10 questions to ask third-party asset managers

10 questions to ask third-party asset managers

Money managers add value beyond investment expertise, freeing up time for advisors to do what they do best. How do you evaluate them?

It’s not easy being a financial advisor, especially in today’s complex financial environment. Clients need a lot of attention, and advisors offer far more services than first meets the eye. One successful advisor interviewed in the Maryland area has identified 50 discrete client-related “major financial tasks” to review for each and every client. Then, like any other business owner, there are the day-to-day office duties to handle, employees to manage, and strategic business concerns to address with a vigilant eye.

For financial advisors running small businesses, it can feel like there aren’t enough hours in the day. That is one critical and pragmatic reason why more and more advisors are partnering with third-party asset managers, especially money managers who add additional value through sophisticated risk-management approaches.

However, it makes sense to do so. This kind of partnership gives advisors the time they need to focus on their core business—clients—and immersing themselves in the information gathering that will inform the strategies that will produce the financial outcomes those clients want.

A Forbes article reinforces this point, saying, “Financial advisors can offer a tremendous amount of value by dealing with extremely complex tax issues, investment choices, and emotional decisions impacting one’s financial well-being. Furthermore, they make people more secure for retirement, increase their client’s wealth, and help people feel more confident about their financial status.”

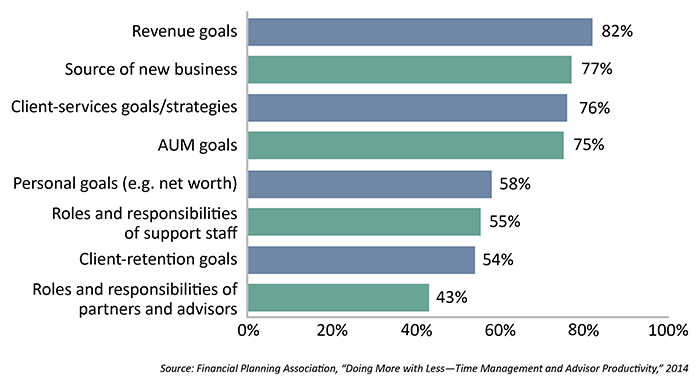

And the facts back this up.

A study by the Investor Protection Institute, a tough critic of the business, acknowledges to consumers that financial plans work. “Research shows that over a lifetime, investors with a financial plan accumulate about 20% more wealth than those with no plan.” A Morningstar paper places the figure even higher, with estimates of the advisor impact helping to create “29% higher retirement income wealth.”

The expertise a third-party active asset manager can offer, when coupled with the financial advisor’s top-notch customer service, creates a valuable package to offer any discerning client. Of course, as with any effective partnership, the asset manager needs to be properly vetted before any relationship is established. Due diligence on third-party asset managers is becoming an increasingly important task for the individual independent advisor, their firm and associates, and their broker-dealer.

- How long have they been doing what they are doing, and how well is it documented?

- What are the qualifications of the asset manager’s leadership and analytical team and their bench strength?

- What is their specific strategic focus? Is it narrow or broad?

- Do they execute well and consistently on their strategies?

- Are they adaptable in changing market environments?

- Do they have strong risk-management capabilities?

- Are their reporting systems timely and user-friendly?

- Do they provide tools to address suitability questions and client risk profile assessments?

- Do they have value-add materials to help in client education?

- Are they committed to customer service and problem resolution for both advisors and clients?

In the end, after all, time is money.

This article, originally titled “Experts need experts,” first published in Proactive Advisor Magazine on June 18, 2015, Volume 6, Issue 11. The content and title have been revised and updated. David Wismer contributed to this article.

Kellye Whitney is founder and chief creative officer at Kellye Media & Associates. She was previously associate editorial director at Human Capital Media. She has specific expertise in human resources, diversity practices, and workforce learning and development programs. Her work has received several distinguished media awards.

Kellye Whitney is founder and chief creative officer at Kellye Media & Associates. She was previously associate editorial director at Human Capital Media. She has specific expertise in human resources, diversity practices, and workforce learning and development programs. Her work has received several distinguished media awards.