement-income and growth goals. This is very different from a market benchmark and relies on firmly educating the client on taking a longer-term perspective that might stretch out across a 30- or 40-year retirement period. The long-term trend of the personalized benchmark is what counts, not performance in any given month, quarter, or year. Many advisors combine this approach with more of an emphasis on risk-managed active-investment strategies that can help reduce portfolio volatility, creating a “smoother ride” over a longer investing time frame.

No matter the methodology chosen, advisors need to recognize that moving to a goals-based wealth-management process is a major decision that can have many potential upsides for a practice—as well as the importance of understanding the pitfalls identified here. Various methodologies should be evaluated, and peer feedback from advisors who have successfully instituted the process is invaluable. The rollout to clients needs to be handled carefully in an educational sense once the advisor has developed a goals-evaluation process that he or she believes is a good fit for their practice and clients. As the advisor gains further insights on goal-setting techniques in general, and on individual client needs specifically, the process should be refined in ways that will serve them well in maintaining successful client relationships.

Educating clients is not a bad idea either. It could be productive to substitute a good book on behavioral finance for that end-of-year bottle of wine or restaurant gift card. In addition, firms are now taking on behavioral coaches, both for themselves and their clients. The coach can be brought in only when needed or when the client elects to meet with them after being given the option. Not every client will feel the need, but for those that do, the intermediary could potentially have a huge impact on helping to save an advisor-client relationship that is having a rough period. Coaches and other third-parties versed in behavioral finance are also excellent choices for speakers at client events.

Managing the ongoing performance-evaluation process would be the next thing to focus on. To avoid the problems of availability bias, selective memory, and other behavioral issues, advisors might do well to create their own goal-centric evaluation mechanism. This might entail a list of goals, preferences, wish-list items, and so on, that is created when the client establishes their initial plan. Estimated time frames and any relevant milestones that can be identified up front toward the eventual fulfillment of those goals can also be included. Notes on each goal or milestone can be as elaborate as the client is willing to specify, and if the client has difficulty doing that, the advisor should prompt them as much as possible. Some advisors have created supporting visuals to direct their clients’ thinking process.

Other advisors, working with wealth-management firms and investment managers, have also taken the next big step toward more of a hybrid version of goals-based portfolio measurement. Here, performance evaluation is not only tied into life goals but also a personalized return benchmark identified in the financial-planning process as one that should adequately help the client meet their retirement-income and growth goals. This is very different from a market benchmark and relies on firmly educating the client on taking a longer-term perspective that might stretch out across a 30- or 40-year retirement period. The long-term trend of the personalized benchmark is what counts, not performance in any given month, quarter, or year. Many advisors combine this approach with more of an emphasis on risk-managed active-investment strategies that can help reduce portfolio volatility, creating a “smoother ride” over a longer investing time frame.

No matter the methodology chosen, advisors need to recognize that moving to a goals-based wealth-management process is a major decision that can have many potential upsides for a practice—as well as the importance of understanding the pitfalls identified here. Various methodologies should be evaluated, and peer feedback from advisors who have successfully instituted the process is invaluable. The rollout to clients needs to be handled carefully in an educational sense once the advisor has developed a goals-evaluation process that he or she believes is a good fit for their practice and clients. As the advisor gains further insights on goal-setting techniques in general, and on individual client needs specifically, the process should be refined in ways that will serve them well in maintaining successful client relationships.

Educating clients is not a bad idea either. It could be productive to substitute a good book on behavioral finance for that end-of-year bottle of wine or restaurant gift card. In addition, firms are now taking on behavioral coaches, both for themselves and their clients. The coach can be brought in only when needed or when the client elects to meet with them after being given the option. Not every client will feel the need, but for those that do, the intermediary could potentially have a huge impact on helping to save an advisor-client relationship that is having a rough period. Coaches and other third-parties versed in behavioral finance are also excellent choices for speakers at client events.

Managing the ongoing performance-evaluation process would be the next thing to focus on. To avoid the problems of availability bias, selective memory, and other behavioral issues, advisors might do well to create their own goal-centric evaluation mechanism. This might entail a list of goals, preferences, wish-list items, and so on, that is created when the client establishes their initial plan. Estimated time frames and any relevant milestones that can be identified up front toward the eventual fulfillment of those goals can also be included. Notes on each goal or milestone can be as elaborate as the client is willing to specify, and if the client has difficulty doing that, the advisor should prompt them as much as possible. Some advisors have created supporting visuals to direct their clients’ thinking process.

Other advisors, working with wealth-management firms and investment managers, have also taken the next big step toward more of a hybrid version of goals-based portfolio measurement. Here, performance evaluation is not only tied into life goals but also a personalized return benchmark identified in the financial-planning process as one that should adequately help the client meet their retirement-income and growth goals. This is very different from a market benchmark and relies on firmly educating the client on taking a longer-term perspective that might stretch out across a 30- or 40-year retirement period. The long-term trend of the personalized benchmark is what counts, not performance in any given month, quarter, or year. Many advisors combine this approach with more of an emphasis on risk-managed active-investment strategies that can help reduce portfolio volatility, creating a “smoother ride” over a longer investing time frame.

No matter the methodology chosen, advisors need to recognize that moving to a goals-based wealth-management process is a major decision that can have many potential upsides for a practice—as well as the importance of understanding the pitfalls identified here. Various methodologies should be evaluated, and peer feedback from advisors who have successfully instituted the process is invaluable. The rollout to clients needs to be handled carefully in an educational sense once the advisor has developed a goals-evaluation process that he or she believes is a good fit for their practice and clients. As the advisor gains further insights on goal-setting techniques in general, and on individual client needs specifically, the process should be refined in ways that will serve them well in maintaining successful client relationships.

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

Richard Lehman is the founder/CEO of Alt Investing 2.0 and an adjunct finance professor at both UC Berkeley Extension and UCLA Extension. He specializes in behavioral finance and alternative investments, and has authored three books. He has more than 30 years of experience in financial services, working for major Wall Street firms, banks, and financial-data companies.

Richard Lehman is the founder/CEO of Alt Investing 2.0 and an adjunct finance professor at both UC Berkeley Extension and UCLA Extension. He specializes in behavioral finance and alternative investments, and has authored three books. He has more than 30 years of experience in financial services, working for major Wall Street firms, banks, and financial-data companies.