Agility drills for client investment portfolios

Agility drills for client investment portfolios

Are your clients invested with enough “agility” to mitigate the risk of large drawdowns during severe market declines?

Football season is in full swing, and all of the fanatics out there (myself included) have been treated to a season with plenty of surprises already. I can’t wait for the playoffs to start.

While most of us now participate in football by watching, many can also think back to our “playing days” in high school—when preparation for the upcoming season provided challenging conditions meant to simulate or surpass tough game situations.

I don’t know who decided that dressing up in full pads twice per day in the hot Texas sun was a good idea, but it seemed to be the thing to do in late August back in my hometown. “Two-a-days,” the tradition of having two daily football practices, one morning and one late afternoon, were a rite of passage in virtually every school district in Texas. I’m sure it was the same way in other states—it’s just hotter down here.

The “Friday Night Lights” movie and TV show attempted to shine a light on high school football in Texas, but to my way of thinking, that is how the rich kids played ball. Those of us in a small, “Class B” high school back in the 1970s had to make do with what we had, both in equipment and players. For example, our “trainer” was one guy with a roll of tape and a bottle of salt tablets, while our second string was mostly the first string in different positions. Hydration consisted of two water hoses—usually reserved for irrigating what little grass would grow on the field in those hot, dry conditions.

So, what does all of this football talk have to do with investing? I’ll admit that there is no shortage of literature comparing the two. But the purpose of this article is to highlight the importance of agility, both on the playing field and in an investment portfolio.

Perhaps the best place to start is to define what agility is. Wikipedia defines it as, “… the ability to change the direction of the body in an efficient and effective manner.” Obviously, physical agility is an important trait in football, where the object of the game is either to score a touchdown or to prevent one. When you don’t know which way your opponent is going to go, you must be prepared to react to whatever direction is taken to make the play. The same goes for investing.

The problem is that many investment portfolios today are passive, the very opposite of agile. If there has ever been a time when investment advisors should be concerned about the agility of their clients’ portfolios, it’s right now. We all know what happened to buy-and-hold investment strategies in the early 2000s and again in 2007–2009. Were your clients invested with enough agility to avoid those large losses—and those of prior bear market periods?

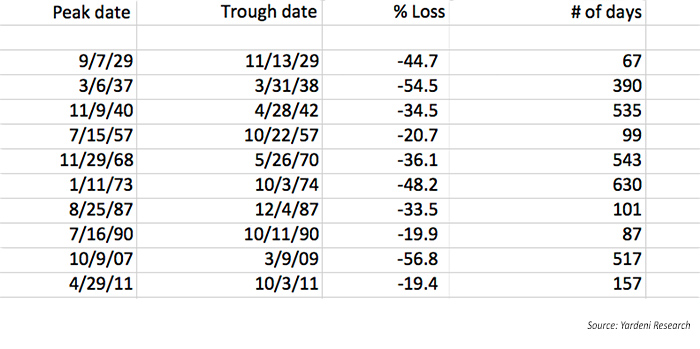

TABLE 1: WORST BEAR MARKETS/CORRECTIONS FOR S&P 500 OF EACH DECADE (1920–2017)

Failure to include agile investment strategies can be costly. In football, the lack of agility can result in an opposing team’s score, or your own team’s fumble or tackle for a loss. For an investment portfolio, the lack of ability to adapt to market conditions can result in huge losses (see Table 1).

Continuing with the football analogy, I would like to suggest five ways you can improve the agility of your investment portfolio:

- Diversify. Just as it wouldn’t make much sense to field a team with players that all have the same skill sets or who all play the same position, an agile investment portfolio should also be diversified to include noncorrelated strategies, each with different strengths in the portfolio. In the role of coach, the investment advisor must select the team of available strategies best designed to meet their clients’ investment goals.

Unfortunately, when discussing diversification, most of the financial press is talking about a passive, 60/40 stock/bond type of traditional allocation, often modified for the age of the investor. While including a small allocation to a passive strategy is probably a good idea from a diversification standpoint, it should not be the only strategy employed. Why? Because passive asset-allocation portfolios have done so poorly in past bear markets, requiring years to get back to breakeven. This can become an overwhelming sequence-of-returns issue for investors, especially retirees. To say the least, passive strategies have fumbled the ball at the worst possible times.

To illustrate this point, back in high school I had a coach who believed that all of the plays he developed were designed to produce a touchdown every time they were run—if they were executed properly. To prove the point, he decided (seriously!) that we would play an entire game using only two plays. You can imagine the result arising from this failure to diversify. No matter how well a play is designed, if the other team knows the ball will go either one place or another, you’re going to lose. We lost.

To achieve true diversification, advisors should develop portfolios for their clients that include tactical strategies with the agility to move to cash or other asset classes as market conditions dictate. Whether you call these strategies active, tactical, or alternative, they are characterized by rules-based strategies that seek to follow market trends rather than being victimized by them.

- Know the playbook. This may sound very basic and unrelated to agility, but no amount of speed or quickness can help you if you’re in the wrong place at the wrong time. In an investment portfolio, it’s important for advisors to communicate why each investment strategy is included and what it is intended to do. In football, sometimes an aggressive passing style is called for on offense; at other times, a tightly controlled and conservative game plan. At different times in the same football game, either style might be called for.

Similarly, it’s equally important to make sure that multiple investment strategies are represented in clients’ allocations and not just multiple asset classes. To be effective, the overall plan for a portfolio should be like a playbook, with different strategies designed to perform during a variety of market conditions across long time frames.

Unfortunately, I have seen advisors who want to remove one or more strategies because of underperformance over a short-term period. They think that all strategies should make money in all market environments, which is clearly not the case. It would be like removing a play from the playbook just because it didn’t work against one opponent.

- Watch the films. The Saturday morning after the game was always dedicated to watching the game films. We used an old WW II–era Bell and Howell movie camera that often resulted in pictures so fuzzy that you’d swear it was filmed from the next county. What we could see clearly would be critiqued by our coach, usually in the form of running the projector backward and forward to document a missed blocking assignment or poor tackling technique.

Returning to the investment world, reviewing the films is akin to advisors monitoring their clients’ portfolios regularly. This is not to say that anyone—client or advisor—should be overly concerned with scrutinizing performance every day or every week. Instead, advisors should review their clients’ portfolios as frequently as quarterly and no less than annually. Such a review can help to determine whether the portfolio’s constituents are performing as expected and whether the risk level is appropriate.

- Be ready for unplanned opportunities. In my high school football days, we had an incredibly fast quarterback. Occasionally, he would call a play but then realize that a lane had opened up that allowed him to run a quarterback sneak. I remember blocking according to my playbook assignment, only to see him standing in the end zone. His vision, coupled with his agility, resulted in a touchdown. (Of course, these little excursions didn’t always work, so our coach encouraged keeping them to a minimum.)

Advisors need to be aware that their clients are the target of direct advertising for a wide variety of investments, including precious metals, real estate, and even private equity opportunities. In addition, some advisors have clients who made their fortunes in real estate, oil, or other investments and want to continue to “dabble” in opportunities that might come along.

In such cases, advisors need to again take on the role of coach and help evaluate these opportunities on behalf of their clients. Going back to the playbook, the advisor might be able to show the client how the same or similar opportunities are already present in the portfolio holdings. Most importantly, however, is the need to realize that investment products marketed directly to investors are sometimes subject to higher risks than disclosed in the flashy marketing brochures promoting them.

- Keep fantasy football in its place. A final point in this analogy is to be wary of the investment equivalent of fantasy football. For those who do not partake in fantasy football leagues around the world, it’s a way to establish imaginary teams of actual players and then score points based on their actual performance during games. The athlete’s performance is real and the games are real, but the scores are nothing but pure fantasy, hence the name.

A similar exercise in “fantasy” in the investment world is known as backtested performance. Backtesting occurs when an investment manager has a strategic idea, but it has not been traded with real money in an investment account. The solution is to set up a backtest, usually consisting of hypothetical trades applied to the past performance of a financial asset such as a stock, bond, index, mutual fund, or ETF.

Backtesting can be a valid and productive analytical tool when used properly, and a dangerous tool when used improperly. And, to be fair, there are many times when backtests are the only data available, such as in a brand-new strategy just starting out. Even so, investment advisors must resume their coaching role and make sure that not only is the trading strategy evaluated but also the methodology of producing the backtest. One solution to the backtesting question is to seek out database services that review and analyze the investment returns of managers’ various strategies based on actual performance. Database services can offer a sort of “scouting report” when looking for agile investment managers.

Postgame analysis

I hope you have enjoyed this trip back to my old high school playing days. However, unlike high school football, where you can lament “maybe next year” after a losing season, there’s seldom such solace for financial advisors.

Either your clients will meet their goals of a child’s college education or they won’t. Ditto with purchasing a home, starting a business, or a myriad of other financial goals. Most importantly, they will either have a secure retirement or they won’t, and you won’t have a second chance to create a sound portfolio for them with the agility to handle the ups and downs of the market over several decades.

After 30-plus years in the investment industry, and having lived through markets of all types, I have come to some firm convictions. By including actively managed strategies in your clients’ portfolios, they will have a better chance, I believe, of being on the winning team and reaching their investment goals.

The opinions expressed in this article are those of the author and do not necessarily represent the views of Proactive Advisor Magazine. These opinions are presented for educational purposes only.

Mike Posey is the marketing director for Theta Research, LLC, an investment performance database and publishing firm. He has more than 35 years of marketing and management experience in the investment and retirement-planning industries. His prior experience includes serving as marketing director at Halbert Wealth Management and as president at Sterling Trust Company, a provider of self-directed retirement account services. Mr. Posey is a graduate of Baylor University and has earned the Fellow, Life Management Institute (FLMI) designation. http://www.thetaresearch.com/

Mike Posey is the marketing director for Theta Research, LLC, an investment performance database and publishing firm. He has more than 35 years of marketing and management experience in the investment and retirement-planning industries. His prior experience includes serving as marketing director at Halbert Wealth Management and as president at Sterling Trust Company, a provider of self-directed retirement account services. Mr. Posey is a graduate of Baylor University and has earned the Fellow, Life Management Institute (FLMI) designation. http://www.thetaresearch.com/